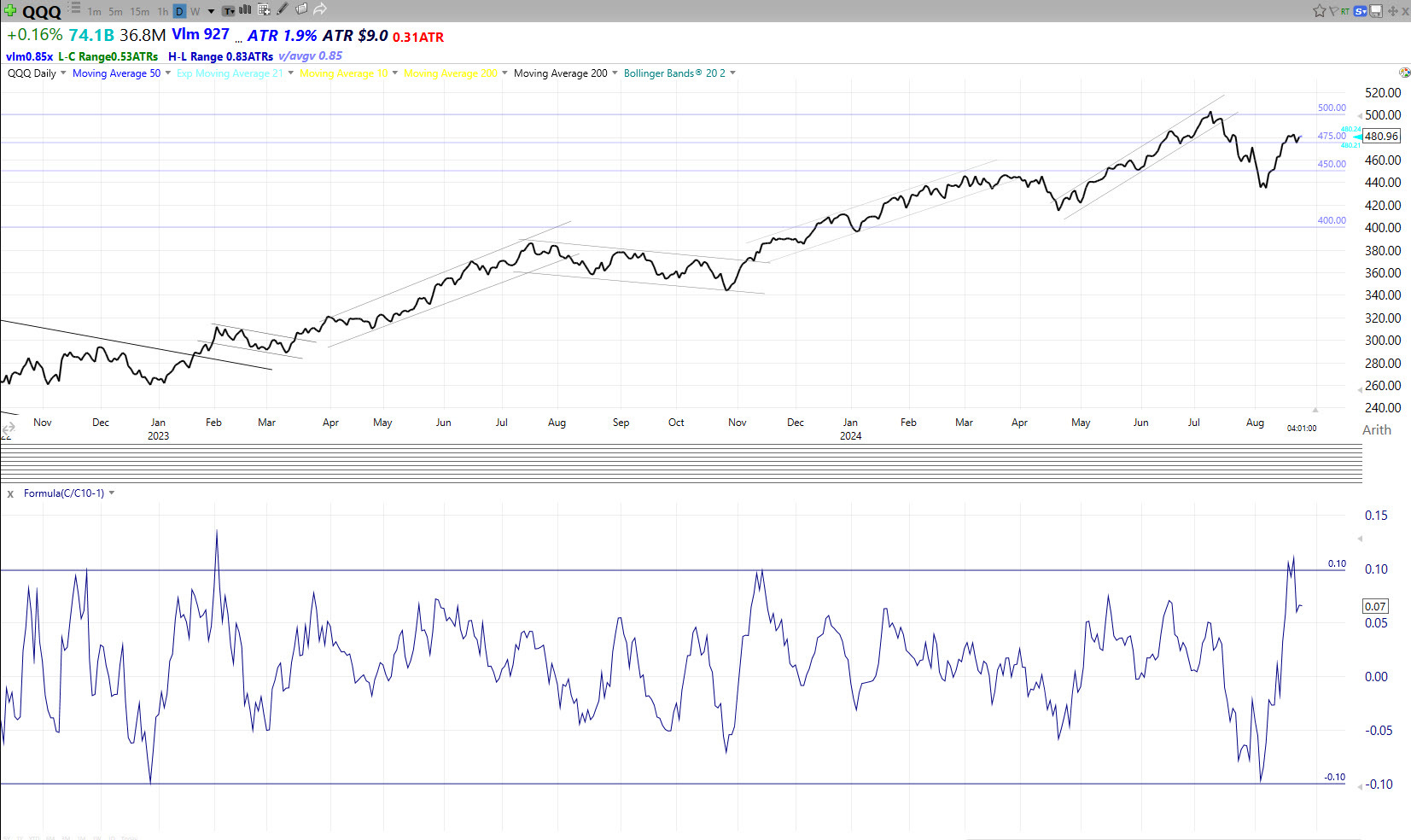

QQQ weekly: 19-23 Aug

Price action

After a fast bounce from the 5 August low, QQQ paused above its 50dma. In the 11 sessions from 5 August QQQ lifted +14%, which is an awful lot of ground to cover in a short period of time (as is shown by QQQ’s rate of change chart below). As we noted last week, a period of consolidation might be needed to digest the bounce - this may come in the form of mid-range summer chop. Intraday price action from Tuesday to Friday was full of spikes and reversals and signifies a lack of participation from market makers and momentum traders as we head into late August/early September.

The Fed

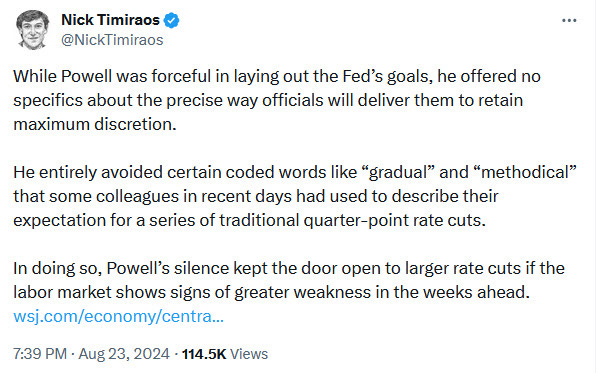

This week the Federal Reserve Bank of Kansas City hosted its annual symposium at Jackson Hole. JPowell delivered his speech on Friday. For all intents and purposes he announced that the Fed will begin a cycle of interest rate cuts at the FOMC meeting on 18 September.

JPowell (Fri):

the time has come for policy to adjust

labour market cooling is unmistakable, we do not seek or welcome further cooling, will do everything we can to support strong labour market as we make further progress toward price stability

timing and pace of cuts data dependent, policy rate level gives ample room to respond to risks, including unwelcome further weakening in jobs

This was strong wording. JPowell is saying (1) he doesn’t want to see any further labour market softness, and (2) if he does see it, the Fed “will do everything we can do” to arrest it. If the next NFP report (due Fri 6 Sep) is weak, then we should expect a substantial response.

On which point, Nick Timiraos of the WSJ noted the absence of language about the cutting cycle being a “gradual” process.

What did we learn about markets?

DXY and the US10y yield have both weakened as the market prices in the cutting cycle. Falling rates and a falling dollar are usually supportive for equities. However, if that weakness occurs in the context of a deflationary/recessionary impulse, then this is problematic for stocks. Watch DXY for a break below 100 and the US10yr yield for a break below 3.5%, especially if that occurs on disappointing labour data.

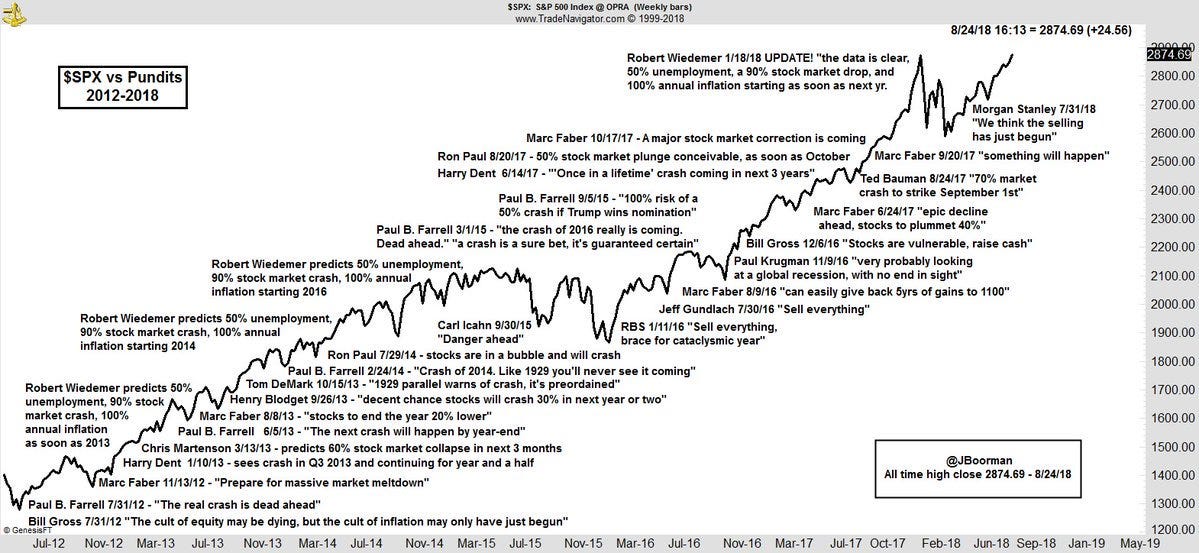

While we are on watch for a deterioration in economic data, remember that predicting a US recession is not easy. Recessions remain thankfully rare and recent ones required very large catalysts to produce them. For example, the collapse of the US housing market and the failure of multiple major financial institutions in 2007-8, or the sudden and complete global economic shutdown caused by the pandemic in 2020. Meanwhile, the financial media will tend to produce a constant stream of negative takes to capture our attention and in so doing boost their advertising revenue. The chart below from the late Jon Boorman shows that crashbait media is a permanent feature of the market. Lesson: follow the data and the charts, not the headlines.

Breadth

The Market Monitor showed 762 stocks +4% on Friday after JPowell’s Jackson Hole speech. We saw strong moves in interest-sensitive ETFs: IWM (+3.4% on Friday), KRE (+5%), XHB (+5%). We also saw strong moves in story stocks and speculative areas like ARKK (+5%) and IBIT (+7%).

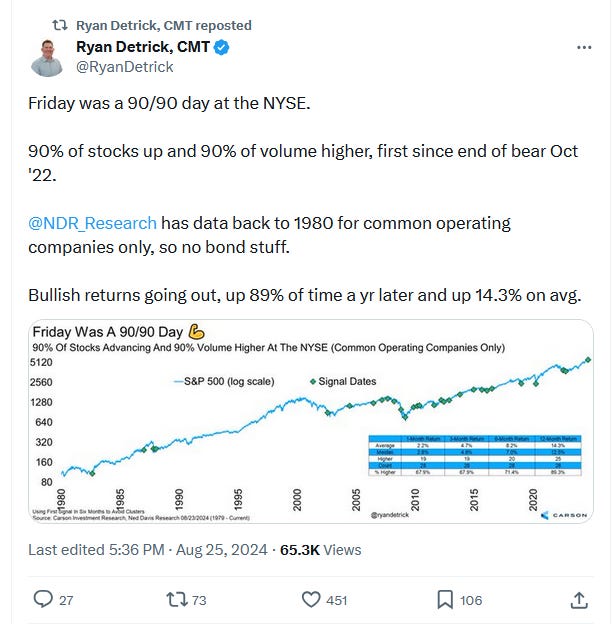

The excellent Ryan Detrick notes that on Friday 90% of NYSE stocks were up on the day, with 90% of the volume higher (source here). Breadth thrusts like these tend to be bullish signals.

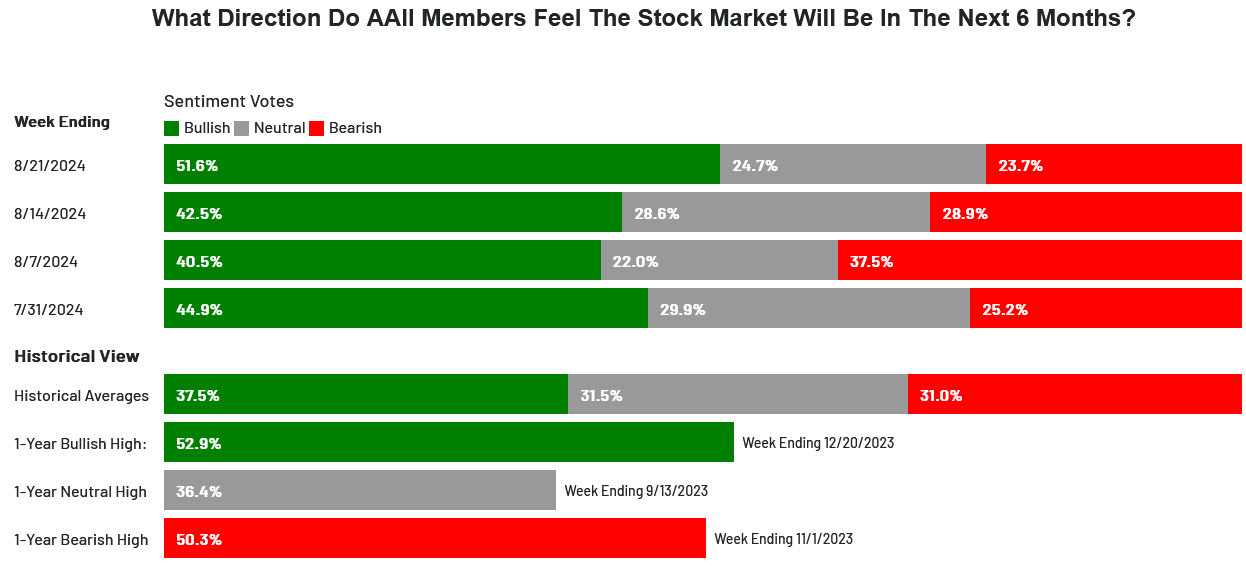

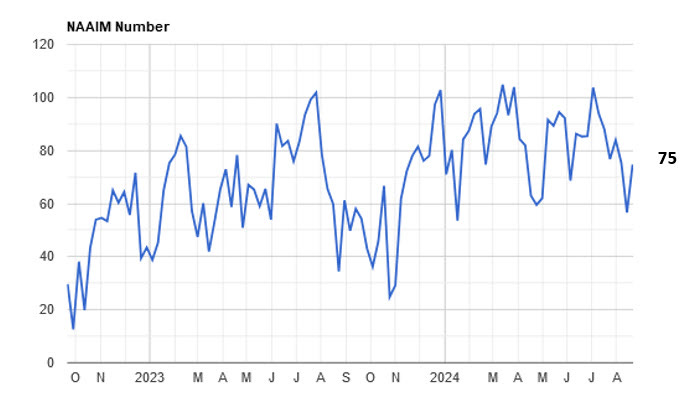

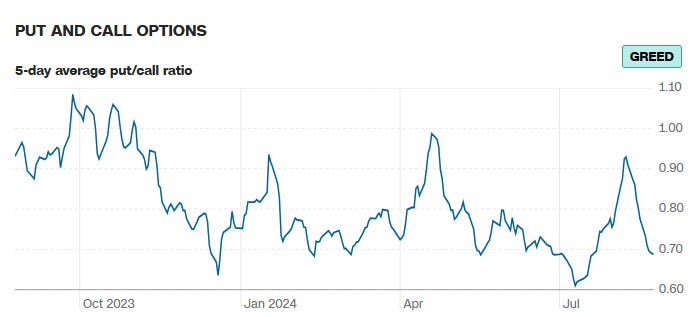

Sentiment

The surveys are showing an abrupt turnaround in sentiment after the pullback. It would be more constructive for further immediate upside if sentiment was still low and still catching up, but moderately strong bullish sentiment tends not to be contrarian bearish.

AAII: Bulls up to 52% (nearly at 1yr Bullish high), Bears down to 24%

NAAIM: a bit slower to turn higher than AAII

Put call ratio: crisis, what crisis?

Seasonality

Your weekly reminder that seasonality is not helpful from late August to early October. The erratic intraday price action this week in QQQ is part of that story.

Summary

Price action: this week QQQ consolidated just above its 50dma after its large, fast bounce from the 5 Aug low. Intraday price action was erratic and difficult. The longer term primary trend remains bullish.

The Fed: at Jackson Hole on Friday, JPowell effectively announced a cutting cycle will begin at the next FOMC meeting on Sep 18.

Breadth: breadth was strong this week with notable outperformance in small caps and interest-rate sensitive sectors on Friday.

Sentiment: surveys and options markets show sentiment has rebounded after the early August washout.

Markets: be careful with recession-related clickbait.

Key events next week: Wednesday - NVDA earnings, Friday - PCE.

PS, an explainer for the weekly slide can be found here:

https://chartnotes.substack.com/about

PPS, if you find these posts useful, please do post and share - thanks!