QQQ weekly: 2 - 6 Feb 2026

Range holds

Price action

From intraweek high on Tuesday to intraweek low on Thursday, QQQ fell -5.6%. The move lower was helped along by uncertainty around America’s plans for Iran, and a flurry of weak jobs data. The support zone at the psychologically important round number 600 held, as we suggested it might last week. On Friday, QQQ bounced as news emerged that US/Iran talks had not fallen apart.

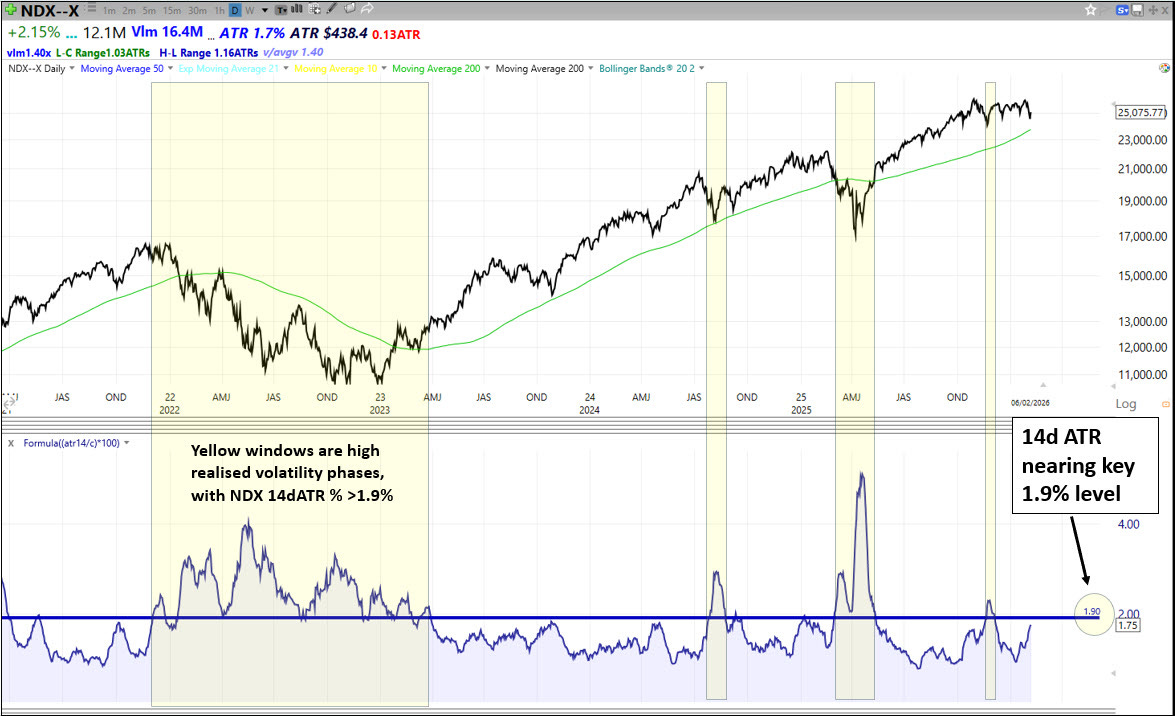

QQQ remains stuck in the range that has been in play since late September. The confluence of longer-term bullish factors still suggests a break higher could be on the cards, namely fiscal and monetary support, along with a strengthening economy and a decent earnings season. However, note that realised volatility is rising, with the Nasdaq 100’s 14dATR now at 1.8%. Readings above 1.9% are consistent with corrective or bear phases (see chart below). If we continue to shake around, then volatility-sensitive players, such as vol control funds, may start to sell.

On the positive side, it’s hard to ignore the Dow Jones making a new high, along with RSP, the equal-weighted SPY.

The Fed

Now the question of Powell’s successor has been settled, it was back to business as usual with a bunch of Fed speakers on deck offering their takes on policy. There continues to be a range of opinion within the FOMC about how far from neutral the FFR stands, and therefore how many cuts to expect in 2026.

Bostic (Mon): no cuts for 2026 pencilled in, policy now 1-2 cuts higher than neutral

Barkin (Tue): policy now at higher end of neutral range, econ encouraging, risks remain on inflation and jobs

Jefferson (Fri): policy roughly neutral

Daly (Fri): leaning towards more cuts in 2026, case could have been made for a cut at last meeting

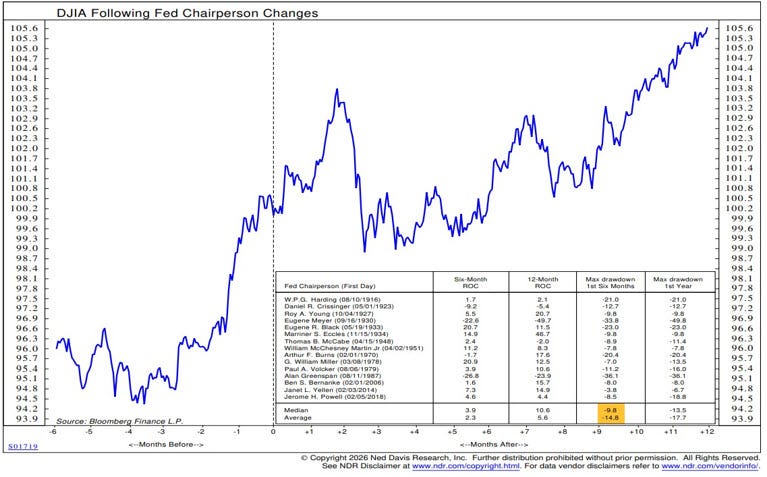

An interesting post caught my attention from the excellent Ed Clissold of Ned Davis Research. He provides some colour on the notion that the market tests new Fed Chairs early in their tenure, full post here. Ed notes, “Markets tend to test new Fed chairs. The average correction in the first six months is 15%. When the chair faces their first crisis, investors don't wait and see how they handle it.”

Markets & Narratives

1/ Iran

No change here from last week. America has gathered a powerful force in the Middle East, the question is will they use it? Niall Ferguson provides some useful colour in this podcast interview. He discusses the idea of regime alteration (Venezuela-style), rather than regime elimination.

2/ Cross-asset volatility

It doesn’t feel an exaggeration to say pockets of the market have suffered crashes in recent weeks. SLV dropped -40%, IGV -30%, and IBIT -50%. For an interesting discussion of these moves, see The Short Bear’s take below. If these moves have now played out, a headwind for QQQ may be diminishing.

3/ AI, software, and creative destruction…

As noted above, the software ETF IGV has dropped -30% from its high. The fundamental narrative behind its fall is that new AI tools, such as Anthropic’s Claude, allow software buyers to create their own applications. That in turn kills demand for the traditional software products of firms like NOW, CRM, and MSFT, whose charts have been in freefall.

Consider the example posted this week by the excellent Florian Kronawitter (link here, “The Digital Gutenberg Moment”). With zero coding background and in little more than a month, Florian claims to have built an investment application that has largely replaced his Bloomberg terminal. Through nothing more than a conversation with Claude (FK, “it is literally a conversation”), he has built a custom platform to support his investment process. It’s well worth reading about his experience, which is equal parts inspiring and terrifying.

Among the implications Florian notes, perhaps the most significant is this, “it has now likely never been easier to attack an existing business”. Up till now, the AI theme has focused on the picks-and-shovels winners of the AI infrastructure buildout. However, the theme is now ferreting out the losers. It brings to mind Warren Buffett’s observation about investing during times of rapid technological change, that it can be easier to identify losers than winners. When the automobile arrived in the early 20th century, there were hundreds of auto companies, so picking the winner was almost impossible. However, picking the loser, horses, was quite obvious. “What you really should have done in 1905 or so, when you saw what was going to happen with the auto is you should have gone short horses. There were 20 million horses in 1900 and there’s about 4 million now.” Will more subsectors and tickers suffer IGV-style drops as investors suddenly lose confidence in business models existentially threatened by AI?

Breadth

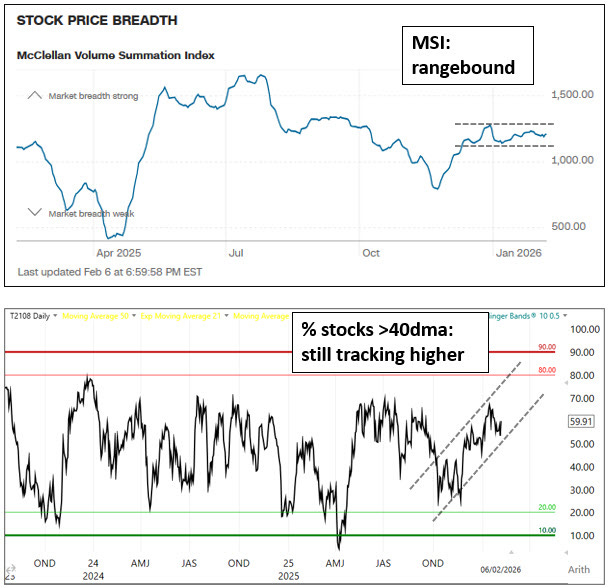

Despite the drop in QQQ, breadth held up OK this week. The McClellan Summation Index is tracking sideways, while the % of stocks above their 40dma is still more-or-less on the up.

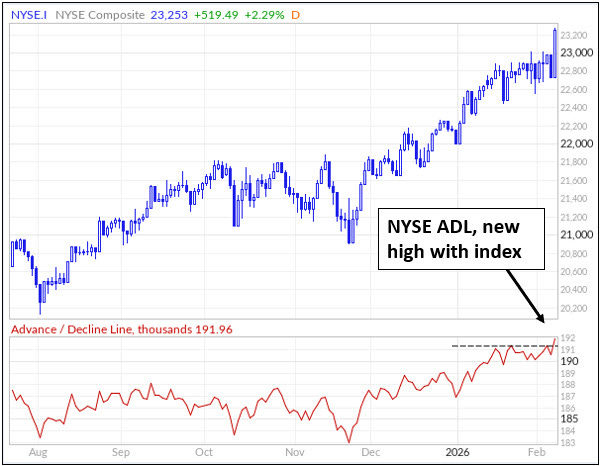

Elsewhere, the NYSE Composite advance decline line made a new high, which is constructive.

Sentiment & Positioning

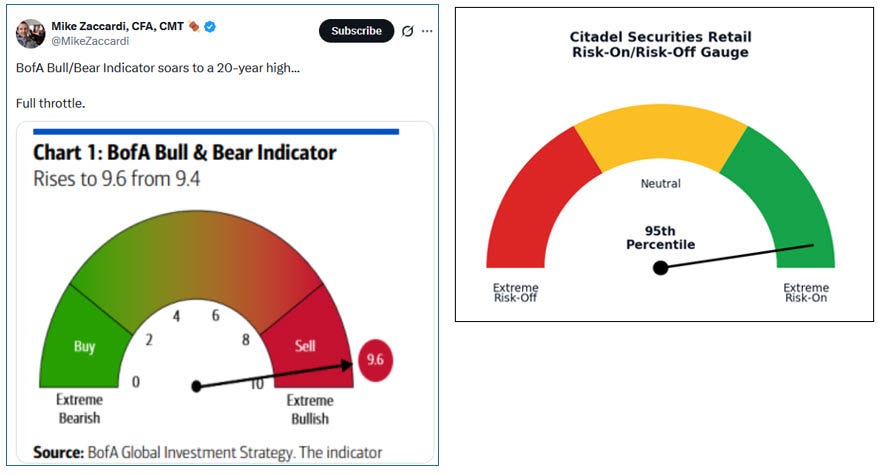

We have a bunch of mixed signals here, which isn’t terribly helpful. Bank of America’s Bull & Bear Indicator and Citadel’s Risk-On/Risk-Off Gauge are red flags.

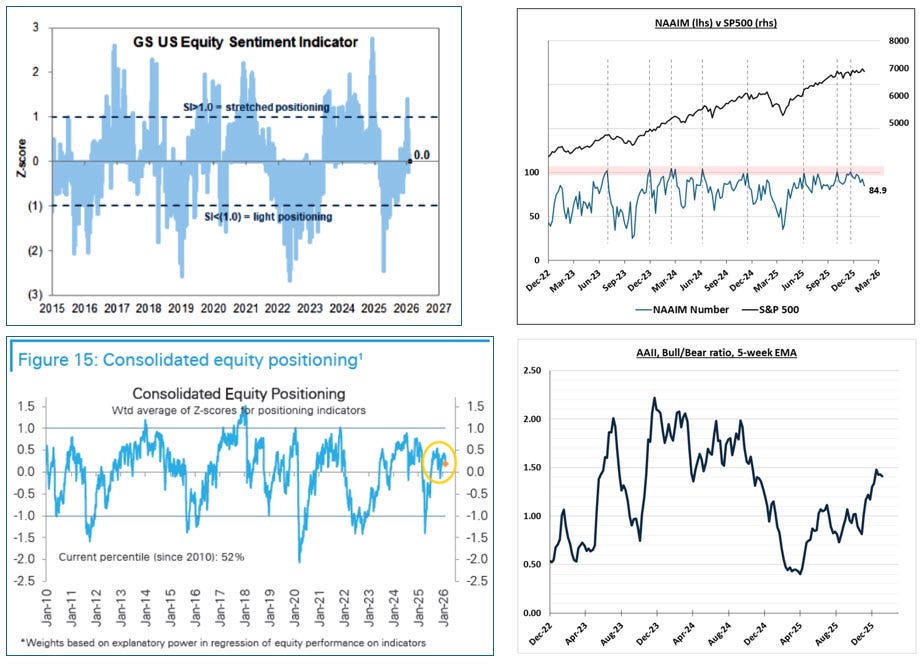

However, many other indicators are in neutral territory, including Goldman’s, Deutsche Bank’s, the NAAIM, and AAII.

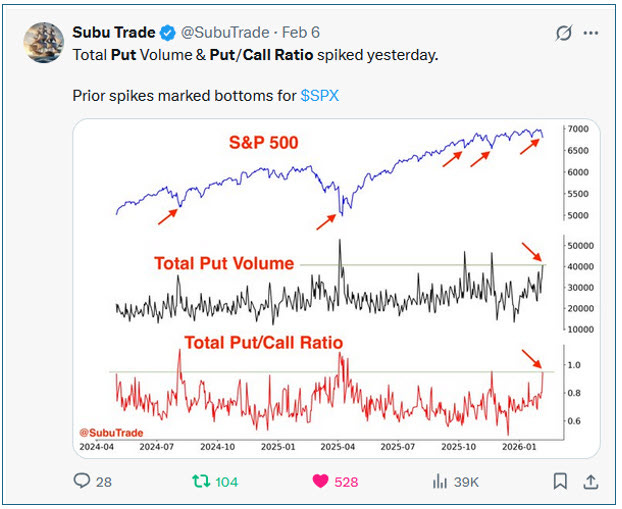

Meanwhile, the options market is more characteristic of a short-term low than a short-term top.

Seasonality

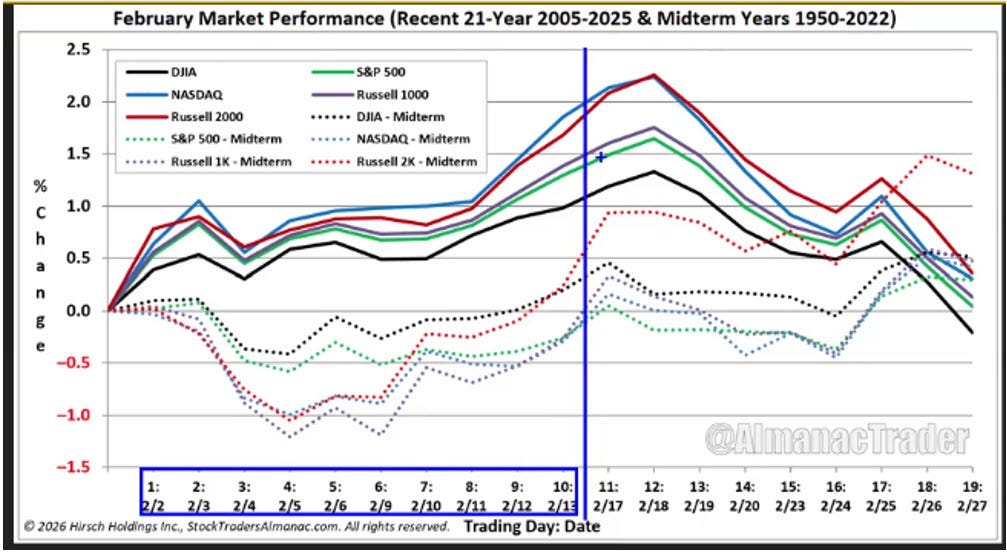

Note the seasonal fade mid-February, although this is less pronounced in mid-term years.

Summary

Price action: QQQ fell to support at 600, at the bottom of a multi-month range. Realised volatility is approaching levels characteristic of a corrective or bearish phase. The longer-term primary trend of QQQ remains bullish. DIA and RSP made new all time highs.

The Fed: the market has a tendency to “test” new Fed Chairs.

Markets & Narratives: 1/ Iran remains an unpredictable factor. 2/ Has recent cross-asset volatility played itself out? 3/ The AI theme is ferreting out losers.

Breadth: ok

Sentiment & Positioning: Mixed messages. Red flags from BoA and Citadel. Neutral readings from GS, DB, NAAIM, and AAII. Put call ratio is characteristic of a short-term low.

Seasonality: February is mixed.

Key events next week: Iran headlines, NFPs, CPI.

View

Short-term: no strong view short-term. Waiting for a break of the 4-month range. Long term bullish factors (policy, econ, earnings) argue for an upside break in QQQ. New all time highs in DIA and RSP are also bullish. However, there is scope for a downside break on disruptive Middle East headlines or a new negative narrative, possibly relating to AI disruption. Feeling somewhat wary about defensive outperformance (XLP), cross-asset volatility, mixed February seasonality, and the emergence of red flag readings in certain sentiment indicators.

Long-term: the primary trend is bullish.

Technical evidence

QQQ is trending higher above its upward-sloping 200dma. It has reclaimed the bullish primary channel in play from the 2022 lows.

Fundamental evidence

Monetary stimulus as the Fed cuts its policy rate.

Fiscal stimulus from Trump’s spending bill.

US economy is strengthening, supporting earnings.

Challenges and risks:

Fed independence: is Warsh his own man?

Geopolitical uncertainty surrounding Iran.

Uncertainty relating to the AI theme: OpenAI’s ability to honour $1.4t spending commitments, NVDA’s monopoly, capex depreciation, hyperscaler credit spreads, skepticism relating to scaling assumptions, disruption to incumbent business models such as software.