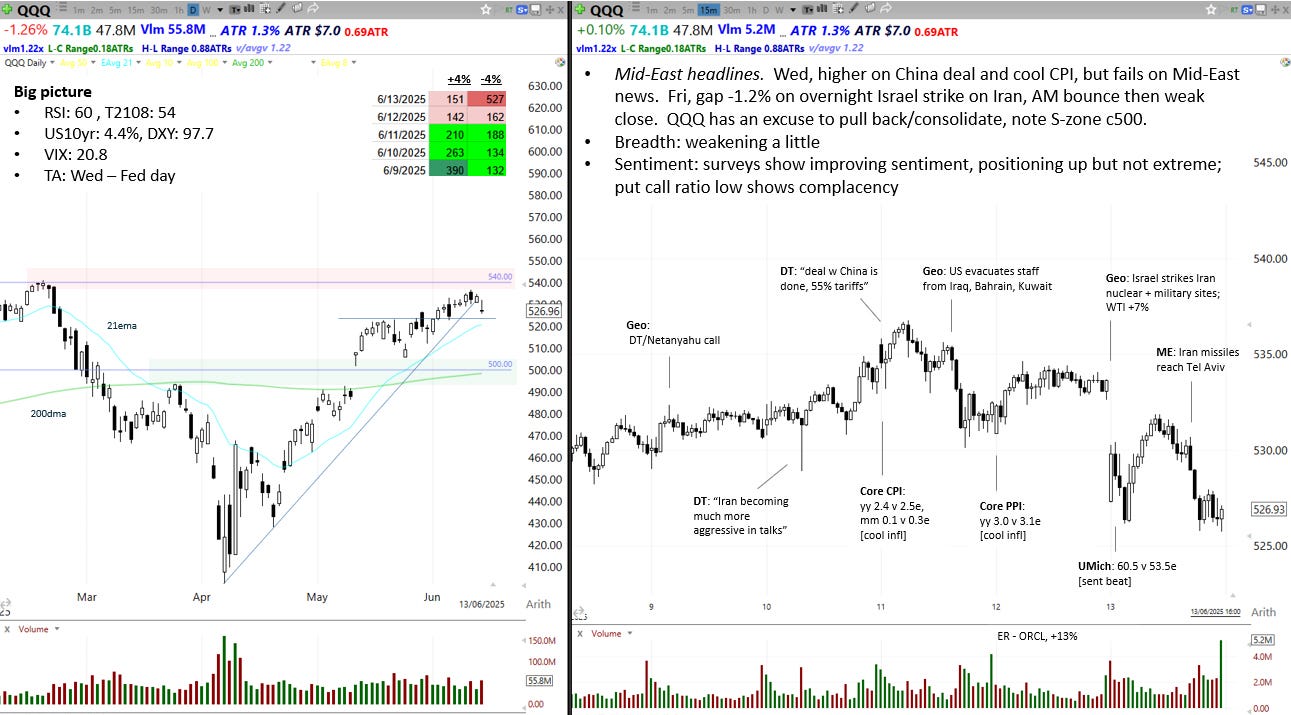

Price action

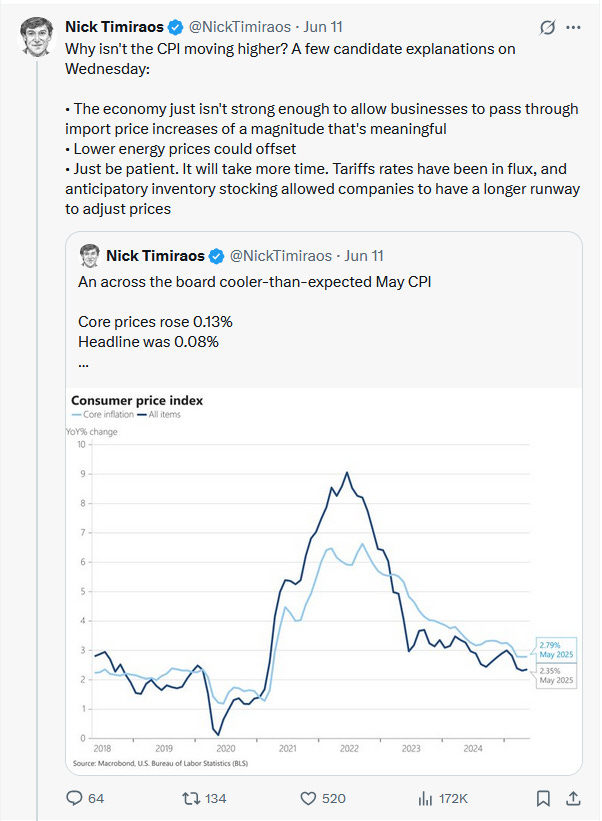

QQQ fell -1.8% from its intraweek high as Middle East headlines returned. Clues of a coming Israeli strike arrived through the week. On Monday, President Trump spent an hour on the phone to Netanyahu, a call which we now know focused on Friday’s attack; then on Tuesday, Trump noted Iran had become “much more aggressive” in talks. Significantly on Wednesday morning, QQQ was unable to rally despite two quite strong bullish catalysts - the first being a positive outcome to the US/China trade talks in London, the second being a cool CPI release that relieved fears about a tariff-induced spike. Then on Wednesday afternoon, it was reported that America was withdrawing its non-essential personnel from posts across the Middle East. Those reports led to a persistent move higher in oil and a move lower in stocks as markets repriced the probability of military action by Israel. Finally on Friday, news broke that Israel had launched large scale attacks on Iranian nuclear and military targets. Initially QQQ bounced at the open, but as news arrived of Iranian retaliatory strikes against Tel Aviv, QQQ weakened to close at the low of the day.

This episode may provide QQQ a reason to pull back from clear resistance at its all time high c540. This would be the first material pullback since late April. The most obvious level of support is the zone around 500, which lines up with the 200dma and 100dma. A drop to 500 would represent a -6.7% pullback for QQQ.

The Fed

The Fed were in blackout this week ahead of next week’s FOMC meeting. JPowell will have been encouraged by cool CPI and PPI data, but the path ahead is still uncertain.

Markets and Narratives

1/ Trade

President Trump framed the outcome of this week’s London talks with China as positive, especially in relation to the supply of rare earths to America. However, it appears China have only signed up on rare earths for six months, so we can expect this story to return before too long.

2/ US debt sustainability

The US government conducted UST auctions on Wednesday and Thursday that both saw solid demand. The US debt sustainability theme might be receding for now.

3/ Middle East

Israel and Iran continue to exchange attacks over the weekend. In 2023 and 2024, investors were rewarded for buying dips created by Middle East headlines. If the current military action fizzles out quickly, that playbook seems likely to be rewarded again.

However, the action over the last few days has been hotter than 2023-24. If Iran’s energy complex is targeted then this episode has the capacity to cause more lasting trouble for QQQ. Here is a summary of key areas and installations to look out for in the headlines. Meanwhile, the ever useful leShrub offers this handy guide:

There are further escalatory wildcards. The first concerns direct US involvement in striking Iran. Could they get drawn into the conflict by giving Israel the ordnance it needs to destroy the heavily fortified uranium enrichment plants at Fordow and Natanz? The second concerns regime change in Iran, which would be drawn out, complex, and unpredictable.

Keep an eye on US oil producers, which moved higher on these developments.

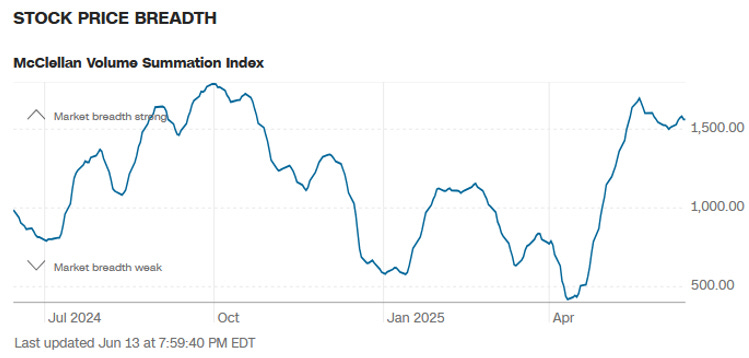

Breadth

Breadth eased this week as markets pulled back. However, there was no major pullback in the McClellan Summation Index.

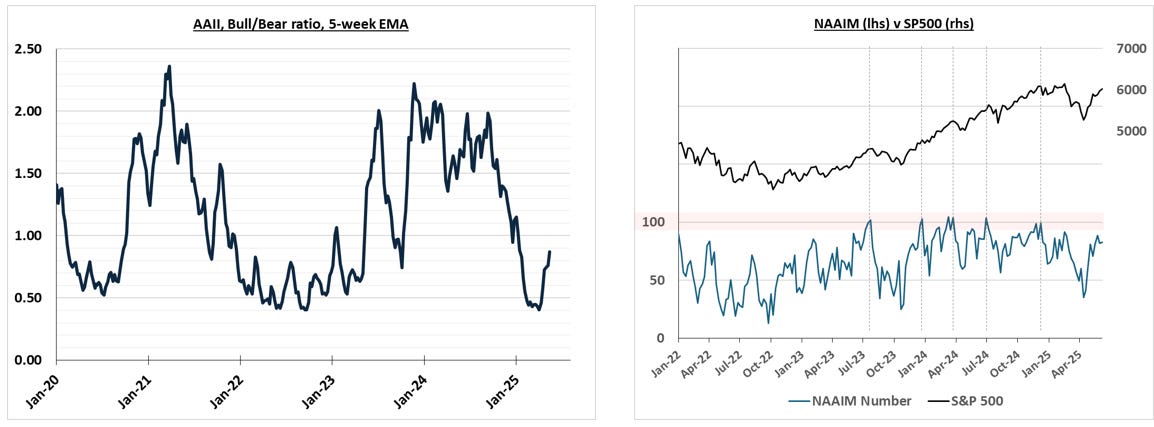

Sentiment and Positioning

The AAII and NAAIM surveys continue to show steadily improving sentiment. These are conducted on Wednesdays and Thursdays respectively, so they don’t reflect Friday’s events. Neither show enough exuberance yet to suggest a contrarian bearish signal.

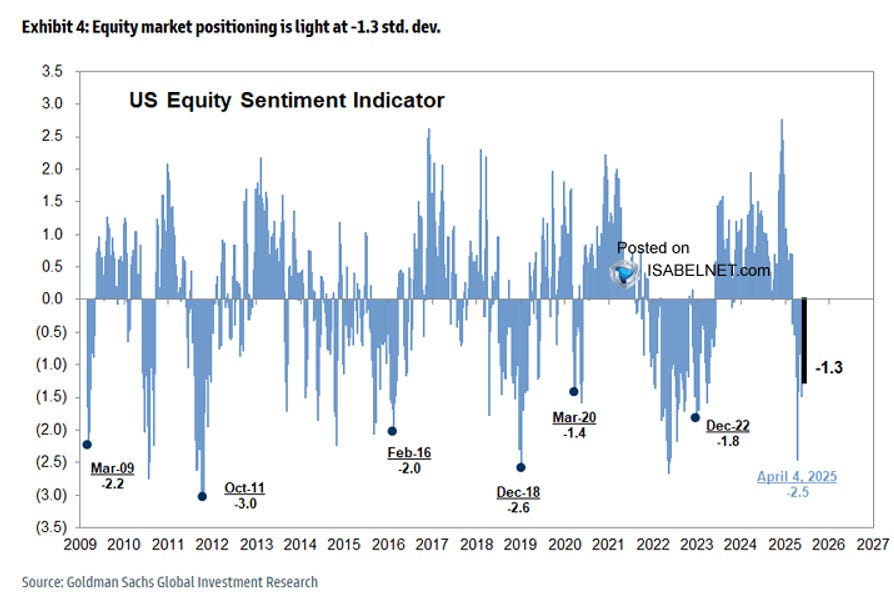

The GS US Equity Sentiment Indicator remains stubbornly light, despite the recovery in stocks from post Liberation Day lows. This continues to be a constructive dynamic for QQQ.

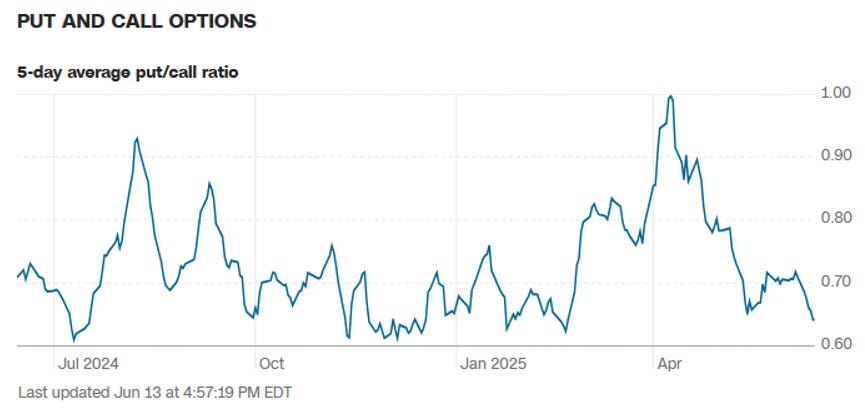

The options market suggests investors have become complacent in the short term, which could support the idea of a short term pullback.

Seasonality

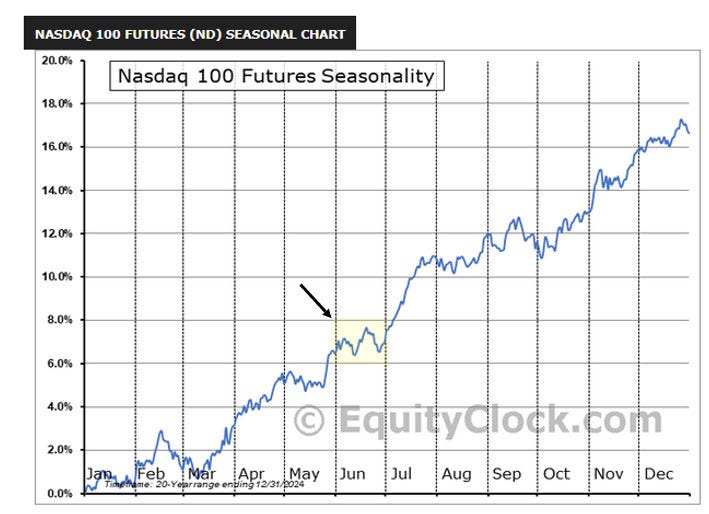

June tends to be a choppy month. July is more clearly bullish. A phase of Middle East related volatility would fit the seasonal pattern quite well.

Summary

Price action: QQQ fell -1.8% from its intraweek high as Middle East headlines returned. A pullback may be underway. The clearest confluence of support is around 500, which would constitute a -6.8% pullback.

The Fed: the Fed was in blackout ahead of next week’s FOMC meeting. CPI and PPI came in below consensus expectations, however the impact of tariffs may still be ahead of us.

Markets and Narratives: trade policy and America’s fiscal position faded as key narratives this week as Middle East conflict returned. Middle East headlines are likely to drive price action in the short term.

Breadth: eased off as indices retreated.

Sentiment: surveys suggest neutral sentiment and light positioning among investors. Options markets suggests short term complacency.

Seasonality: June is a choppy month for the Nasdaq 100. July is a bullish month. The US Presidential cycle suggests bullish conditions till August.

Key events next week: Tue - Retail Sales; Wed - FOMC interest rate decision and press conference.

View

Short-term: neutral. Interested in a pullback to 500/200dma for a potential long.

Long-term: neutral-bullish

Technical evidence

QQQ has reclaimed it 200dma and has spent five weeks above it.

Realised volatility is consistent with bull market conditions.

Breadth was very bullish off the lows, evidenced by a sequence of thrust signals with good statistical records (Zweig breadth thrust, HY bond breadth thrust, Degraaf breadth thrust).

Sentiment and positioning is supportive as investors remain lightly positioned.

Fundamental evidence

Trump admin continues to walk back hardline trade policy.

Recent economic data shows economy is ok.

Supportive themes in tech (AI, defence, nuclear energy, cybersecurity).

Fiscal stimulus set to continue absent a bond market revolt.

Challenges and risks

Middle East conflict has returned, will this be short-lived or drawn out? Will it impact global energy markets? Will America become directly involved?

Tariffs, immigration policy, and higher energy prices may lead to upside inflation surprises in coming months, though there is no sign of this yet.

Weak seasonality in Q3