QQQ weekly: 23 - 27 Feb 2026

Range break coming?

Price action

This week, QQQ chopped around between 600-618 as tensions in the Middle East continued to build. Towards the end of the week, evidence accumulated that America was about to deploy the forces it has amassed against Iran. News came that America and its allies were evacuating personnel from bases in the region and instructing its citizens to leave, which was the pattern that preceded last summer’s strikes against Iran’s nuclear facilities. From Wednesday onwards, White House comments became increasingly hawkish, oil prices lifted, a bid for USTs emerged, and we saw a spike in the Pentagon pizza index (not serious / but seriously). The latest strikes, which started yesterday, are significant, but they cannot be considered a surprise.

QQQ may finally now have a catalyst to break its frustrating five and a half month range. We will see whether that breakout is to the downside or the upside.

The Fed

After somewhat hawkish minutes last week, this week brought a range of views. Four speakers spoke in favour of holding rates steady:

Collins (Wed): likely to hold rates for some time, policy mildly restrictive, near neutral

Musalem (Wed): inflation 1pp above target, policy now neutral

Barkin (Wed): inflation still above target, policy well-positioned

Schmid (Wed): more work needed on inflation

Two speakers intimated further cuts before too long:

Waller (Mon): March decision a coin toss between cut and hold

Goolsbee (Tue): optimistic on more cuts this year

Miran returned to calling for immediate cuts, albeit now only 100bps:

Miran (Thu): want 100bps cuts this year, inflation stable, AI profoundly disinflationary, banks over-regulated, no problems in private credit yet

If we see a spike in oil prices next week, look out for Fed commentary on how that impacts their thinking on inflation. Most likely they sit on the fence for now, but hawkish commentary would be a headwind for QQQ.

Markets & Narratives

1/ Iran

As we write this, we know (1) America and Israel finally attacked Iran, (2) Khamenei has been killed, (3) Iran is in the process of appointing a new leader and/or its government is fracturing, (4) Iran has launched aerial attacks against its neighbours, and (5) Iran may close the Strait of Hormuz.

It’s impossible to know where this story will be when cash markets open on Monday. One should keep an open mind and be prepared for moves that may appear counterintuitive. As we noted in last week’s post, the put call ratio for US stocks has been elevated, suggesting investors were well-hedged going into this event. Now we have greater clarity, investors may unwind those hedges, which would put upward pressure on QQQ in the short-term.

To illustrate with an example of a counterintuitive short-term move, the chart below shows my notes of the Nasdaq 100 intraday price action on Thu 24 Feb 2022. That was the day Russia launched its attack on Ukraine. Note the gap down, then the disorderly short squeeze +7% as the day unfolded.

It’s been instructive to watch Bitcoin over the weekend, which has a positive correlation to QQQ. BTC initially dropped -3.5% on the news of the strikes on Iran, then bounced. Meanwhile, IG’s weekend spread betting markets don’t suggest a big move in US stock indices.

However, keeping an open mind also means being prepared for downside on Monday. 582 looks like a decent area of support for QQQ, near its 200dma. Should that fail to hold, keep in mind Paul Tudor Jones’s dictum… “nothing good happens below the 200dma”. A big spike in oil could cause trouble. IG’s Weekend WTI market shows a jump to around $75.

2/ Private credit

Early in my career, I had the good fortune to interview John Paulson when I was doing investment due diligence on the Paulson Credit Opportunities Fund, which did very well shorting subprime mortgage-backed securities into the GFC (we made an investment). Paulson explained his rule of thumb was to ignore news stories denominated in billions of dollars, but when people start talking trillions, then pay attention. The private credit market reached $3tr last year, so we should pay attention.

There were more bad headlines this week. Hopefully what we are seeing are isolated instances of crap lending rather than something systemic, but it’s not going in the right direction.

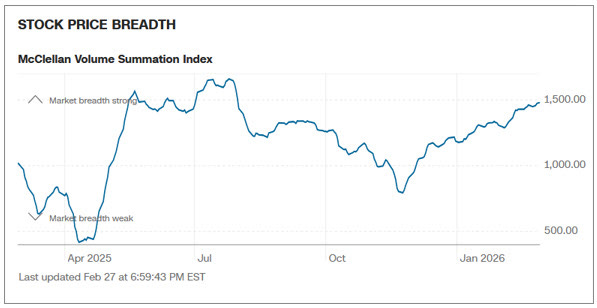

Breadth

Still holding up OK. The McClellan Summation Index is still grinding higher.

Elsewhere, RSP closed near its all time high, while QQQE closed less than 3% from its all time high. Advance-Decline Lines are still rising. That’s constructive.

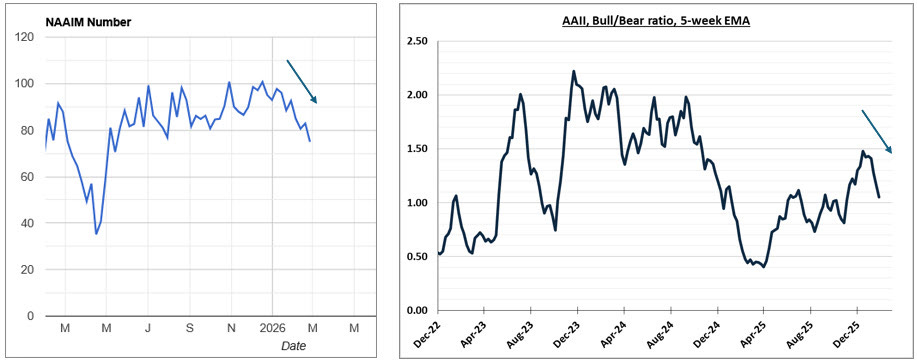

Sentiment & Positioning

AAII and NAAIM metrics both showed deterioriating sentiment this week, which is contrarian constructive for QQQ. A real pick up in panic would help set up conditions for a leg higher in QQQ. We’re not quite there yet.

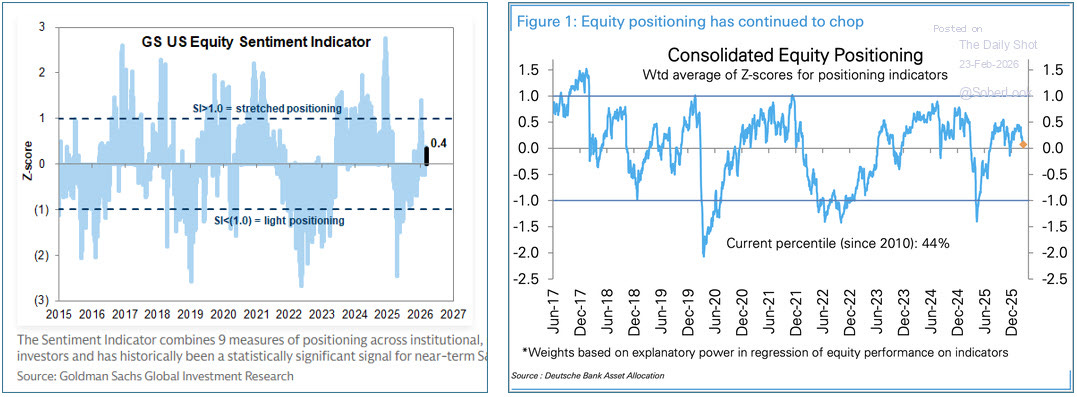

BofA’s Bull & Bear indicator has flagged a sell signal for a few weeks. However, Deutsche Bank’s and Goldman’s indicators are neutral, which suggests dry powder to chase stocks higher.

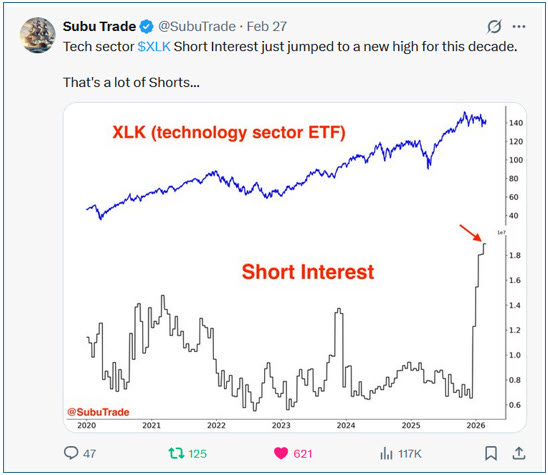

Elevated short positioning in XLK suggests potential for a squeeze in tech if momentum develops.

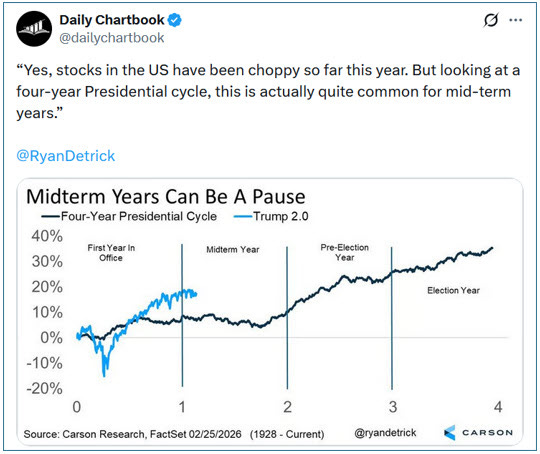

Seasonality

As we move from February to March, here is a reminder that the midterm year of the Presidential cycle is the lemon. 2026 is following that pattern so far.

Summary

Price action: QQQ continued to chop around in its range. On Saturday, America and Israel launched strikes on Iran, which may precipitate a breakout of QQQ’s range, either to the upside or downside. The long-term primary trend is bullish, but a break below the 200dma could suggest a change.

The Fed: FOMC speakers provided a mix of views about further cuts this year.

Markets & Narratives: 1/ Iran. Weekend markets in BTC and US indices do not suggest a big gap down on Monday, but weekend oil markets are less rosy. 2/ More problems are emerging in private credit.

Breadth: still OK

Sentiment & Positioning: AAII and NAAIM indicators show sentiment deteriorating, while investment bank surveys are neutral (DB and GS), with the exception of BofA, which continues to flash a sell signal. Recent demand for puts over calls has been more characteristic of a local bottom than a top. Elevated short interest in XLK provides fuel for a squeeze.

Seasonality: the midterm year of the Presidential cycle is the weakest of the four.

Key events next week: Iran headlines, ISM surveys, NFPs, private credit headlines.

View

Short-term: Iran newsflow means a wide range of outcomes are possible short-term, either bullish or bearish. I’m open-minded for a melt-down if headlines deteriorate and oil spikes, or melt-up if news improves and investors close out hedges and shorts in a hurry. Developments in private credit are growing in significance.

Long-term: the primary trend is still bullish, but the evidence is weakening at the margin.

Technical evidence

QQQ is trending higher above its upward-sloping 200dma. However, a break below that moving average could suggest a trend change.

Fundamental evidence

The Fed is gradually cutting its policy rate. However, a small number of FOMC members have recently begun to entertain the idea of hikes if inflation does not continue to fall.

Fiscal stimulus from Trump’s spending bill.

US economy is strengthening, supporting earnings.

Challenges and risks:

Geopolitical uncertainty around Iran.

Uncertainty relating to AI:

AI-disruption, OpenAI’s ability to honour its spending commitments, NVDA’s monopoly, capex depreciation, hyperscaler credit spreads, skepticism relating to scaling assumptions.

Private credit problems.

Fed independence.

PS…

If you enjoy these posts and find them useful, please do share with colleagues, friends, or on social media. Thank you.

Alex