QQQ weekly: 25 - 29 May 2026

Pressing higher

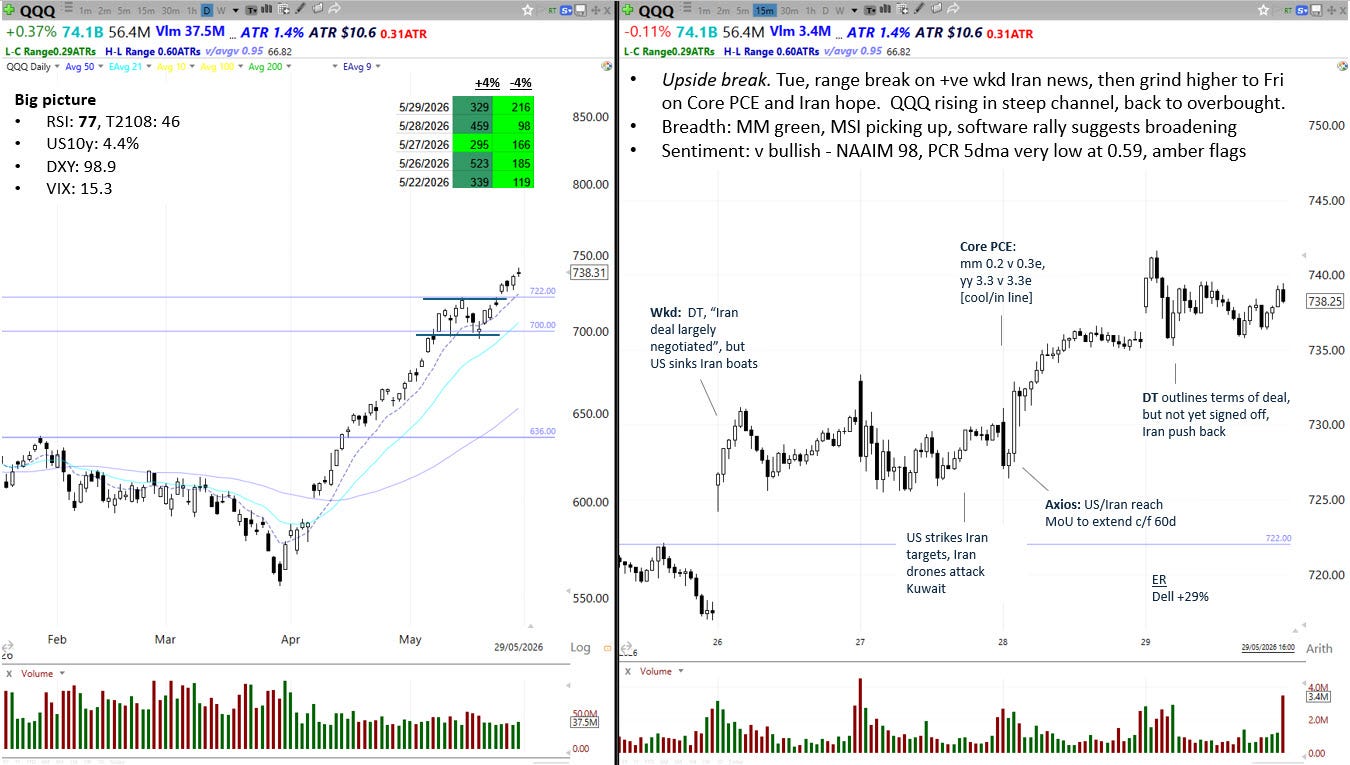

Price action

QQQ gapped up on Tuesday after President Trump suggested last weekend that a deal with Iran was “largely negotiated”. In doing so, QQQ broke out of its tight two-week range above 700. The move followed through to the upside as the week progressed, supported by an in-line/cool Core PCE reading on Thursday, and further optimism that a US/Iran deal could be concluded soon.

QQQ is back to an overbought condition. Its daily RSI is at 77, and it has extended 8.0 ATRs above its 50dma, and 10 ATRs above its 100dma. However, momentum is still strong, and the bullish channel from the 31 March low is intact (see hourly chart below). This conflict between overbought-ness and strong momentum makes it psychologically difficult to stay with it. However, the trend remains the trend until we see signs of a definitive break - the hourly chart below may help identify that moment whenever it comes.

The Fed

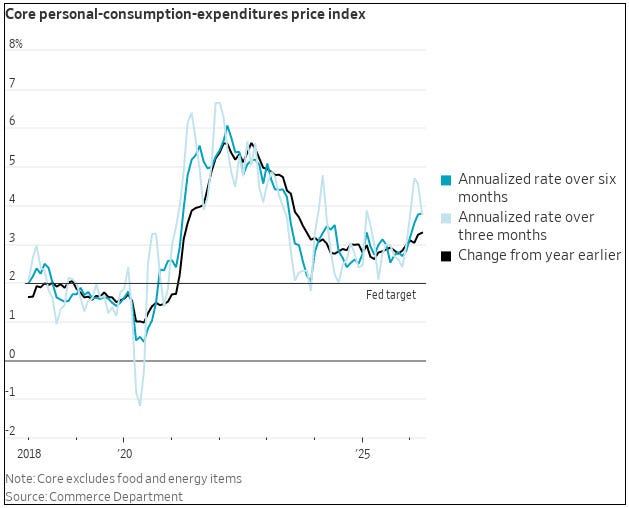

Core PCE came out on Thursday (chart below). It was something of a relief that the month-on-month figure rose only 0.24% in April, the mildest m/m gain in five months. However, the y/y figure for Core PCE is 3.3% and rising. Meanwhile, headline PCE looks ugly: six-month annualised is running at 4.8%, with three-month at 6.0%.

After the PCE release, we heard comments from a handful of FOMC members on Friday. Collectively they sounded modestly less hawkish than recent weeks.

Kashkari (Fri): premature to conclude Fed needs to raise rates immediately after April PCE report.

Paulson (Fri): policy mildly restrictive, inflation too high, but don’t see structural change to inflation - just series of shocks, inflation expectations still OK.

Bowman was the most dovish of this week’s Fed speakers. On Friday, the day after PCE, she defended retaining the controversial easing bias language in the March statement. She also explicitly referenced trimmed measures of inflation, which are not far off 2%. Kevin Warsh also flagged trimmed mean inflation metrics at his nomination hearings as his preferred measure of inflation. Look out for this topic at the June 17 FOMC meeting.

Bowman (Fri): supported keeping easing bias language in March statement, progress on inflation has stalled but trimmed measures are near 2% target, Fed can look through energy shock if it remains credible on policy.

Markets & Narratives

1/ Iran

The deal/no-deal headlines continued this week, with talks progressing against a backdrop of naval skirmishes and drone attacks. Stocks and oil are both behaving like a deal is in the bag, so a disappointment could trigger a pullback in QQQ.

2/ Software

For much of 2026, software has been viewed as the sector most vulnerable to disruption by AI technology. The bear thesis runs that leading AI models are able to reproduce software products cheaply, and so enterprise customers will pivot away from expensive SaaS programs to cheaper products they can develop in-house. However, over the last month the narrative has become more nuanced, with the market beginning to discern some AI winners in the space. We saw notable high volume breakouts among select software stocks on Thursday and Friday. Is this the beginning of a bullish rotation from hardware leaders to software laggards?

Breadth

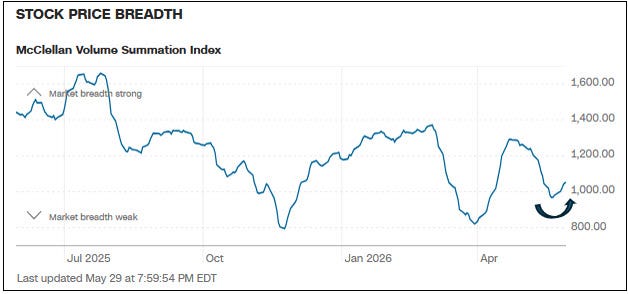

Breadth was good this week. The McClellan Summation Index appears to have put in a turn and is now moving higher. The Market Monitor showed a healthy number of stocks +4% each day this week. Meanwhile, equal-weighted versions of SPY and QQQ both closed at all time highs.

Sentiment & Positioning

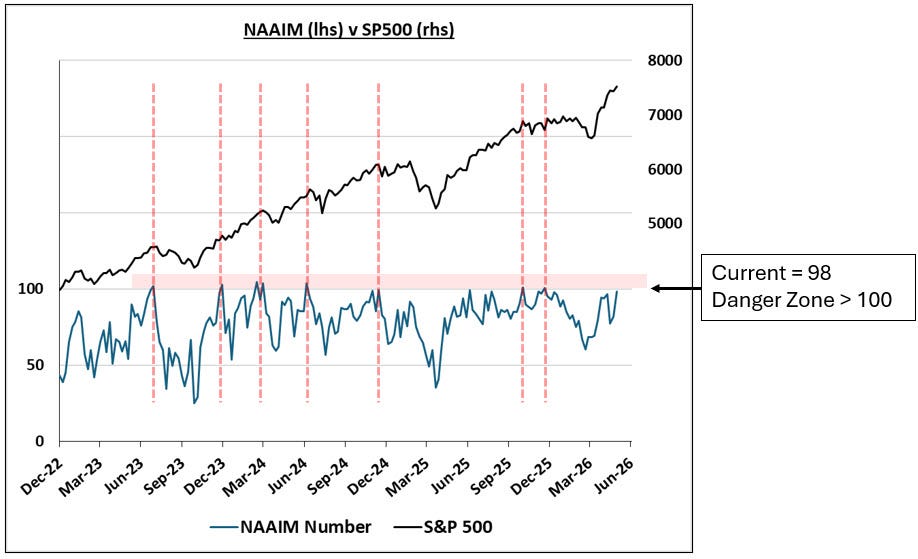

This week, the NAAIM Exposure Index jumped to 98, just short of the “too bullish” danger zone above 100. One shouldn’t place too much emphasis on any single indicator, but since this bull market began in late 2022, each time NAAIM has broken 100 (red dotted lines in the chart below), we have seen a phase of sideways consolidation or pullback in US indices. If stocks push higher again next week, it wouldn’t be surprising to see a push through that key level.

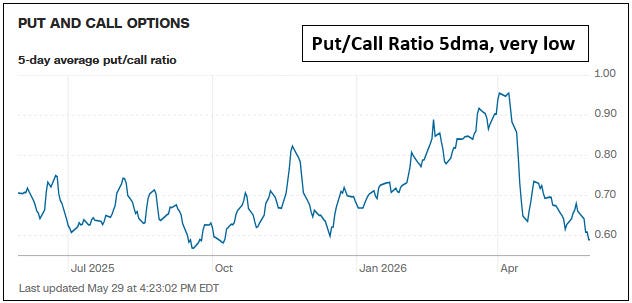

The options market also provides evidence of giddiness. The Put/Call Ratio 5dma is now below 0.6, which is an amber flag.

The NAAIM and PCR are both suggesting conditions are setting up for a pause or reversal in QQQ. However, sentiment and positioning indicators are less precise at market tops than bottoms.

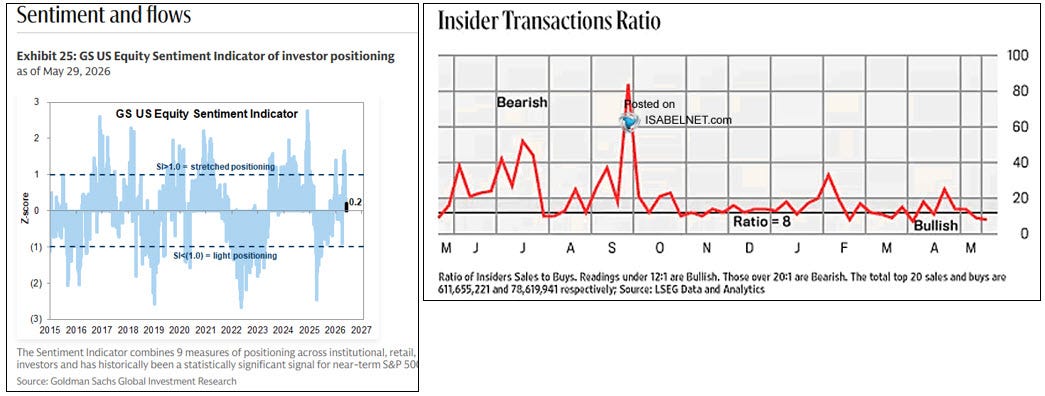

We also have to acknowledge that many indicators are not in euphoria territory yet, so it may take a bit longer before we get a clear red flag from market psychology. The GS US Equity Sentiment Indicator remains in neutral territory, the Insider Transactions Ratio shows insider buying, and the AAII survey shows more Bears than Bulls.

Seasonality

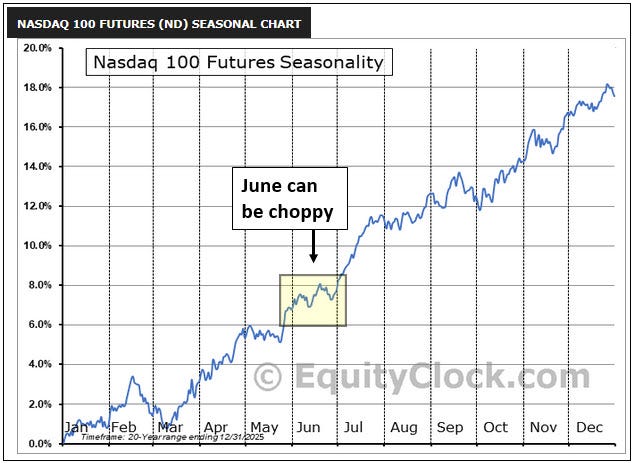

In our last two posts, we’ve highlighted the seasonal weakness in the 4-year Presidential Cycle during the middle phase of midterm years. As for the straight 1-year seasonal cycle (shown below), June can be choppy, with a weak second half of the month.

Summary

Price action: QQQ broke out of a tight two-week range and followed through to the upside in a steep bullish channel observable on the 1-hr chart. It is short-term overbought again. The long-term primary trend is bullish.

The Fed: Core PCE was not as bad as feared, and FOMC speakers were somewhat less hawkish than last week.

Markets & Narratives: 1/ Iran conflict - ping-pong headlines continue, market is pricing in resolution. 2/ Software - notable high volume breakouts this week.

Breadth: solid again, MSI has turned up.

Sentiment & Positioning: evidence of euphoria emerging in NAAIM and Put/Call Ratio, but no clear signal across the board.

Seasonality: the Nasdaq 100 1-year seasonal cycle and seasonality composites that include the US Presidential Cycle suggest June may be choppy.

Key events next week: Iran news, ISM, NFPs, earnings - AVGO

View

Short-term: going with the flow, but on deck with life jacket on

Last week our base case was for an upside breakout, which we got this week. Momentum is still strong and breadth is helpful, but I wonder if June might be a bit less easy? Yes price momentum and breadth look good, but QQQ is overbought again, spots of euphoria are beginning to emerge, and seasonality is less helpful. Iran also remains undecided. Warsh’s debut is not far off - the next Fed meeting is on 17 June.

Conditions for swing trading continue to be very favourable. This week, there were excellent breakout setups in NOW, IBM, ORCL, and MU. I plan to continue taking swing setups as long as they keep working and the indices hold up. A downside break of QQQ’s bullish channel on the hourly chart could act as an early warning of deteriorating trading conditions.

Long-term: cautious bullish

From a technical perspective, QQQ is trending in a long-term primary bullish channel in play since late 2022. It sits above its long-term moving averages, which are sloping upward. The bull market is very much intact.

From a fundamental perspective, there are plenty of tailwinds supporting the market. Fiscal support continues, with the US running a large deficit that stimulates the economy, which is strong; corporate earnings have been stellar; the AI theme continues to suggest trillions of annual capex spending ahead; and, negative headwinds from Iran, private credit, and AI disruption have eased off.

My long-term view is bullish, but I can’t help but retain a little caution until the Strait of Hormuz is settled, bringing energy prices, inflation, and bond yields down, and lifting pressure on the Fed to hike later this year.

Challenges and risks

Iran conflict and energy shock - rising inflation and bond yields, pushing the Fed to a hawkish pivot.

Fed dysfunction under new Chair Warsh.

Weak midterm seasonality.