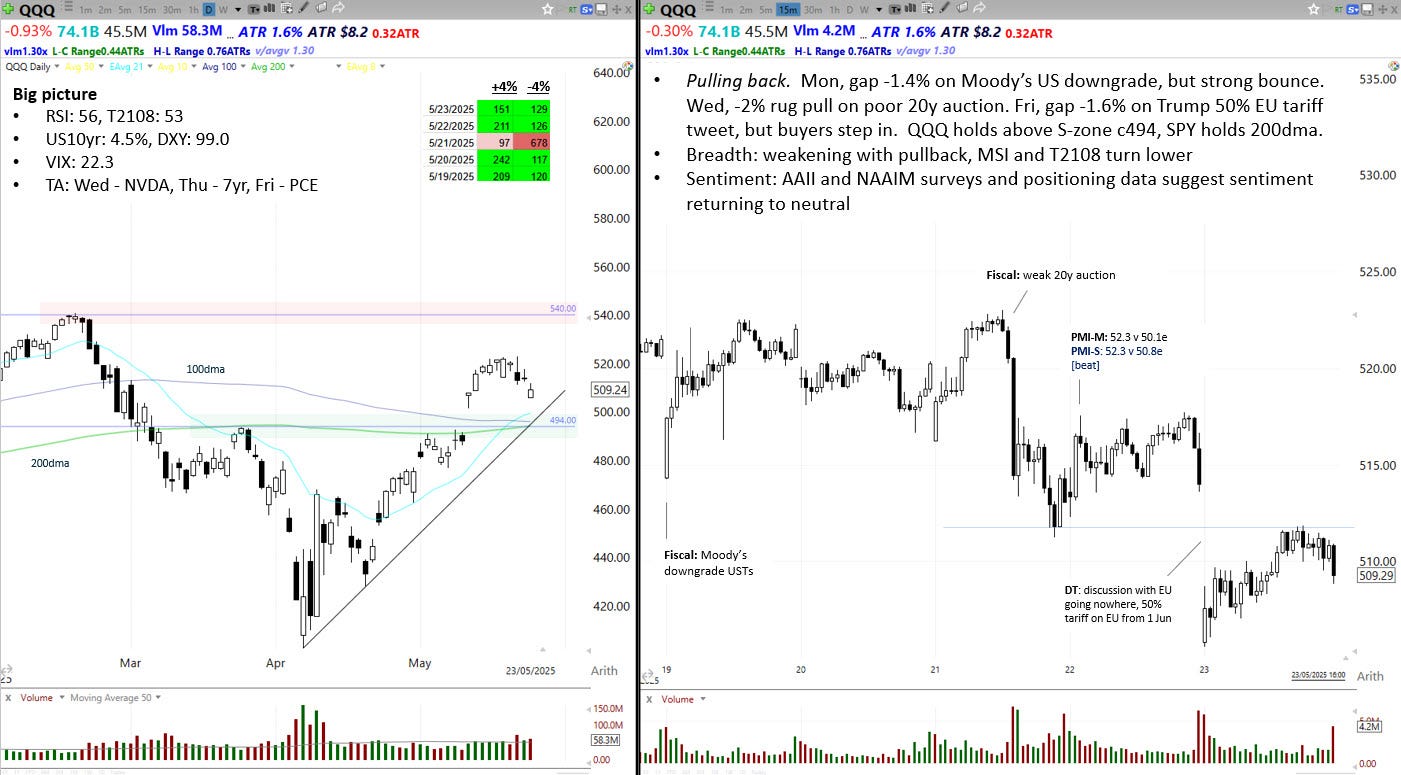

Price action

QQQ eased back from short-term overbought conditions, finishing the week -2.6% from Wednesday’s high. The week turned on Wednesday’s 20-year bond auction, which saw weak demand for America’s long-term bonds. Yields spiked, and QQQ dropped -2.2%. Although yields eased back as the week progressed, on Friday QQQ took a second step lower after President Trump tweeted that he intended to impose a 50% tariff on European imports on 1 June.

These negative catalysts provided QQQ and SPY an excuse to take a breather from their steepling rallies up from the April lows. On Sunday, news broke that Trump had spoken to European Commission president Ursula von der Leyen and agreed to delay the 50% tariff till 9 July, which provides a new positive catalyst for QQQ.

As we noted last week, realised volatility is falling. The 14d ATR is now at 1.6%, which is consistent with bull market conditions. Meanwhile, the short-term overbought condition we noted in QQQ has now cooled off. Having reached +2.7 ATRs above its 10dma, QQQ is now -0.8 below it. And having reached +4.6 ATRs above its 20dma, QQQ is now only +1.3 ATRs above it.

The Fed

There were plenty of FOMC speakers on deck this week. The message continues to be that the Fed remains in wait-and-see mode, and that if tariffs cause rising inflation and weakening jobs, they will prioritise their price stability mandate.

Williams (Mon): recent data very good, jobs in balance, Q1 GDP unusual due to trade, econ in good place, policy slightly restrictive, Fed can take its time, path might not be clear for months

Bostic (Mon): Moody’s downgrade could have implications for cost of capital, could ripple through the econ, leaning towards one cut this year, depends on trade policy, more risk on inflation than employment, inflation expectations moving in a troubling way, inventory rundown may be nearing an end

Musalem (Tue): monetary policy well positioned, if inflation expectations become de-anchored Fed policy should prioritise price stability, policy uncertainty high, tariffs just as likely to have one time as persistent effect on prices, hearing that businesses and households holding back from decisions amid uncertainty, impact of uncertainty tends to be pretty meaningful

Hammack (Tue): most likely scenario from tariffs is a stagflationary outcome.

Hammack (Wed): best for Fed to sit on hands for now.

Waller (Thu): bond market wants more fiscal discipline, Fed in wait-and-see mode, firms are pausing not cancelling plans, tariffs will bring one time price increase which a central bank should look through

Goolsbee (Fri): need to wait for dust to clear.

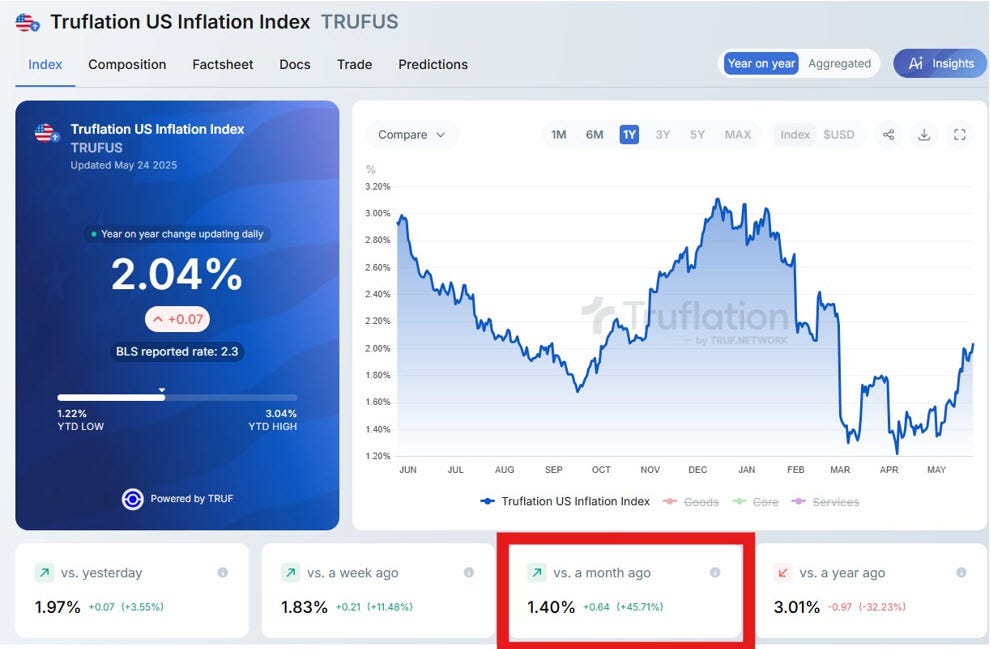

Are we seeing any initial signs that the tariffs imposed so far are impacting prices? Jim Bianco points to Truflation data as potential evidence this may be starting to happen. The Fed are watching this closely, as is the bond market…

Markets and narratives

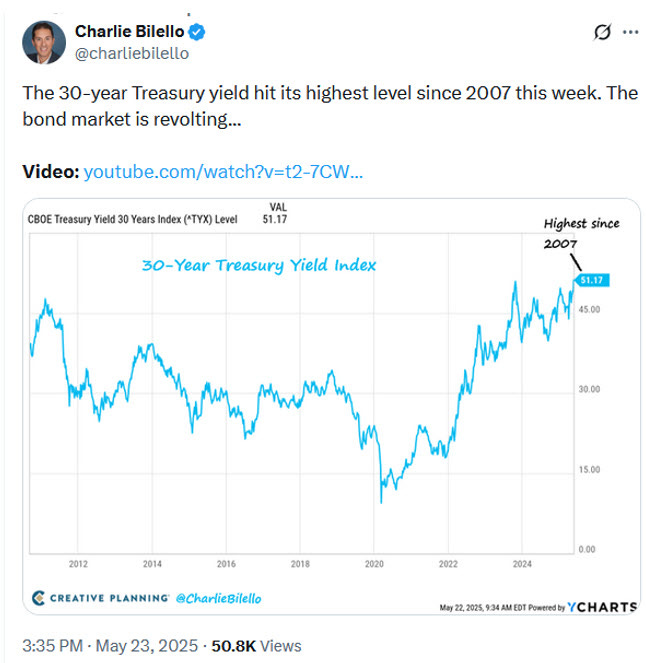

As we noted last week, a new bearish narrative is potentially emerging, which relates to US debt sustainability. On Friday 16 May, Moody’s downgraded America’s credit rating, which caused a gap down on Monday morning. QQQ quickly shook that one off, bouncing on Monday morning to fill the opening gap. However, there was more bad news from the bond market as the week unfolded. Wednesday’s 20-year bond auction was weak, causing a -2.2% drop in QQQ. The long end of the US yield curve is experiencing upward pressure.

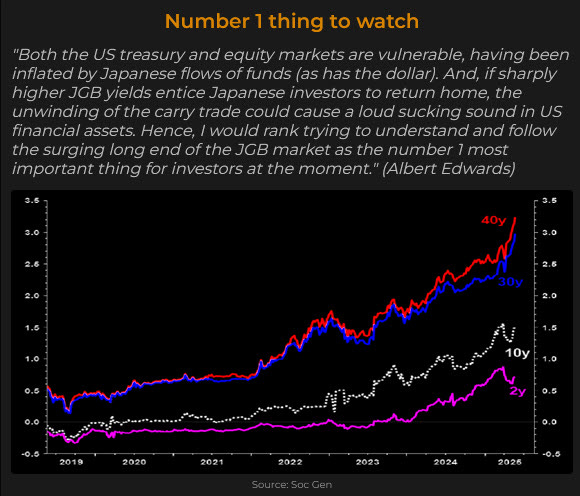

Elsewhere in global fixed income markets, long-term Japanese Government Bonds have been selling off. These dynamics brings to mind the events of August 2024.

If higher yields fail to attract demand from real money buyers such as pension funds, insurance companies, and asset managers, then we should expect a growing headwind for QQQ.

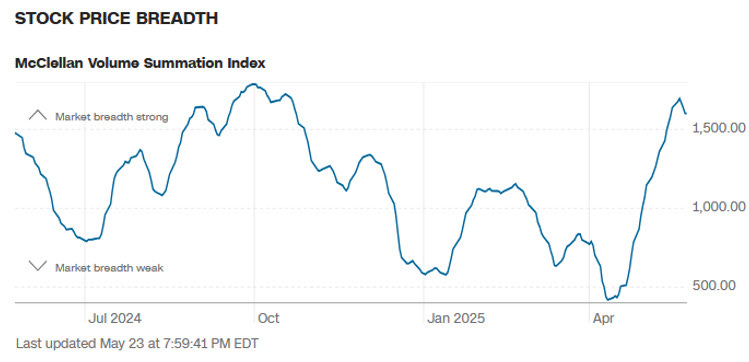

Breadth

Having been very strong for a number of weeks, breadth eased off this week. The McClellan Summation Index turned lower.

As did the % stocks above their 40dma.

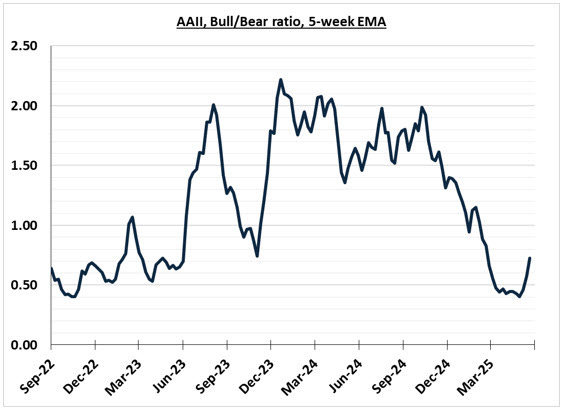

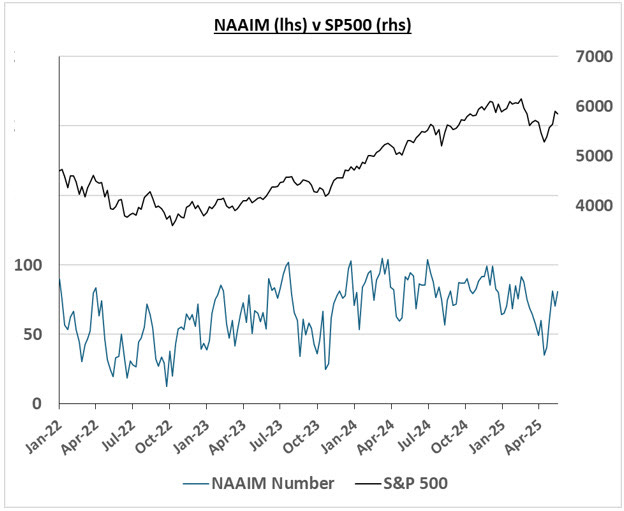

Sentiment

The surveys suggest sentiment is returning to a more neutral position. The 5-week MA of the AAII bull/bear ratio continues to lift from recent ultra-bearish lows.

The NAAIM is now back at 81, a moderately bullish reading.

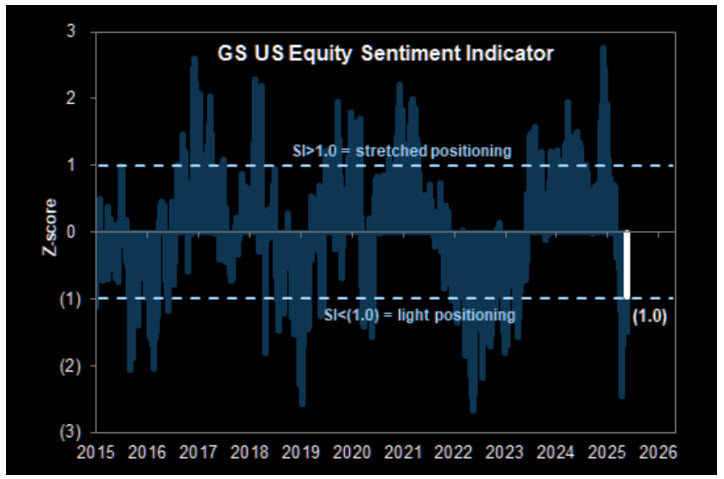

The GS US Equity Sentiment Indicator shows light positioning among institutions.

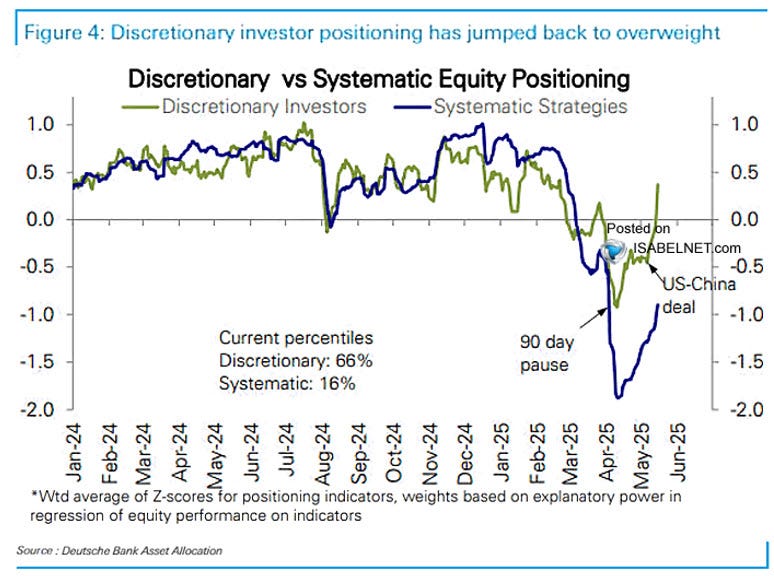

Meanwhile among hedge funds, discretionary managers are back to a modest net long position, though systematic managers are still net short.

Seasonality

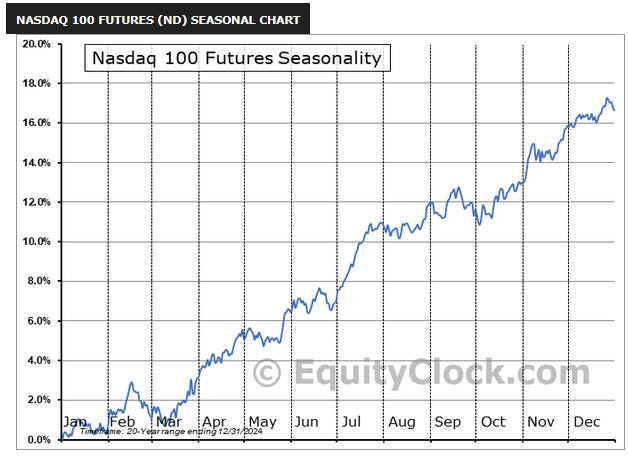

A seasonal tailwind picks up at the back end of May.

Summary

Price action: having reached a short-term overbought condition, QQQ pulled back after a weak 20-year bond auction and a threat by President Trump to impose a 50% tariff on imports from the EU. On Sunday, this threat was postponed. Realised volatility is consistent with bull market conditions. QQQ and SPY are holding above key support at their 200dma’s.

The Fed: the Fed remains in wait-and-see mode due to uncertainty about the impact of tariffs on inflation and jobs. Some indications may be emerging of upward pressure on prices.

Markets & Narratives: rising long-term bond yields and a challenging narrative surrounding US debt sustainability may develop as a headwind for QQQ.

Breadth: after a phase of very strong breadth since April’s low, breadth eased back this week.

Sentiment: surveys of sentiment and positioning suggest sentiment remains light, but returning to a more neutral condition.

Seasonality: Nasdaq 100 seasonality improves towards the end of May.

Key events next week: US trade negotiations with EU and Jap; Wednesday - NVDA earnings; Thursday - 7yr bond auction; Friday - Core PCE.

View

Long-term: Neutral, but edging towards bullish again. Constructive evidence has emerged in the last month: (1) QQQ has reclaimed its 200dma and bullish trend channel. (2) Realised volatility is consistent with bull market conditions. (3) the Trump admin has walked back hardline trade policy with China and Europe and shows no appetite for fiscal austerity. (4) Recent economic data has shown the economy is holding up ok. (5) Breadth has been very bullish, evidenced by a sequence of thrust signals with good statistical records. (6) Investors still have some work to do to rebuild equity exposures. However, fiscal sustainability is emerging as a new challenging theme, and trade uncertainty still has room to run.

Short-term: Neutral. A pullback to the support zone between 494-500 could offer an attractive long entry.