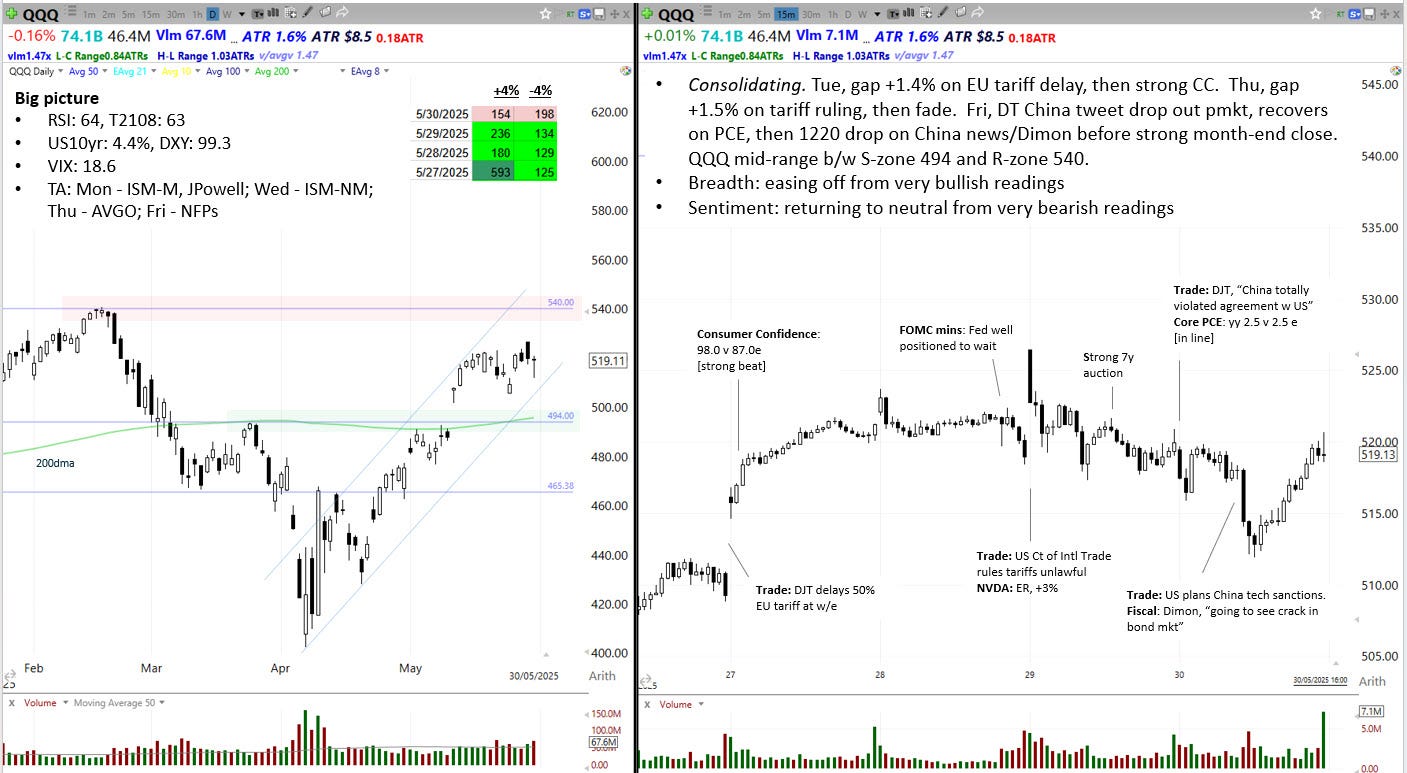

Price action

QQQ consolidated inside a tight 2.8% range this week. QQQ gapped up on Monday after President Trump postponed a 50% tariff on European imports until July. The move higher was helped along by a strong Consumer Confidence beat that suggests households are reacting positively to tariff de-escalation.

After the bell on Wednesday, the US Court of International Trade ruled that Trump does not have the authority to raise tariffs under the auspices of the IEEP and that many of the tariffs he has imposed are unlawful and must be reversed. This news brought a gap up on Thursday at the open. However, the gap faded as it became clear that Trump has plenty of other avenues available to pursue his agenda. Friday saw a -1.5% drop mid-session, then a +1.6% rally into the month-end close, leaving a bullish hammer candle on the daily chart.

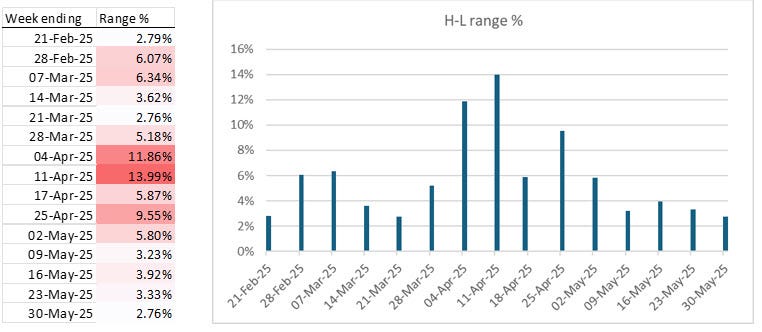

At 2.8%, this week’s high-low range was the tightest since QQQ began its descent in mid-Feb. Things are settling down.

Another measure of falling realised volatility is the 14d ATR, which is now down to 1.64%, a level consistent with easy bull market conditions. This evidence supports the idea that the market has shifted back to bullish mode.

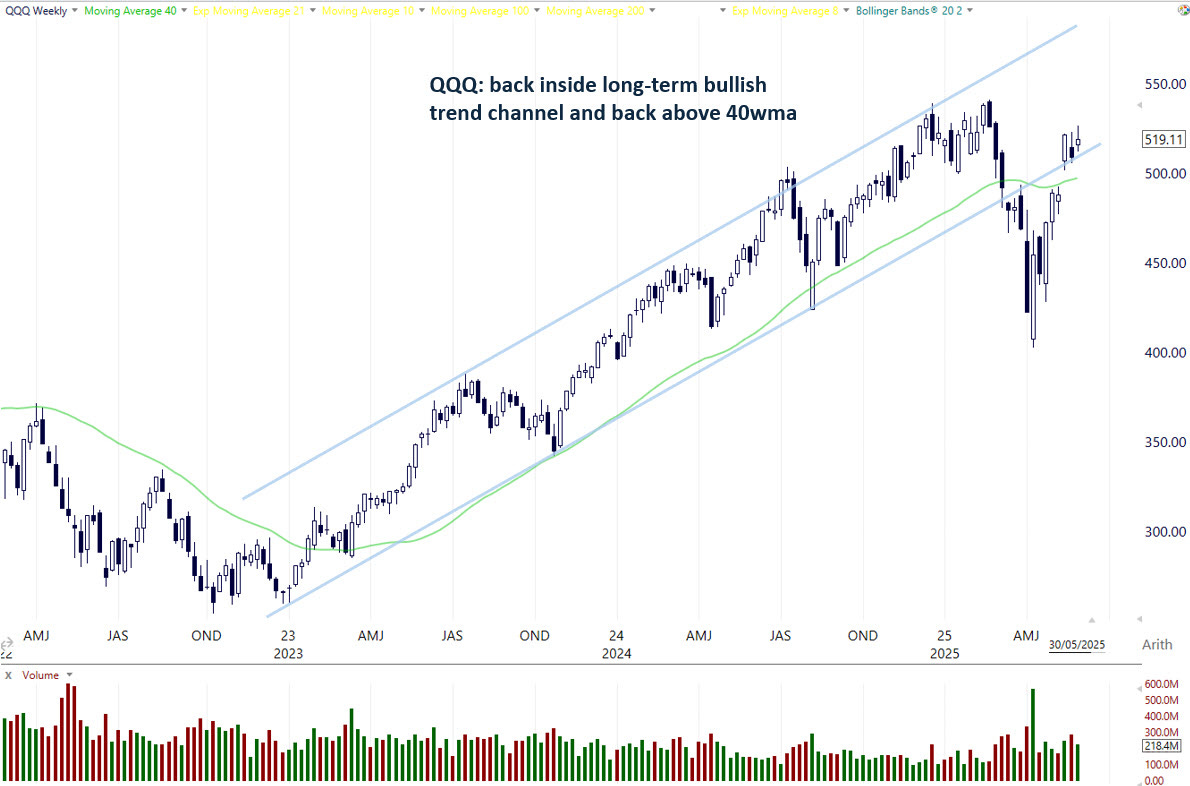

Further checks that we are back in a bull market come from the longer term weekly chart. QQQ has reclaimed its 40-week moving average (aka 200dma) and has held above it for three weeks. It has also regained the bullish primary trend channel that runs up from the 2022 lows. The longer QQQ can hold these levels while realised volatility ebbs away, the more comfortable institutions feel about rebuilding their equity exposures.

The Fed

This week we got the minutes of the FOMC’s May 6-7 meeting, which were released on Wednesday. The minutes reflect the messaging from all the Fed speakers we’ve heard over the last three weeks, namely the Fed remains in wait-and-see mode until the impact of tariffs becomes clearer, so don’t hold your breath for FFR cuts unless the job market tanks.

Markets and narratives

Trade headlines continue to move QQQ around, but their impact is diminishing. On Friday before the bell, Trump tweeted that China has “totally violated” the Geneva trade agreement, adding “so much for being Mr. NICE GUY!” This caused a small drop premarket, but it reversed after PCE came out in line. There was a larger -1.5% mid-session drop out, but once again buyers stepped in to close QQQ unchanged on the day. A headline of that sort would have caused a lot more trouble a few weeks ago, so what’s going on?

The usual trajectory of major macro narratives is that they coalesce on the horizon, then burst into significance, then eventually fade away (cf. GFC, EU sov debt, Covid, US regional banking crisis, Middle East, ad infinitum). QQQ is acting like the worst is past on the basis that (1) Trump understands if he pushes things too far the bond market will melt down, and (2) the business and finance establishment of America (ie, his backers) will push back hard. This dynamic was captured by the FT columnist Robert Armstrong, who calls it the TACO theory…

The risk, as ever, is that Trump goes loco. He cares deeply about his image and popularity and he is acutely aware of the viral power of a well-conceived meme (having successfully coined several of his own, such as “Sleepy Joe Biden” and “Crooked Hilary” etc). Will the TACO taunt trigger Trump’s vanity and prompt a re-escalation? We will see.

Breadth

After a sequence of bullish breadth thrusts that accompanied the bounce from the April lows, breadth has eased back. This doesn’t look alarming yet. The McClellan Summation Index has turned down, but is not falling very quickly.

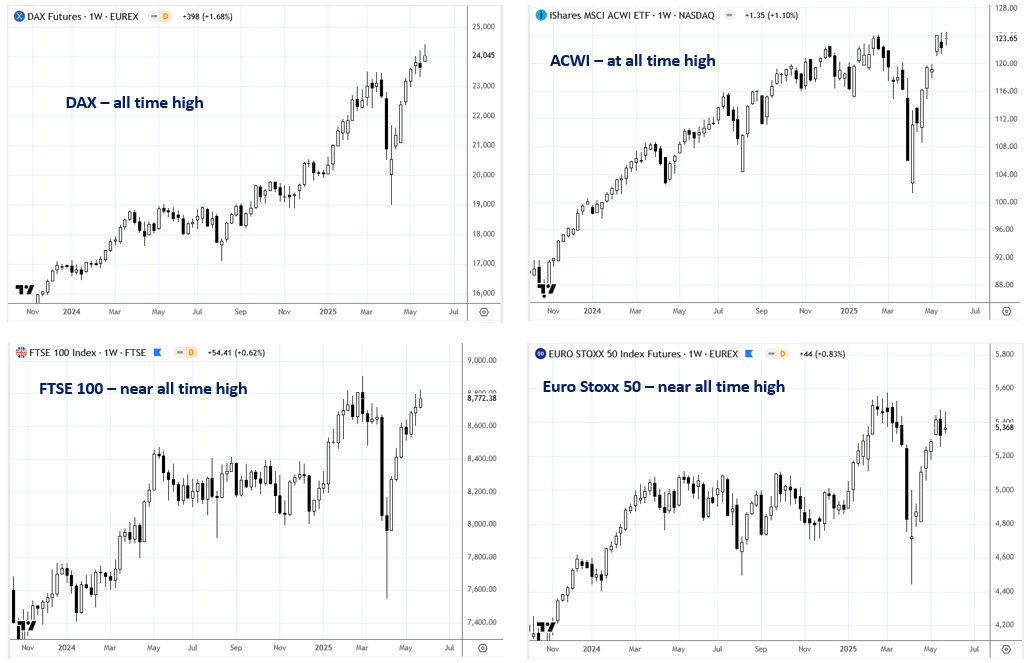

A study of breadth also contemplates global stock markets. There are a number of regions showing strength, which supports the bull market hypothesis.

Sentiment and positioning

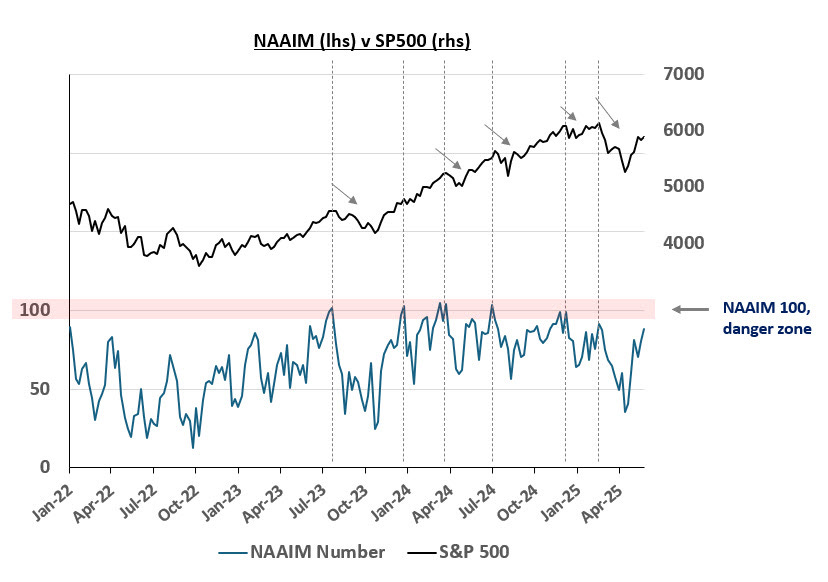

Last week we saw a clear turn in the sentiment surveys. The NAAIM is now back up at 88. A reading of 100 has been a fairly reliable indicator that a pullback or consolidation is coming. Still a bit to go, but one to monitor.

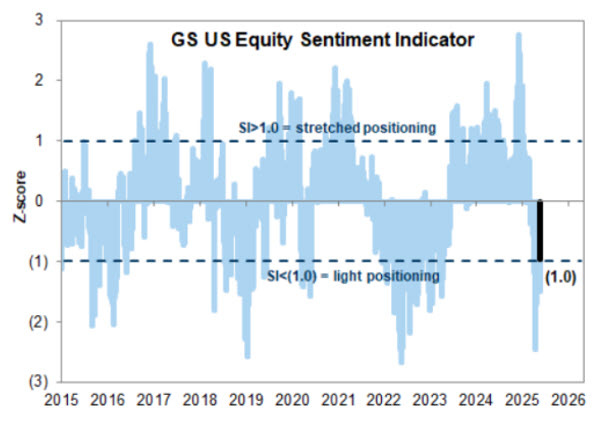

Surveys and indicators from the IBs still show hedge funds carrying light equity positioning, which suggests the pain trade for them remains higher. Here is Goldman’s US Equity Sentiment Indicator:

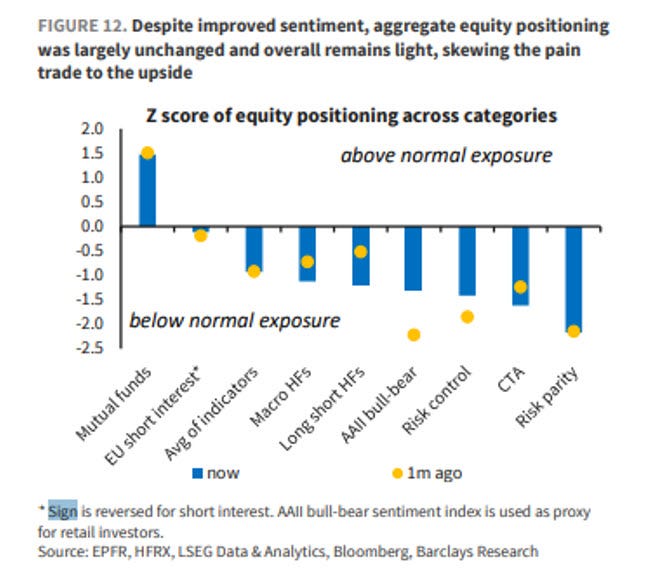

Barclays tell a similar story - equity positioning has lifted from the low, but is still below normal.

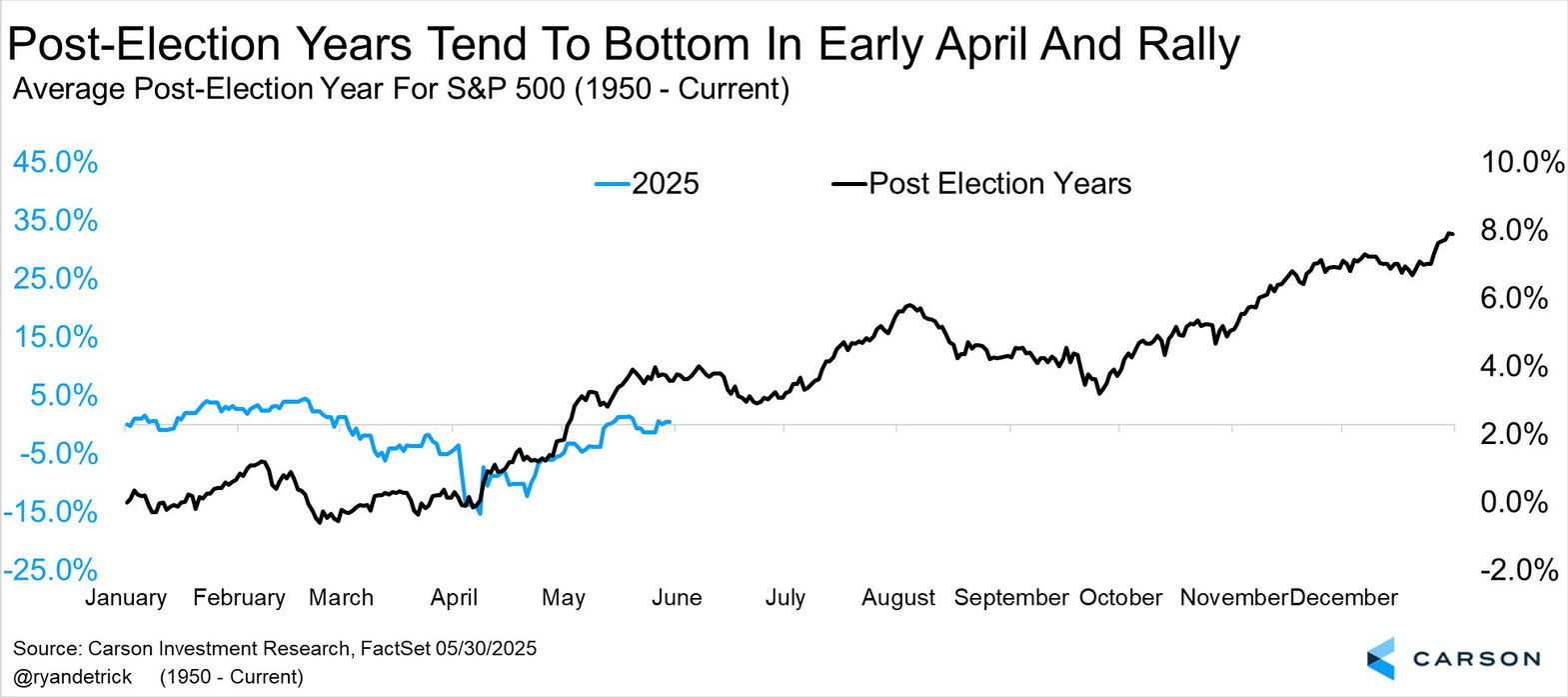

Seasonality

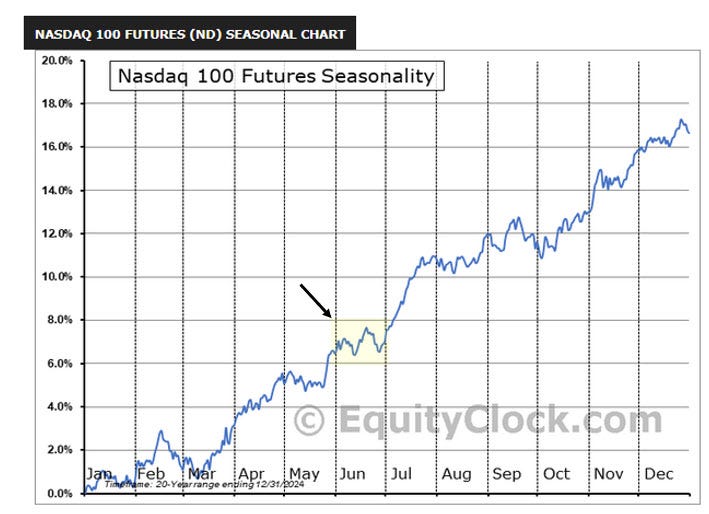

June can be a difficult month. The seasonality chart for the Nasdaq 100 shows, on average, a choppy sideways experience.

As for the Presidential cycle, this year is keeping somewhat close to the script. Note the sideways action in June before a bullish phase in July.

Summary

Price action: QQQ consolidated in a tight 2.6% range midway between resistance at 540 and support at 494. Realised volatility is consistent with bull market conditions. QQQ is holding its 200dma.

The Fed: the Fed remains in wait-and-see mode due to uncertainty about the impact of tariffs on inflation and jobs.

Markets and narratives: trade policy appears to be fading as a driver of price action, but Trump may re-escalate. US debt sustainability also remains a challenging theme.

Breadth: after a phase of very strong breadth since April’s low, breadth eased back for a second week. Some international stock indices suggest bull market conditions.

Sentiment: the NAAIM survey shows positioning is rising, but IB surveys suggest positioning remains light among hedge funds. Sentiment is returning to a neutral level after the extreme bearishness of April.

Seasonality: June is a choppy month for the Nasdaq 100. July is a bullish month.

Key events next week: Monday - ISM-M, JPowell; Wednesday - ISM-NM; Friday - NFPs.

View

Long-term: from a technical perspective, evidence is building that the bullish primary trend has resumed: (1) QQQ has reclaimed its 200dma and bullish trend channel. (2) Realised volatility is consistent with bull market conditions. (3) Recent economic data has shown the economy is holding up ok while soft data, such as consumer sentiment is improving. (4) Breadth was very bullish off the lows, evidenced by a sequence of thrust signals with good statistical records. (5) Investors still have work to do to rebuild equity exposures. However, from a fundamental perspective, the challenging and unpredictable trade war narrative is still in play, as is the US debt sustainability theme.

Short-term: neutral. Not much edge for a tactical trade mid-range between support at 494 and resistance at 540. A pullback to 494 could provide a decent long opportunity. June can be choppy.