Price action

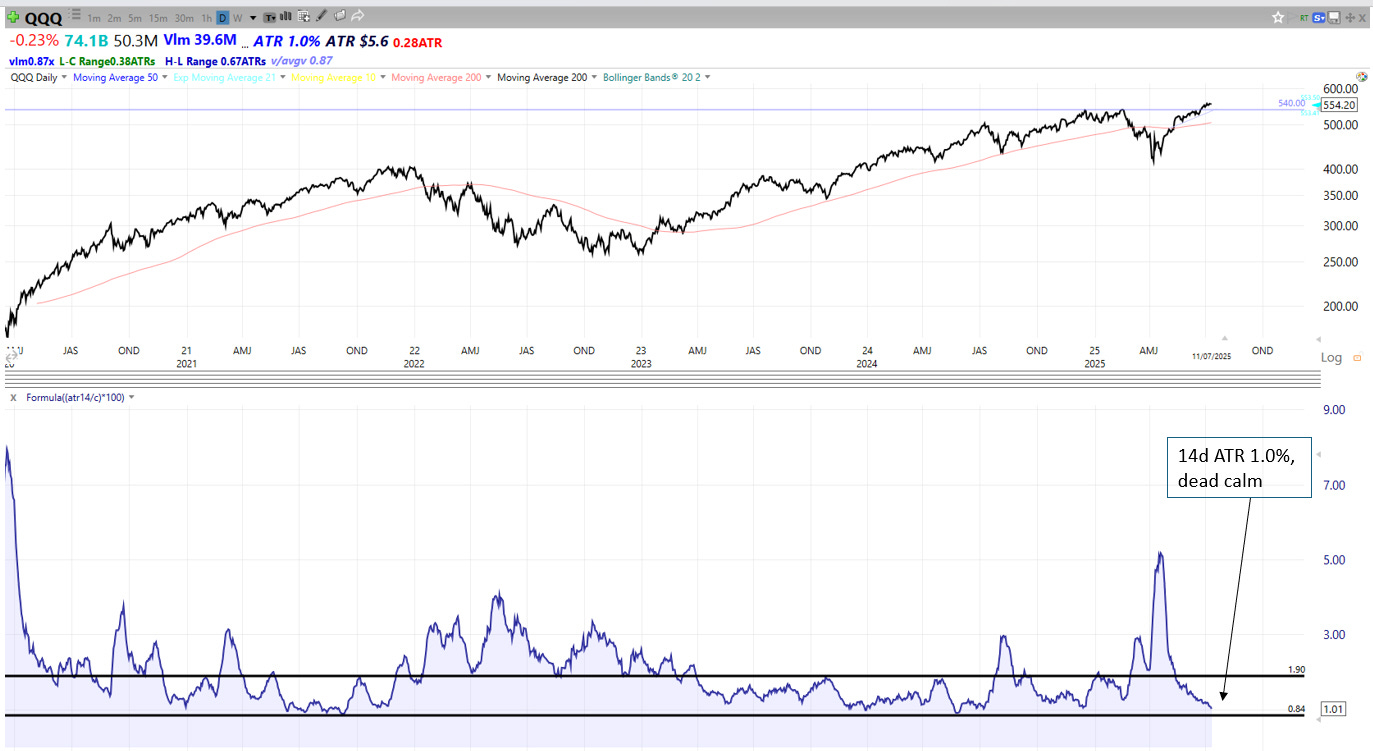

QQQ traded in a super-tight 1.5% range, holding new all time highs above 540. There was a notable lack of reaction to adverse tariff news at the end of the week when President Trump announced 50% tariffs on Brazil and 35% tariffs on Canada. Realised volatility has fallen to very low levels, with the 14d ATR down to 1.0% (it doesn’t get much lower than 0.8%).

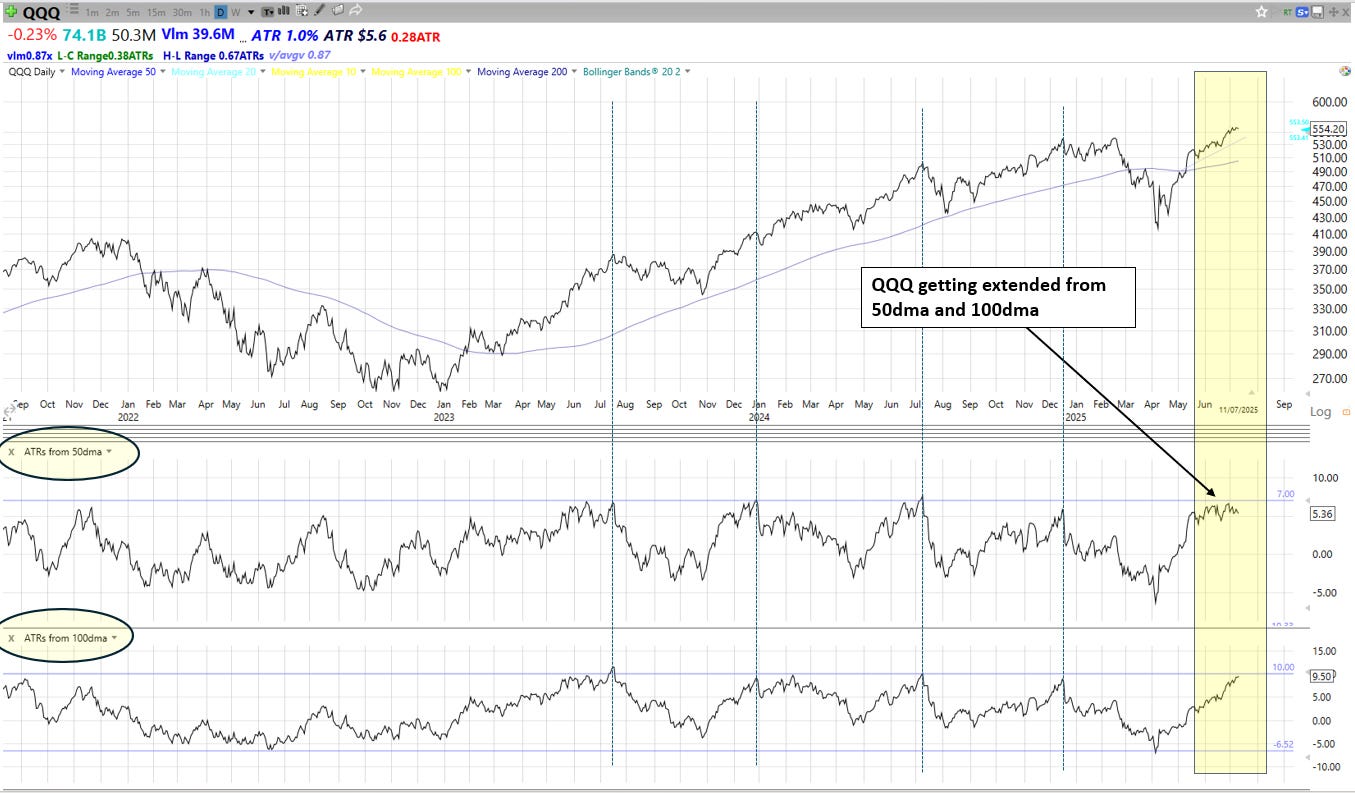

Last week we noted that QQQ was getting a little overbought. While the daily RSI fell to 66 this week, QQQ remains quite extended from its 50dma and more clearly its 100dma, which may set us up for a period of consolidation or pullback.

The Fed

On Wednesday, the Fed released minutes of their June meeting. The minutes indicate something of a split in the FOMC, with a couple of members favouring a July cut but most keeping to JPowell’s wait-and-see approach. From recent speeches, we know the two members who favour a July cut are Michelle Bowman and Christopher Waller. Towards the end of the week Trump announced 50% tariffs on Brazil and 35% on Canada, and over the weekend he has announced tariffs of 30% on the EU and Mexico. This muddies the water for the Fed, who have stated they need more clarity about the impact of tariffs on inflation, which may take a while to feed through to the economy. Austan Goolsbee made that point on Friday:

Goolsbee (Fri): latest tariff threats could delay rate cuts, the threats could spark fresh concerns about inflation and force the Fed to maintain its wait-and-see approach, new round of tariffs makes it messy to truly say how the economy is doing, if prices start rising again will be nervous.

Markets & Narratives

1/ Trade

As noted above, on Saturday 12 July, Trump threatened to impose 30% tariffs on the EU and Mexico, which follows 50% tariffs on Brazil and 35% tariffs on Canada. We will see how the market takes that news on Monday.

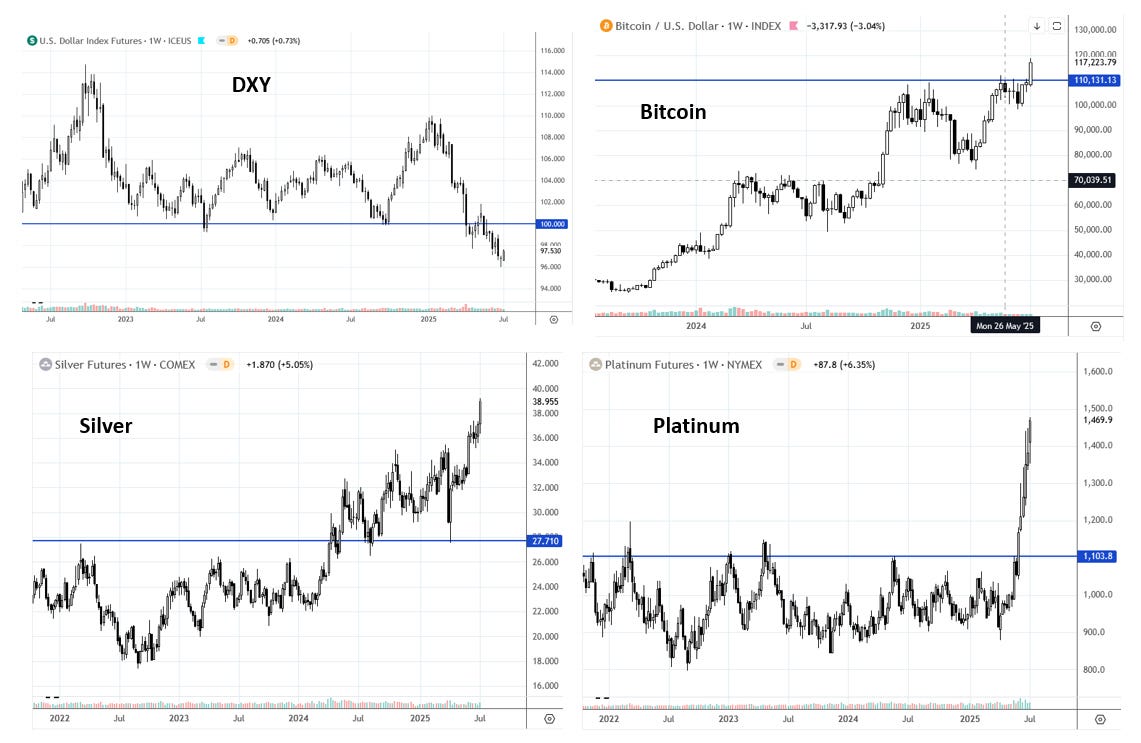

2/ USD debasement

The dollar has been weak so far in 2025. Very large US fiscal deficits are set to continue for years, the Fed may start cutting rates again later this year, and President Trump has made it clear he intends to install a dovish stooge as the next Fed Chair who is prepared to play along with Trump’s boom agenda. Furthermore, Bessent and Trump himself have indicated the Treasury will flip from issuing longer-dated Bonds to shorter-dated Bills to raise financing. This has the effect of increasing liquidity within the financial system. As a result of all these influences, DXY has fallen from 110 at the start of the year through support at 100, down to 97.5. After that big move, DXY looks extended to the downside and may retrace higher, perhaps retesting 100, which could be accompanied by a pullback in stocks. However, the root causes of dollar weakness look like they will be around a while.

As well as supporting US stock prices, this dollar debasement theme is supporting precious metals. Gold has been trending for some time and now platinum is joining the party. So too is their digital cousin, Bitcoin.

Breadth

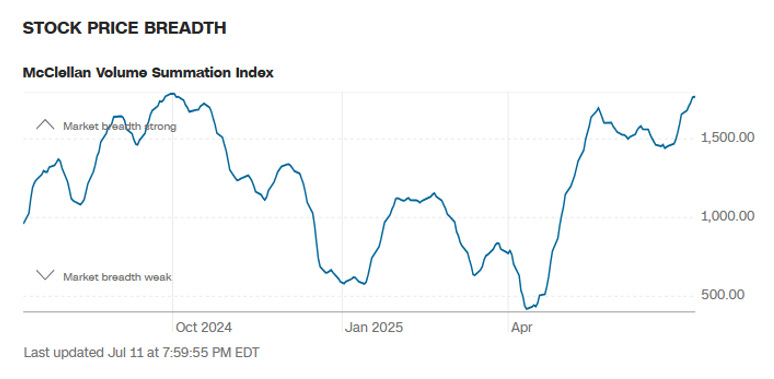

Breadth continues to be solid, if unspectacular. The McClellan Summation Index is rising:

Sentiment & Positioning

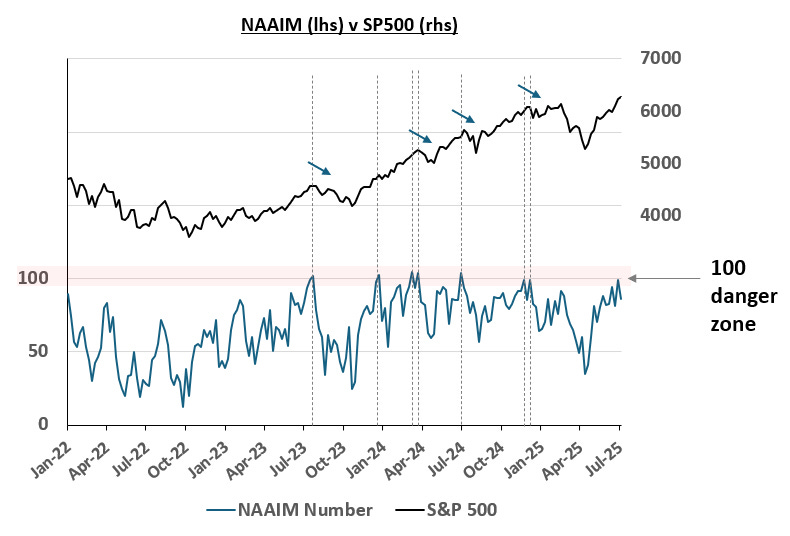

Last week we noted that the NAAIM survey had hit 99, which constituted an amber flag. This week it eased back to 86, which is a marginal positive, but it’s still pretty high.

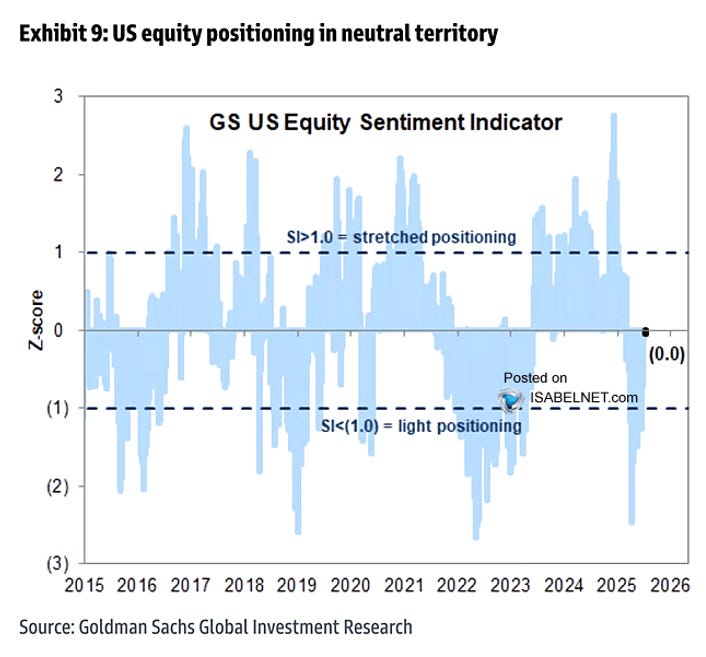

However, the GS US Equity Sentiment Indicator remains stubbornly unbullish, suggesting there is more runway before institutional investors become overpositioned.

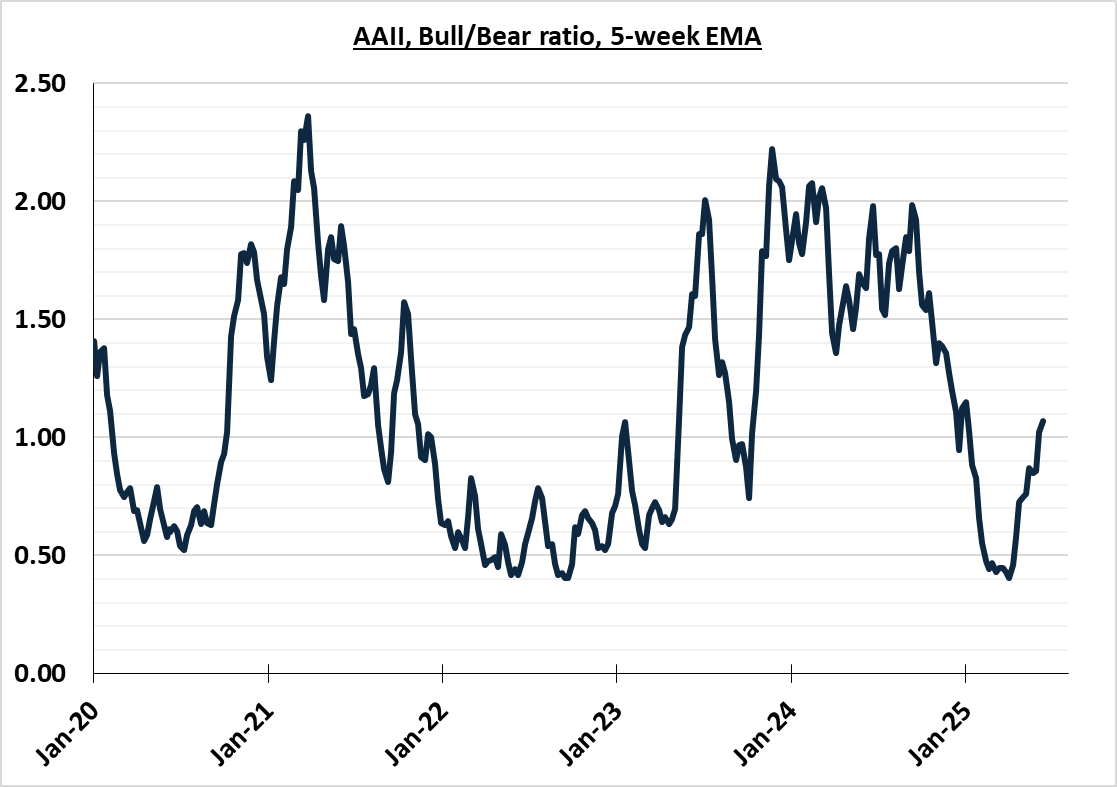

The AAII survey shows sentiment continuing to improve from the very bearish extreme seen in April, but it’s by no means overly bullish.

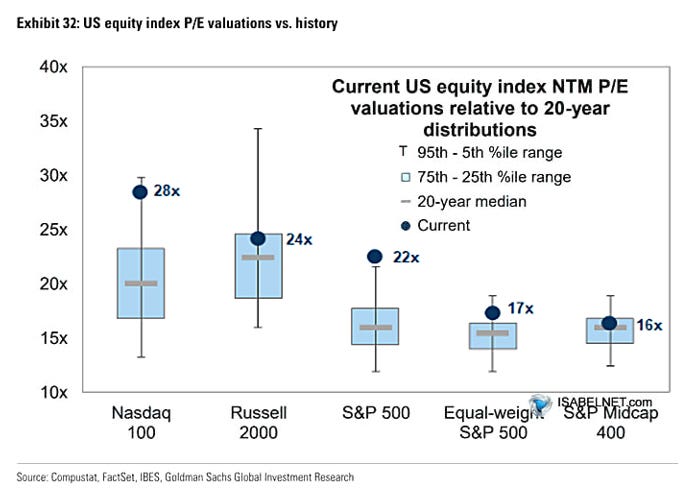

Stock index valuations have crept back up for the Nasdaq 100 and S&P500. PEs can be a useful longer-term gauge of sentiment, offering an insight into how willing investors are to bid up or sell down stocks.

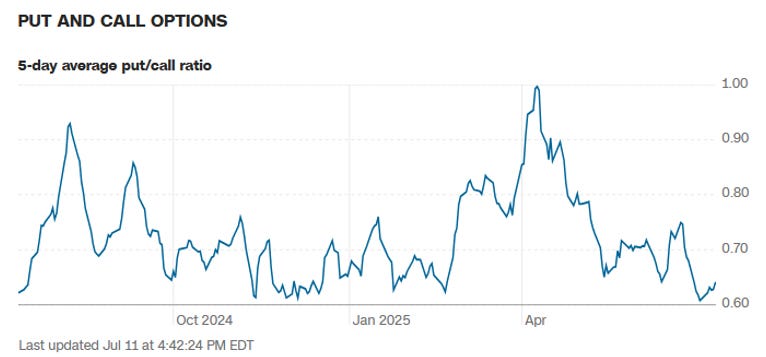

The put call ratio 5dma continues to suggest a mood of complacency.

Seasonality

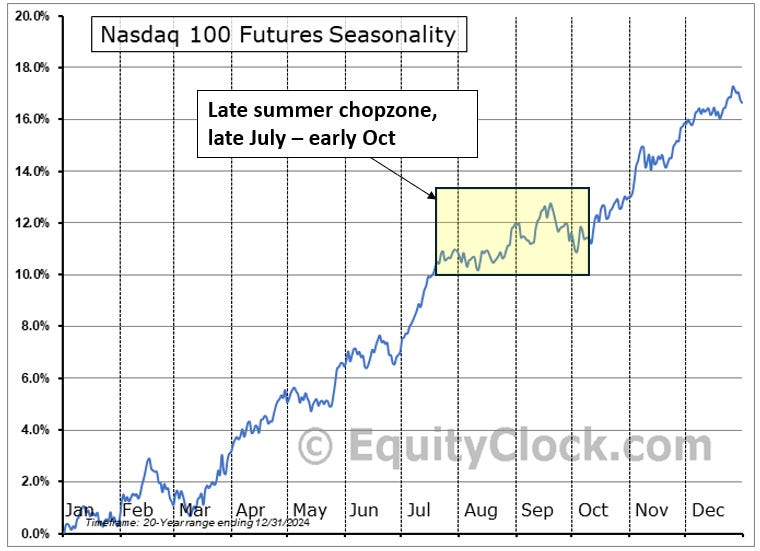

We are still in July’s favourable seasonal window, but the late summer chopzone is approaching.

Summary

Price action: QQQ traded in a tight range despite adverse tariff headlines. Realised volatility is very low. Somewhat overbought conditions.

The Fed: some members of the FOMC favour cutting the FFR in July, but the majority are in favour of the current wait-and-see stance.

Markets and Narratives: Trump’s new round of tariff announcements have not made an impact on markets yet. Note strength in precious metals and Bitcoin arising from dollar weakness.

Breadth: in decent shape.

Sentiment and Positioning: investor surveys suggest moderately bullish sentiment, but it’s not quite yet extreme enough to raise a red flag. Valuations are reaching rich levels again. The put call ratio is low, suggesting complacency.

Seasonality: July is a bullish month for QQQ, but late summer chop is approaching.

Key events next week: Fed speakers all week, unscheduled trade headlines, possibly Russia/Ukraine developments, Tue - CPI, Thu - earnings from TSM (premarket) and NFLX (after hours).

View

Short-term: bullish momentum remains strong, but QQQ is somewhat overbought. A pullback to 540 may provide an attractive entry for a tactical long.

Long-term: primary trend bullish.

Technical evidence:

Having spent nine weeks above its 200dma, QQQ has broken to new all time highs.

A Golden Cross signal triggered on 23 June.

Realised volatility is consistent with bull market conditions.

Breadth was very bullish off the lows, evidenced by a sequence of thrust signals with good statistical records (Zweig breadth thrust, HY bond breadth thrust, Degraaf breadth thrust).

Fundamental evidence:

Fiscal stimulus is set to continue absent a bond market revolt. Treasury is switching issuance to Bills from Bonds, which increases system liquidity.

The Fed may cut rates in the coming months.

Trump intends to select a dove as JPowell’s successor.

Trump admin has walked back hardline trade policy.

Recent economic data shows US economy is ok.

Supportive themes in tech (AI, defence, nuclear energy, cybersecurity).

Challenges and risks:

Tariffs and immigration policy may lead to upside inflation surprises in coming months, though there few signs of this yet.

Weak seasonality in Q3: