QQQ weekly: 4 - 8 May

Lock-out rally

Price action

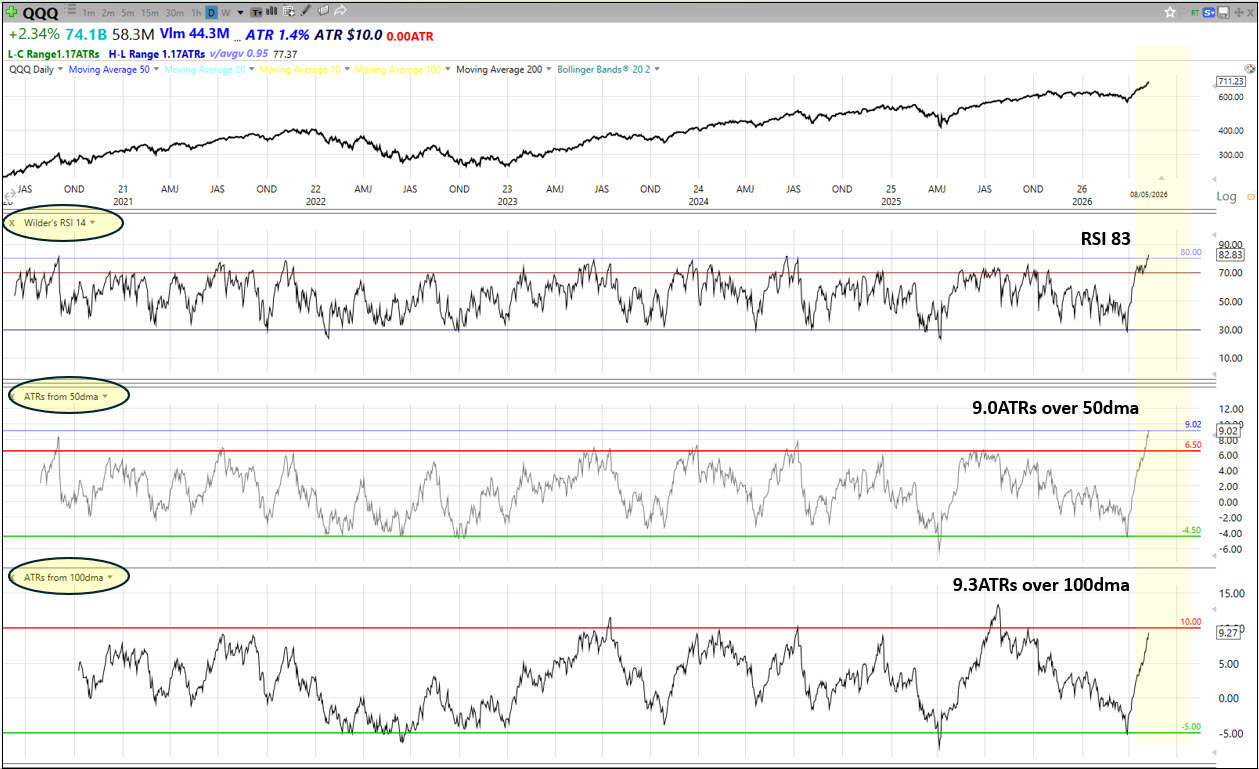

QQQ continued its lock-out rally, +5.5% for the week and +28% from the low set just 28 sessions ago at the end of March. The semiconductor ETF, SMH, closed the week +11%, and +58% from the March low.

QQQ’s annualised rate of change from the low is now more than +1,100%, while its daily RSI is north of 80. While a pause must come eventually, red-hot short-term momentum makes it hard to say when. In terms of its daily RSI, which is 82.8, and the number of ATRs above its 50dma, which is 9.02, QQQ is the most overbought since January 2018.

The Fed

Last week we discussed the hawkish trio of dissenters (Kashkari, Hammack, and Logan) who weren’t happy with the Fed maintaining language in its FOMC statement that implies an easing bias. The chorus continued this week, with Hammack, Kashkari, Musalem, Goolsbee, and Barr all delivering messages that explicitly or implicitly push back on near-term cuts because of inflation persistence from tariffs and the energy shock.

Kashkari (Thu): if Hormuz remains shut for long, the next move may needs to be a hike

Goolsbee (Wed): it would be wrong to think only cuts are before the Fed

Barr (Tue): elevated energy prices could bleed into goods and services prices.

Musalem (Tue): plausible scenarios exist either for hiking or cutting

However, the influential Vice Chair, John Williams, kept the door open for cuts later this year.

Williams (Mon): Fed not in a position to offer strong guidance for next meetings, but inflation expectations remain well-anchored, Fed will need to cut rates at some point once price pressures dissipate.

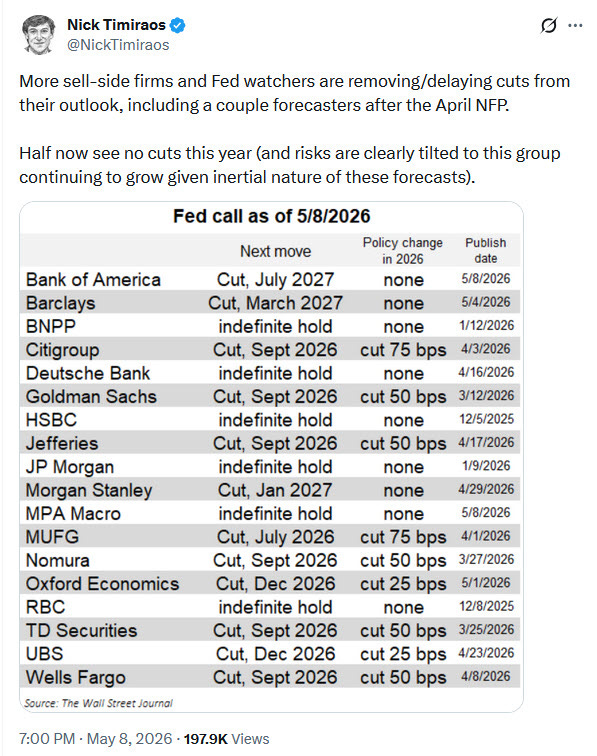

With inflation rising and Friday’s NFPs showing a stabilisation in the unemployment rate, Kevin Warsh will have a tough time pushing through cuts early in his tenure. Accordingly, street analysts are dialling down forecasts for cuts this year.

Markets & Narratives

1/ Earnings

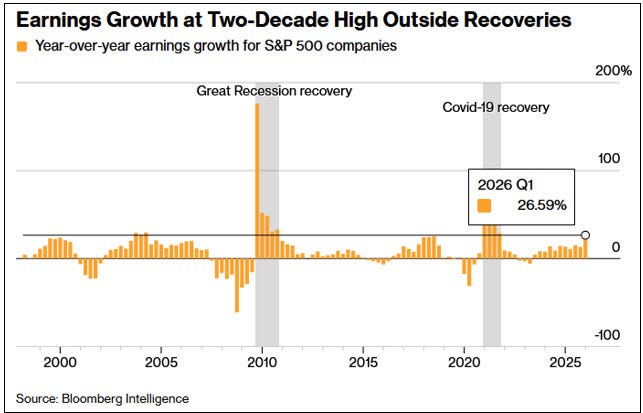

QQQ’s rally has been helped by a very strong earnings season.

Corporate America has outstripped expectations by the widest margin outside the Covid-19 era since at least 2013.

First-quarter profits at S&P 500 companies have surged, with about 85% of companies surpassing analyst forecasts, and the so-called Magnificent Seven firms are expected to post a 57% jump in profits.

The bull market in earnings continues to support the bull market in stock prices.

2/ Bond yields

Something to keep an eye on as a potential obstacle for QQQ. The US30y yield looks like it could be coiling for a breakout. With inflation creeping up due to tariffs and high energy prices, with the jobs market OK, and with AI capex humming, there are fundamental dynamics that could push bond yields higher. Higher yields due to a strengthening economy are ok, but the pace of change is important - QQQ does not like fast moves at the long end.

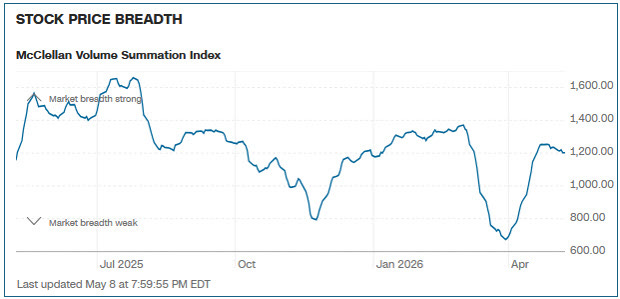

Breadth

This week’s rally in QQQ was not confirmed by improving breadth, which is not ideal. The McClellan Summation Index is drifting lower.

Sentiment & Positioning

A lock-out rally is a sustained, persistent advance in which the market refuses to give pullback-buyers a meaningful entry opportunity. Each shallow dip gets bought aggressively, intraday weakness reverses by the close, and would-be buyers waiting for a 3-5% pullback to add never get filled. They are in effect locked out.

A lock-out rally begins from a condition where investors are underinvested in the market as a result of a negative narrative, like the Iran conflict. When the narrative improves, there’s a scramble to put risk back on. Underexposed managers become forced buyers to avoid underperforming the index, systematic CTAs and volatility targeting strategies are forced to buy as the trend changes and the market calms down, and investors of all types and sizes close their hedges. This can last a while, but when sentiment and positioning finally catch up with price, then there are no more locked-out buyers left to capitulate back into the market

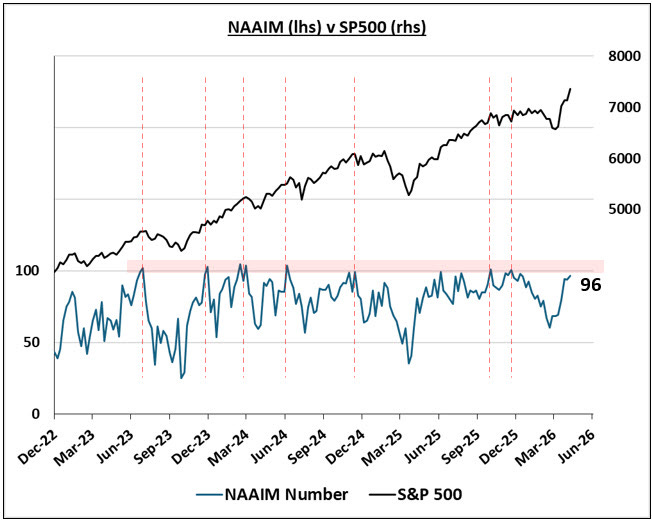

So, how far through this repositioning process do the indicators suggest we have got?

The NAAIM is at 96. When it exceeds 100 it’s been a useful signal that investors are too bullish and has preceded phases of consolidation or pullback.

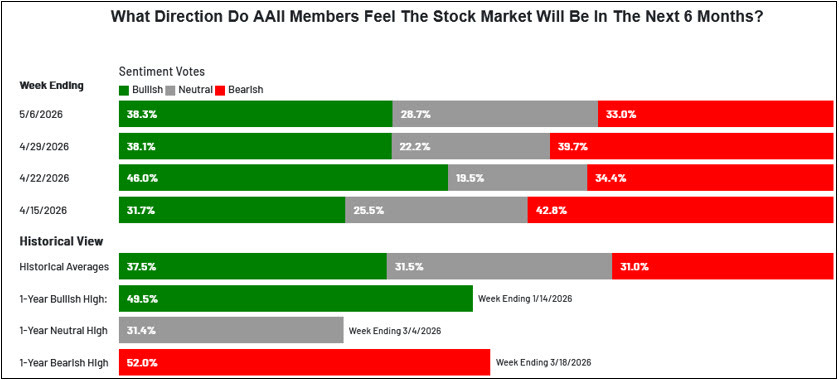

However, the AAII survey does not show signs of euphoria. Bulls are at 38%, nowhere near the 52wk high of 49.5%

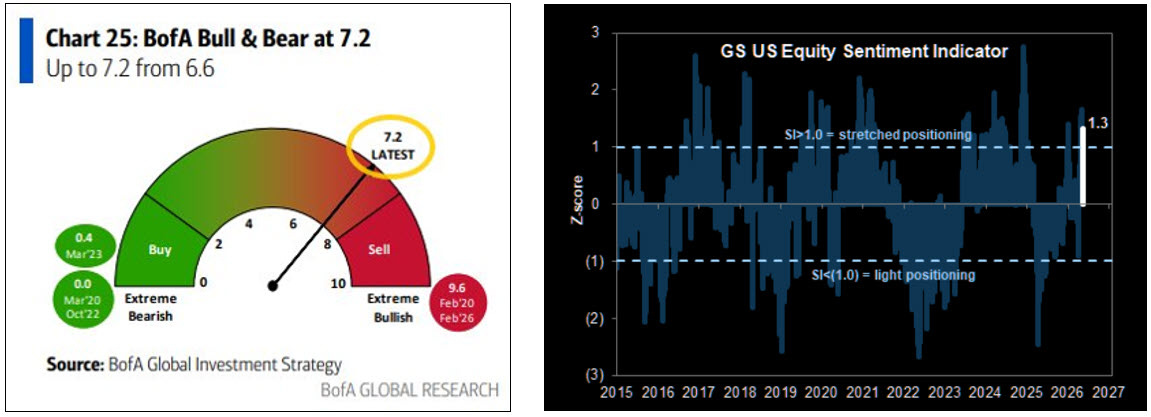

Moreover, the invstment bank surveys don’t suggest euphoric sentiment or positioning. BoA’s indicator is at 7.2, while the GS US Equity Sentiment Indicator is at 1.3.

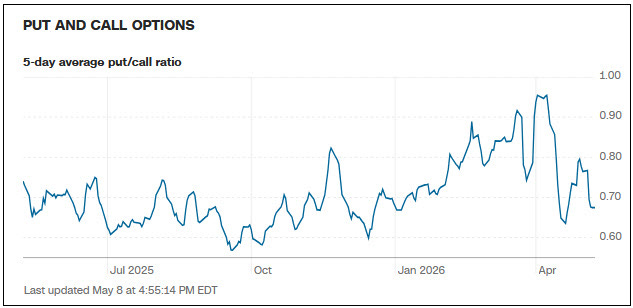

As for the options market, the Put Call Ratio 5dma is low, but not on the mat.

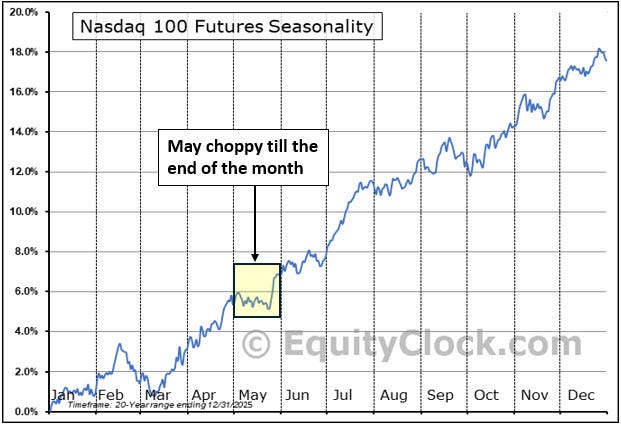

Seasonality

May is seasonally choppy, but closes strongly.

Summary

Price action: QQQ continued to push higher in what feels like a lock-out rally. Momentum is strong, but QQQ is very overbought. The longer-term primary trend is bullish.

The Fed: the FOMC is moving in a hawkish direction as result of rising inflation pressures and a stabilising job market. Warsh will have a difficult job building a consensus among FOMC members for rate cuts.

Markets & Narratives: 1/ Earnings season has been very strong. 2/ Monitor long end bond yields.

Breadth: somewhat disappointing.

Sentiment & Positioning: increasingly bullish, but not yet overextended or euphoric.

Seasonality: May is choppy but closes strong.

Key events next week: Iran news, Tue - CPI, Thu - Trump visits China.

View

Short-term: red-hot momentum, but very overbought

QQQ is still too overbought to chase, but momentum is too strong to fade. More broadly, conditions continue to favour breakout opportunities in leading stocks.

Long-term: cautious bullish

From a technical perspective, QQQ has done what it needed to do to reclaim its long-term primary bullish trend - it’s back at the top of its long-term channel and back above its moving averages.

From a fundamental perspective, the picture is more constructive than a few weeks ago. The negative narrative headwinds of Iran, private credit, and AI disruption are fading, while the positive tailwinds of earnings, AI capex and AI productivity are back. However, the oil price shock is not over yet, mid-term seasonality is not helpful till the back-end of the year, plus there is a growing risk of Fed dysfunction when Warsh takes over as Fed Chair.

Challenges and risks

Iran conflict and energy shock

Weak mid-term seasonality

Fed dysfunction under new Chair Warsh

OpenAI’s ability to honour its spending commitments

If you enjoy these posts and find them useful, please do share with colleagues, friends, or on social media - thank you.

Alex