QQQ weekly: 27 Apr - 1 May

Momentum continues

Price action

On Monday, QQQ shook off the failure of last weekend’s peace talks between America and Iran and held up fine, but on Tuesday it encountered a bump in the road. This came in the form of a WSJ article that suggested OpenAI is missing revenue targets and might be unable to meet its spending commitments, causing AI momentum names to gap down sharply. However, buyers showed up in the middle of Tuesday’s session and QQQ rallied for the rest of the week, helped along by reports that America and Iran are continuing to engage in talks, and also by Wednesday’s hyperscaler earnings that showed: 1) no let up in the AI capex theme, and 2) indications that AI capex is translating into increasing revenues, margins, and EPS.

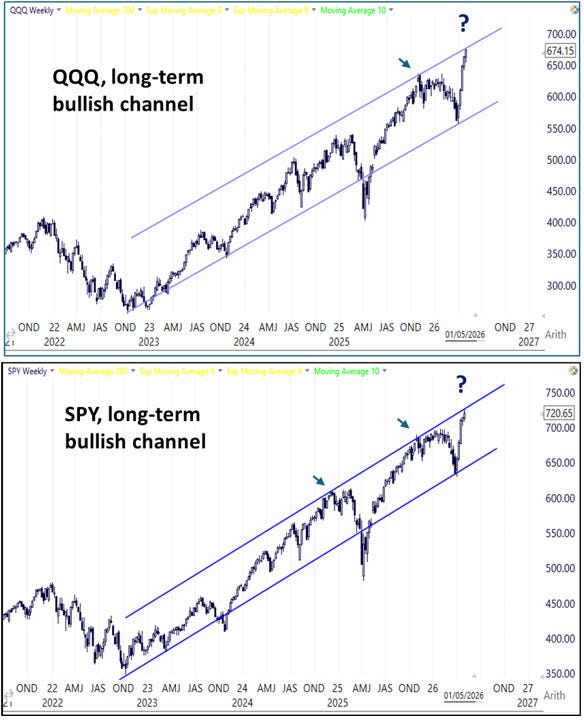

We noted in our last post that QQQ was overbought and edging into an area that may act as channel line resistance. No change this week. The resistance zone is more clearly visible on SPY.

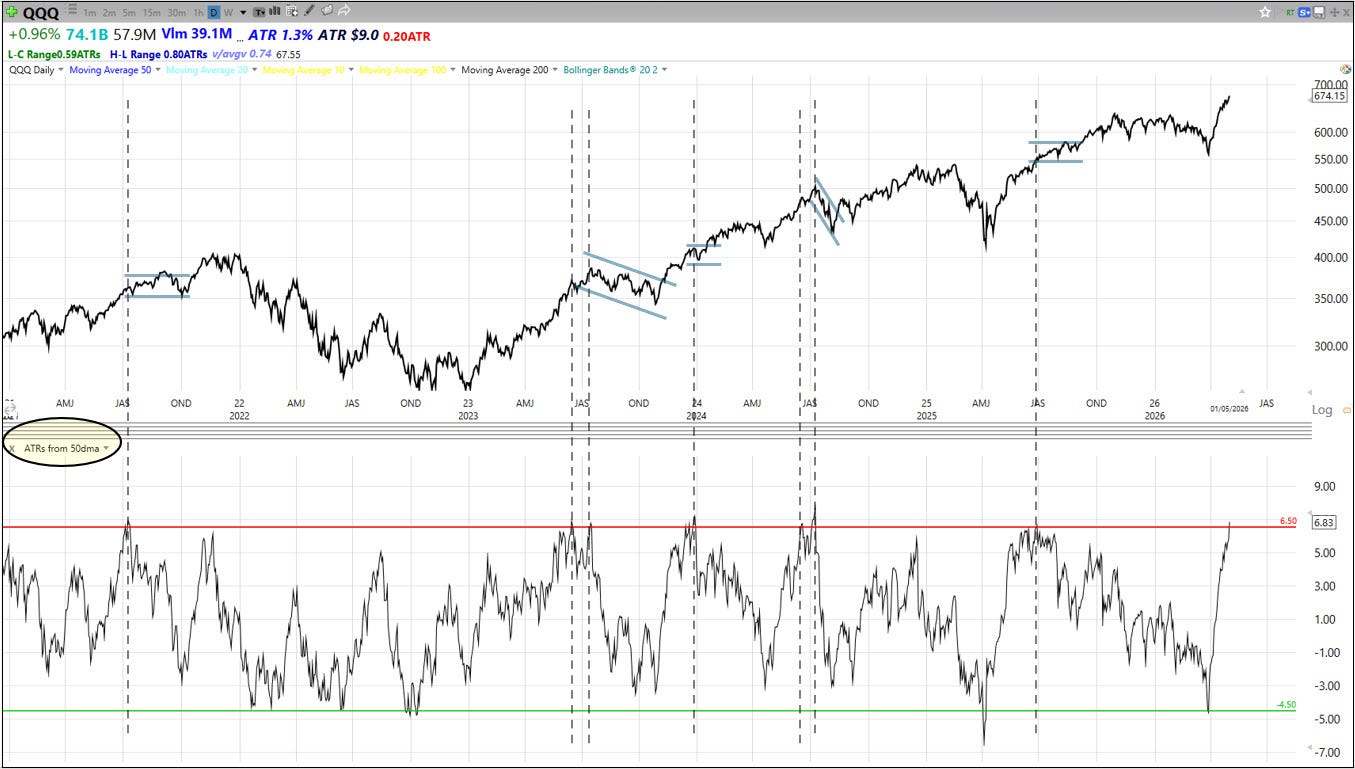

QQQ is now more than 6.8 ATRs above its 50dma. Readings above 6.5 ATRs (the red line in the lower panel of the chart below) have tended to precede periods of sideways consolidation or pullbacks. In the last 22 sessions, QQQ has risen +19%, equating to an annualised return of 713%, which is unsustainable longer-term. So the base case remains for a phase of consolidation before too long.

A final note on recent price action. While the rally off the low has been extreme, QQQ has shown itself capable of some stunning moves out of V-bottom lows in recent years, which have confounded market commentators (including myself at times). We can’t discard the right-tail scenario that we could be in a lock-out rally, in which case trying to fade momentum is a bad idea. As the excellent Walter Deemer notes…

The Fed

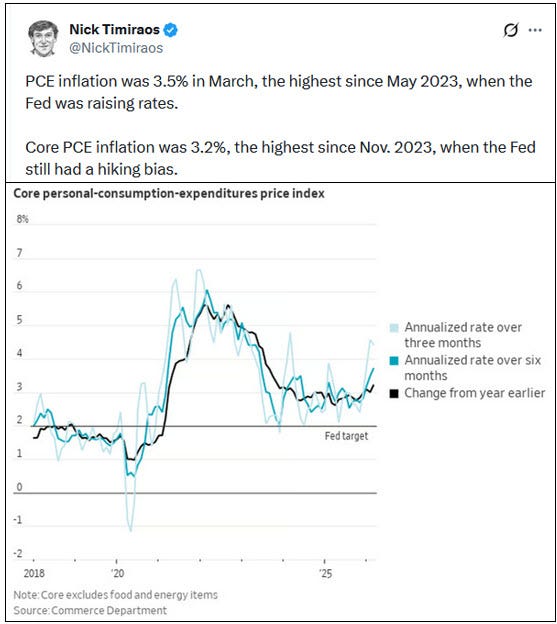

Trump’s observations that Iran is in a state of confusion because they don’t know who their leader is might just as well be applied to the FOMC, which is fragmenting into factions as it undergoes a leadership transition of its own. In his final FOMC appearance as Fed Chair before he hands over to Kevin Warsh, Jerome Powell had to explain the fact that no less than four FOMC members dissented at this week’s meeting. On the one hand, Trump’s dovish stooge, Miran, dissented in favour of a -25bp cut; on the other hand, three hawks, Kashkari, Hammack, and Logan dissented against retaining language in the statement that implies an easing bias. The FOMC is clearly shifting to a more hawkish stance in the context of the continuing energy price shock, and Powell, with one foot out of the door, was unable to build a common agreement around the statement language, which many members considered too dovish to keep. Good luck, Kevin Warsh, with building a consensus for a cut if the Strait of Hormuz remains closed while Core PCE is inching higher…

Markets & Narratives

1/ Iran

QQQ continues to look through the fog of war, pricing in a resolution that results in a reopening of the Strait of Hormuz and a normalisation of oil prices. A good exposition of that view comes from Citadel this week, here. In summary, Trump wants to pivot to domestic priorities ahead of the midterms, while Iran's leadership needs to rebuild to avoid internal unrest, and further escalation would cause catastrophic global economic damage with little strategic gain. The wildcard is whether, as was floated last week, America believes it can force a better deal, particularly with reference to Iran’s nuclear program, by engaging in further strikes against the Iranian regime.

A less optimistic view we picked up over the weekend comes from Sir Alex Younger, former head of British secret intelligence services, who observed that face-saving is an obstacle that is preventing the Iranian regime from making concessions to the US, whom they want to see humiliated. Moreover, they are unwilling to relinquish their nuclear capabilities because without them they are vulnerable to being deposed in a way that Kim Jong Un, by comparison, isn’t. That view suggests the Strait may remain closed for longer than the market currently reckons.

We hope the market’s view is correct and that a resolution is coming soon. However, there still remains the unpredictable prospect of further attacks against Iran, and/or a protracted Gulf cold war, either of which could preclude a rapid normalisation of energy prices.

One contrarian ray of light comes from the Economist’s cover, which suggests oil is going higher. Fingers crossed this turns out to be the magazine cover indicator at work.

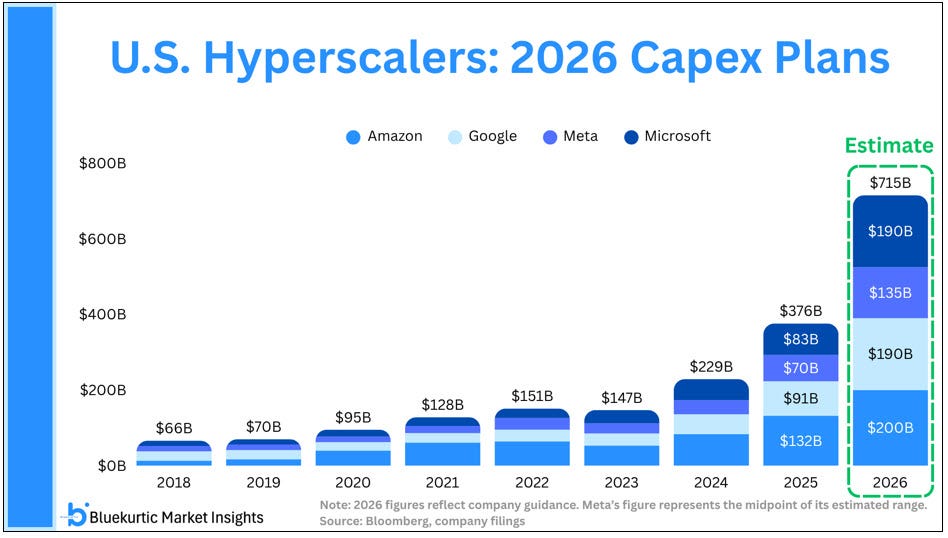

2/ AI capex

No sign of AI capex stalling. Post Wednesday’s hyperscaler earnings, 2026 estimated capex for the big four is now at $715b, with a view on $1tr in 2027. This juggernaut theme keeps trucking.

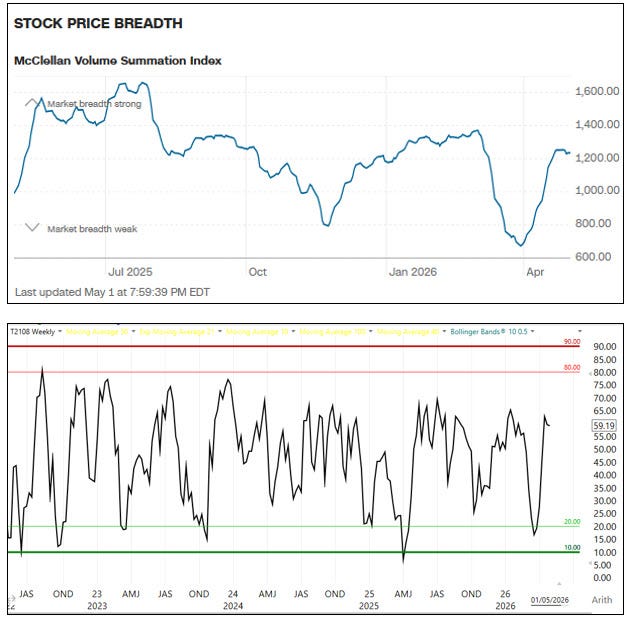

Breadth

Breadth has been OK - not much to write home about, but nothing too alarming. The McClellan Summation Index is tracking sideways, as is the % of stocks above their 40dma.

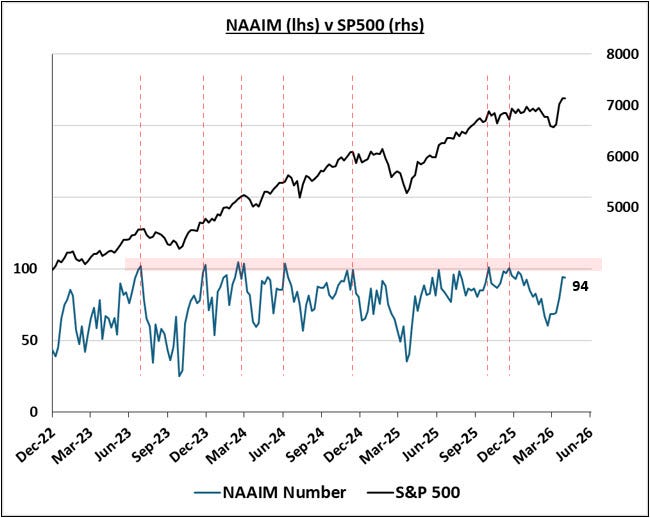

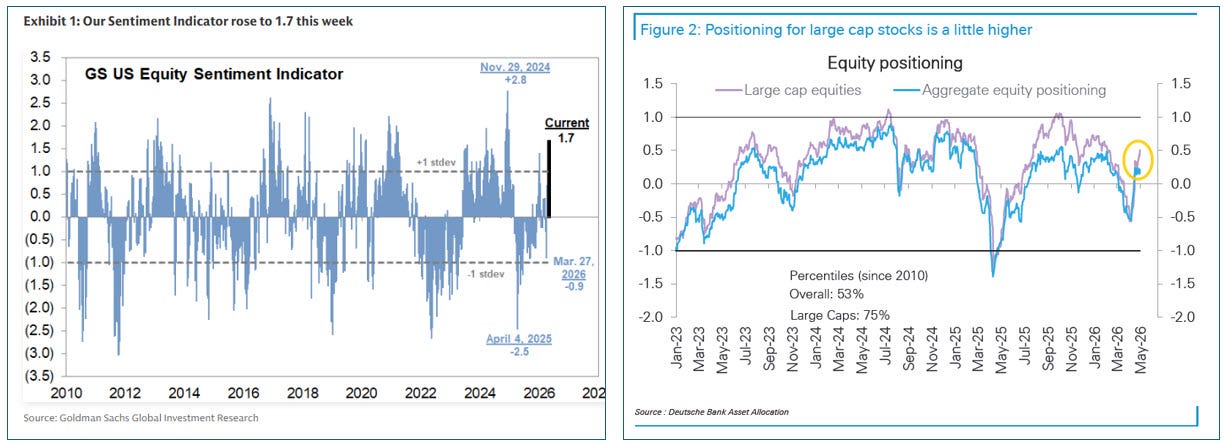

Sentiment & Positioning

Unsurprisingly, sentiment and positioning indicators have run up into bullish territory. The indicators I follow show positioning has become quite full, but isn’t too euphoric to be a contrarian bearish indicator just yet. It’s worth keeping in mind that in strong phases for stocks, sentiment can remain elevated for some time and is less of a helpful and immediate trade signal than excessively bearish sentiment at lows.

NAAIM is at 94 for a second week, still short of the danger zone above 100

Goldman Sachs US Equity Sentiment Indicator is pushing up into “stretched” levels, but DB’s survey is still neutral.

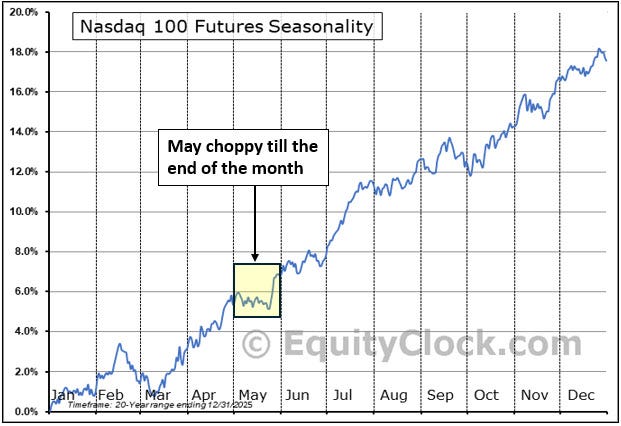

Seasonality

May is less seasonally helpful than April, but conditions improve towards the end of the month.

Summary

Price action: QQQ pushed up to new all time highs. Momentum is strong, but QQQ is overbought and pushing into channel resistance on the weekly chart, as is SPY. The longer-term primary trend is bullish.

The Fed: the FOMC is shifting in a hawkish direction, with three members dissenting in favour of dropping language in the statement that implies an easing bias. Warsh will have a difficult job building a consensus among FOMC members for rate cuts.

Markets & Narratives: 1/ Iran - stocks continue to price in a resolution to the Iran conflict and a normalisation of energy prices, but the outlook remains unpredictable. 2/ AI capex - hyperscaler earnings reconfirmed the AI theme.

Breadth: strong recovery has levelled off.

Sentiment & Positioning: returning to bullish, but not yet euphoric.

Seasonality: May is choppy but closes strong.

Key events next week: Iran news, earnings (Mon - PLTR; Tue - AMD; Wed - ARM; Thu - CRWV), ISM-NM (Tue), NFP (Fri)

View

Short-term: momentum strong, but price action stretched

Not a great deal of conviction short-term for an index trade in QQQ as it’s currently too overbought to chase, but momentum is too strong to fade. More broadly, conditions continue to favour breakout opportunities in leading stocks, but I’m remaining mindful that a period of chop or pullback might be coming in May, which is seasonally less helpful than April.

Long-term: cautious bullish

From a technical perspective, QQQ has done what it needed to do to reclaim its long-term primary bullish trend - it’s back at the top of its long-term channel and back above its moving averages.

From a fundamental perspective, the picture is more constructive than a few weeks ago. The negative narrative headwinds of Iran, private credit, and AI disruption are fading, while the positive tailwinds of AI capex and AI productivity are back. However, the oil price shock is not over yet, mid-term seasonality is not helpful till the back-end of the year, plus there is a growing risk of Fed dysfunction when Warsh takes over as Fed Chair.

Challenges and risks

Iran conflict and energy shock

OpenAI’s ability to honour its spending commitments

Weak mid-term seasonality

PS…

If you enjoy these posts and find them useful, please do share with colleagues, friends, or on social media - thank you.

Alex