QQQ weekly: 22 - 26 Jun 2026

Choppy range continues

Price action

On Monday, QQQ hit resistance at the top of its range and couldn’t get through, confirming the presence of sellers in that area. QQQ gapped down on Tuesday, a large -3%. The cause was an overnight puke in Asian stocks, particularly in the KOSPI, which is dominated by memory giants SKHynix and Samsung (together, around 50% of the index). Overnight, the KOSPI fell -11%, with SKHynix -16% and Samsung -11%. This fed through to the leading AI stocks in the US, with SMH -7% on the day, and DRAM -14%.

After hours on Wednesday, MU reported blow-out earnings, beating quarterly EPS by 22%, revenue by 16%, and next quarter’s consensus revenue estimate by 15%. On Thursday morning, MU gapped up +18%, which, along with an ok PCE print, produced a +2% gap up in QQQ. However, these moves couldn’t hold - a wave of heavy selling came through in the first 30 minutes of the session, with MU dropping -9%, and QQQ -3%. Just as on Monday, sellers had been waiting to sell into strength. After a very choppy week, QQQ closed quietly on Friday at the bottom of the recent range, just above the 50dma and the major round number 700.

The Fed

There were three speakers of note this week, all of whom continued the hawkish tone of the last few months.

Goolsbee (Mon): core inflation still too high and going the wrong way

Kashkari (Fri): one hike pencilled in for 2026

Williams (Thu): given elevated inflation, imperative Fed restores it to its 2% target, current policy well-positioned to do that, pushing expectation for inflation to hit 2% from 2027 to 2028

On the face of it, these were consistent with the Fed’s latest median FFR dot, which suggests a hike by the end of the year, and consistent with market pricing too, which also suggests a hike. However, note that John Williams, the influential Vice Chair, stated that current policy is “well-positioned” to get inflation back to target (albeit over a longer time frame than he previously thought), implying he doesn’t think a hike will be needed.

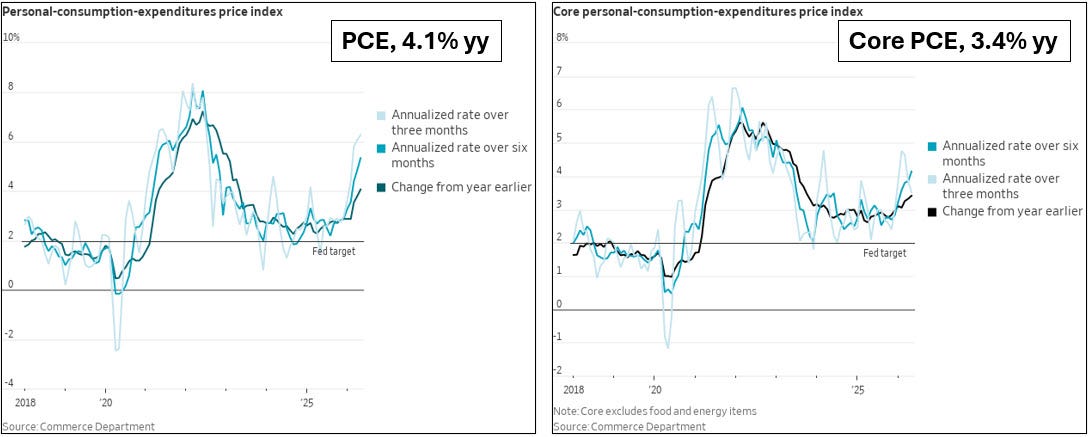

As for data, PCE was released on Wednesday and it’s still going up (see below for headline and core charts). However, energy prices are falling rapidly with the reopening of the Strait of Hormuz, raising hopes that inflation may be peaking. Furthermore, inflation expectations are still broadly anchored: consumer inflation expectations, as measured by the University of Michigan Survey, have not spiralled; and market-based measures of inflation expectations are back where they were prior to the war, as measured by 10y inflation swap rates.

However, if the reopening of the Strait of Hormuz stalls and if inflation fails to roll over soon, the charts like the ones below could develop into a significant headwind for QQQ. The next data points in the story will be Warsh speaking at the ECB symposium at Sintra on Wednesday, and NFPs on Thursday.

Markets & Narratives

1/ Iran

Despite the “Memorandum of Understanding” between American and Iran, there are reports of more hostilities this weekend. Weekend spread betting markets don’t suggest a big move at Monday’s open, but obviously things could change between now and then.

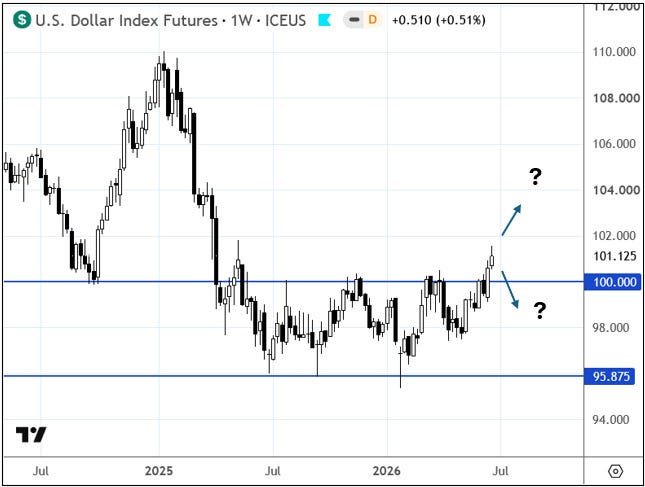

2/ USD

Still watching the dollar. It is not a huge coincidence that recent dollar strength has coincided with choppiness in QQQ.

Breadth

Breadth picked up on Friday, with a strong showing in the Market Monitor, which showed more than 800 stocks up +4% on the day. While semiconductors and memory stocks have chopped up into a messy range, and while the MAGS have struggled, other sectors are looking good. Healthcare (XLV), biotech (IBB/LABU), and insurance (IAK) all made nice moves, and small caps (IWM) made a new all time high. IWM’s consolidation breakout has been acting well, rising in a clear channel (see below). The measured move target is around 328, though note it’s extended in the very short-term and is a difficult one to trade.

Sentiment & Positioning

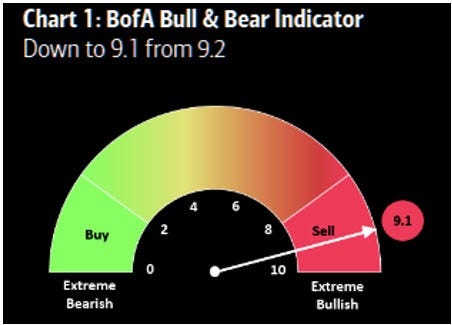

Last week we pointed out that Bank of America’s Bull & Bear indicator had moved into sell signal territory. This one can fire “early”, but it was a useful signal earlier in the year.

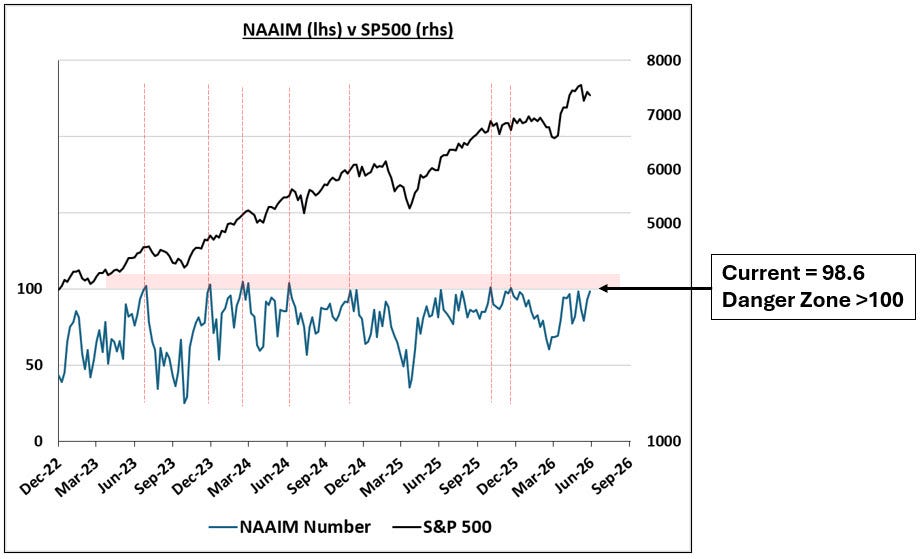

The NAAIM also jumped to 98.6 this week, a whisker away from the 100 danger zone. Since the rally began in 2022, whenever the NAAIM has reached 100, a pullback or sideways consolidation has not been far away. (These moments are marked in the chart below by the vertical red dotted lines). This is an amber flag, almost red.

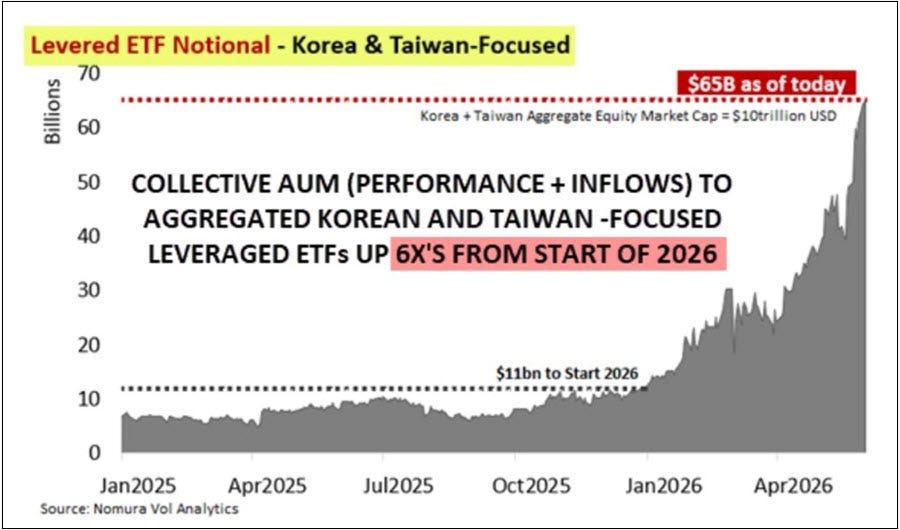

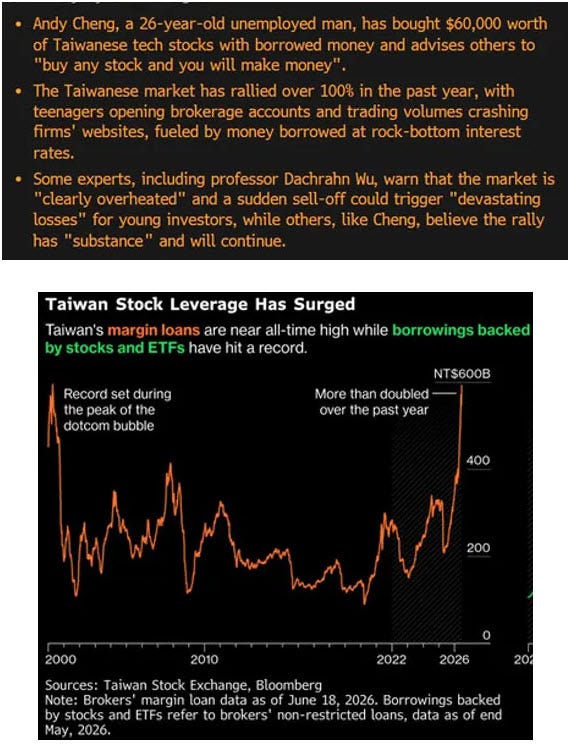

A further red flag is the very large recent rise in the AUM of leveraged ETFs, particularly those related to Korean and Taiwanese stocks, which are heavily skewed to AI names. The problem here is not the fundamentals of stocks like TSMC, Samsung, and SKHynix, rather the problem is the leveraged nature of the money chasing them, which amplifies volatility (as we saw this week).

There are also signs of mania emerging in Asia tech stocks. It’s hard to know how to weight these anecdotal snippets, because it’s hard to know how widespread what they describe has become. Trend following is all about going along with price until price gives you a clear message that the party is over, but stuff like this suggests the party is now in full swing…

Seasonality

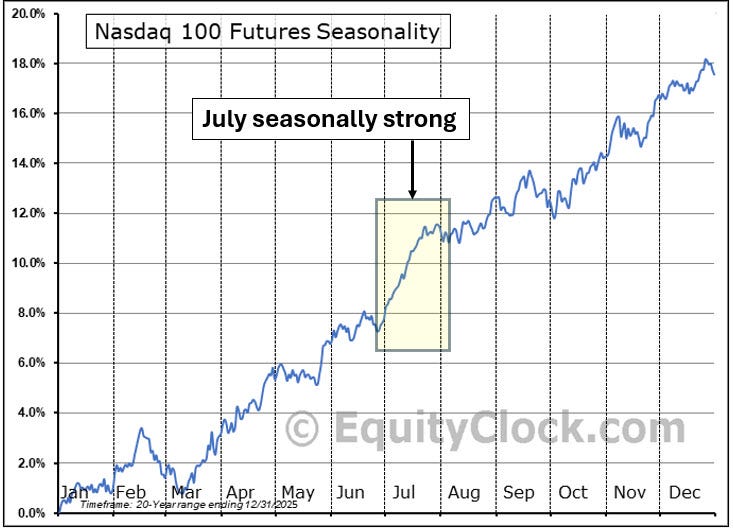

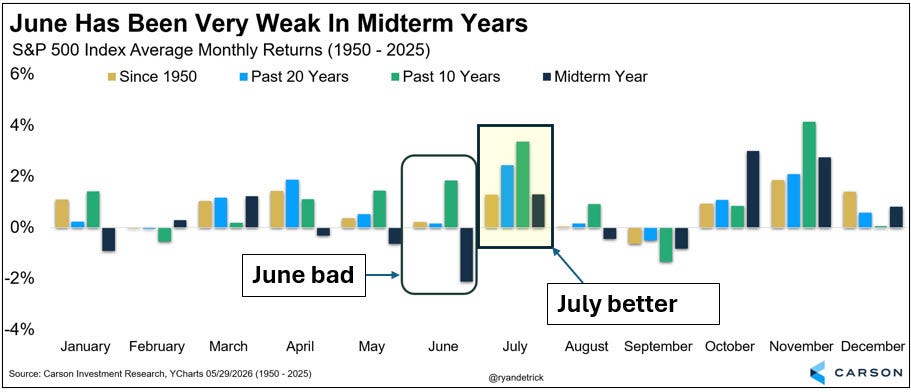

As we move from June to July, seasonality improves.

However, note how July is much less bullish for US stocks in midterm years compared to all July months of the last 10 and 20 years.

Summary

Price action: QQQ continued to chop around inside a wide 50-point range. Moments of strength on Monday morning and especially Thursday morning after Micron’s earnings were met with concerted selling. The long-term primary trend is bullish.

The Fed: FOMC speakers sounded hawkish. Core PCE is still rising, but energy prices are falling following the supposed cessation of hostilities between America and Iran. Inflation expectations remain anchored. Warsh speaks again on Wednesday.

Markets & Narratives: 1/Iran - another flare up this weekend. 2/ USD - looks like it might be breaking out, further strength would be a headwind for QQQ.

Breadth: breadth improved on Friday. Sectors outside tech performed well, with IWM hitting a new all time high.

Sentiment & Positioning: we are spotting more evidence of euphoric sentiment and positioning, either in indicators, surveys, or anecdotal evidence. The NAAIM is almost at 100.

Seasonality: July is seasonally strong, but much less so in midterm years.

Key events next week: Wed - Warsh speaks at Sintra; Thu - NFPs

View

Short-term: more chop

In my last post I noted I was cautious short-term, and that the recent choppy price action would likely continue, which is what we got. I don’t much like this erratic up-and-down at the highs because it looks like topping action. Although seasonality improves into July, and although realised volatility has been easing back, it’s not encouraging that more evidence of “too bullish” sentiment is starting to appear. Last week, the BofA indicator was the only piece of evidence, but now we have the NAAIM almost at 100, plus anecdotal evidence that leveraged ETF buyers are pushing their luck. Add in more Iran friction, plus USD strength. If QQQ does make a new all time high next week (not base case, but possible), then that could push NAAIM above 100, which would be a clearer red flag. I’m trading quite cautiously until we have a clear sentiment and positioning re-set.

Long-term: cautious bullish (no change to my long-term view this week)

From a long-term technical perspective, QQQ is trending in a bullish primary channel in play since late 2022. It sits above its long-term moving averages, which are sloping upward. The bull market is intact.

From a fundamental perspective, there are tailwinds supporting the long-term bull market. Fiscal support continues, with the US running a large deficit that stimulates the economy, which is strong; corporate earnings have been stellar; the AI theme suggests trillions of annual capex spending ahead.

While I’m bullish from a long-term perspective, I’m somewhat cautious on a 6-month view on the basis of elevated inflation and unhelpful midterm seasonality until Q4.

If you find my posts useful, please do share with friends and colleagues.

See you next week,

Alex