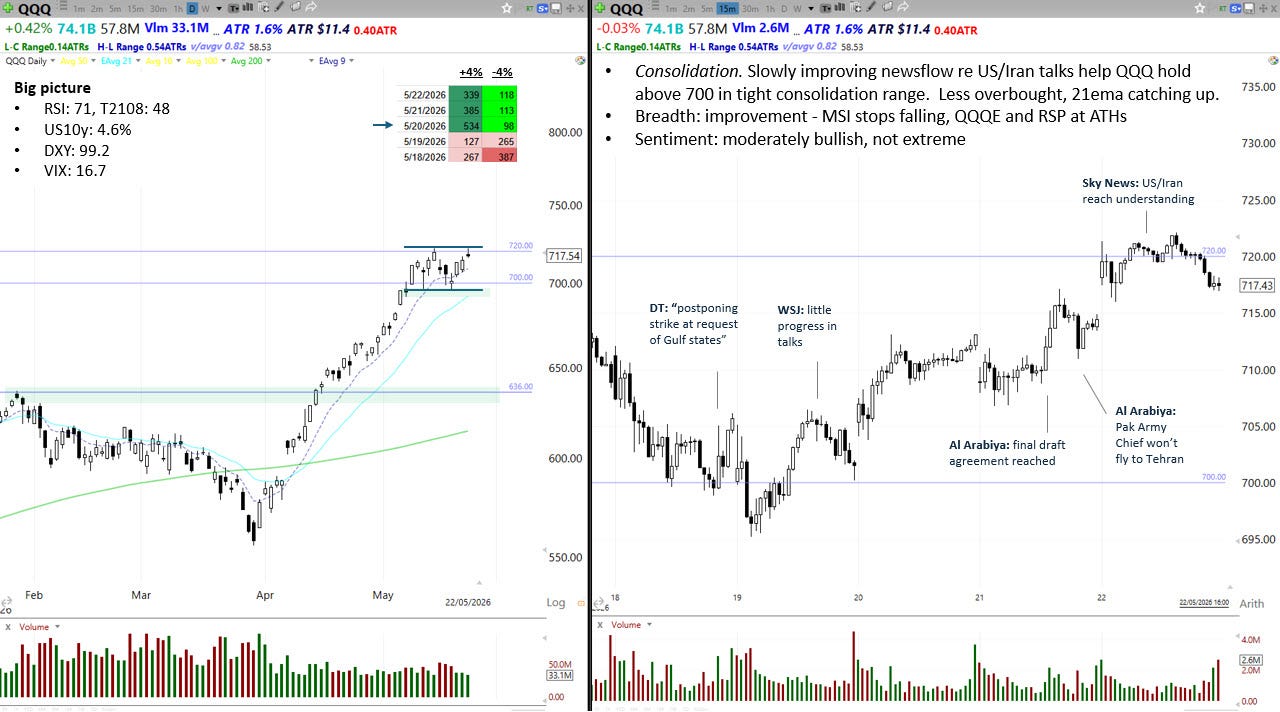

QQQ weekly: 18 - 22 May 2026

Consolidation

Price action

QQQ found support on Tuesday around the 700 round number, and by Friday’s close it had rallied back to the top of a 25-point consolidation range. The move higher was helped along by newsflow around US/Iran talks, and an earnings report from NVDA that was just fine.

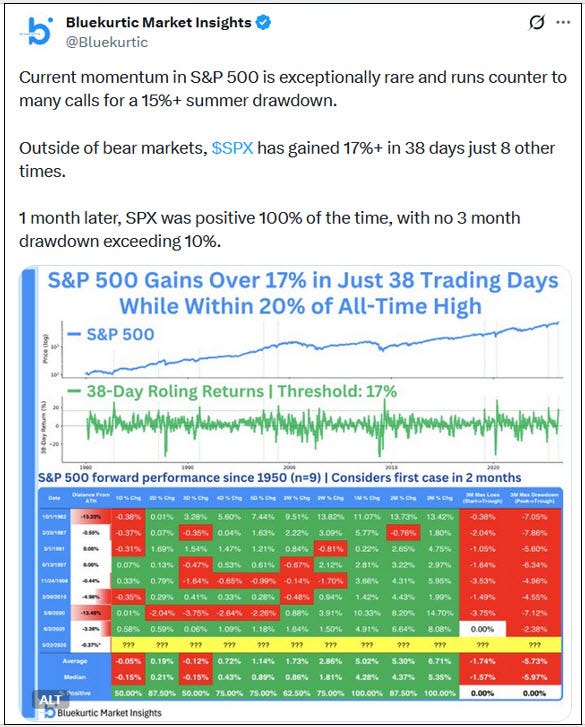

QQQ is working off the very overbought condition it reached two weeks ago when its RSI hit 83 on 8 May. Impressively, it’s done this by moving sideways rather than down, which speaks to current strength. Bluekurtic provide a useful study on historic episodes of extreme positive momentum similar to the one we’re seeing now. They examine phases when the S&P500 gained +17% in 38 sessions (excluding bear market rallies). On the eight occasions when this has happened, the index was higher one month later with an average gain of +5.0%. The idea is that these bursts of price momentum, like bursts of breadth momentum, appear at the start of larger rallies. Precedent suggests momentum begets momentum, and that further upside is entirely plausible.

The Fed

FOMC minutes came out on Wednesday - they confirmed the hawkish tone we’ve heard from FOMC speakers in recent weeks.

FOMC minutes (Wed): a majority of participants said additional policy firming would likely become appropriate should inflation continue to run above the Fed’s 2% target, while many participants said they would have preferred removing the easing bias language from the statement altogether.

The hawkish transition among FOMC members was well-illustrated this week by Fed Governor Christopher Waller. As recently as the January FOMC meeting, Waller was advocating for rate cuts. At that meeting he dissented (along with Miran) in favour of a 25bp cut instead of holding rates unchanged. He has now completely changed his tune…

Waller (Wed): given recent data, it’s crazy to be talking about rate cuts in the near future.

On Friday, Kevin Warsh was sworn in as new Fed Chair, replacing Powell. One of his most pressing jobs is to establish a rapport with the market. His first major test will be the 17 June press conference at the next Fed meeting. The journalists he faces are experienced and clever, and Warsh must avoid a communication misstep when he fields their difficult questions (cf Christine Lagarde and Italian BTPs, March 2020). Markets are pricing in elevated volatility that day.

His also needs to build a working relationship with his FOMC colleagues. The dove Miran has left, Waller and others have turned hawkish, and Powell, despite stepping down as Chair, will remain on the FOMC as an influential governor, which could muddy Warsh’s leadership. And all this is in the context of (1) rising inflation - the Cleveland Fed inflation nowcast is now estimating headline CPI at 4.2%, and (2) President Trump pressuring Warsh to cut rates, either in public or private (Trump is a close friend of Ronald S Lauder, Kevin Warsh’s father-in-law). There is scope for Fed dysfunction while Warsh settles in.

Markets & Narratives

1/ Iran

As we write this, there are signs of an initial understanding between America and Iran. Hopefully the worst has now passed and we see energy prices, inflation, and bond yields easing back, which would be constructive for QQQ. Weekend markets on Hyperliquid and IG show the Nasdaq 100 up around +1.0% currently.

However, this is only an agreement to start further negotiations, not a final deal. The two sides remain far apart on control of the Strait of Hormuz and Iran’s enriched uranium, so there’s room for plenty more back and forth. I remain mindful of Sir Alex Younger’s obervations that Iran strongly wants to avoid a loss of face, which is an obstacle to making the concessions America demands.

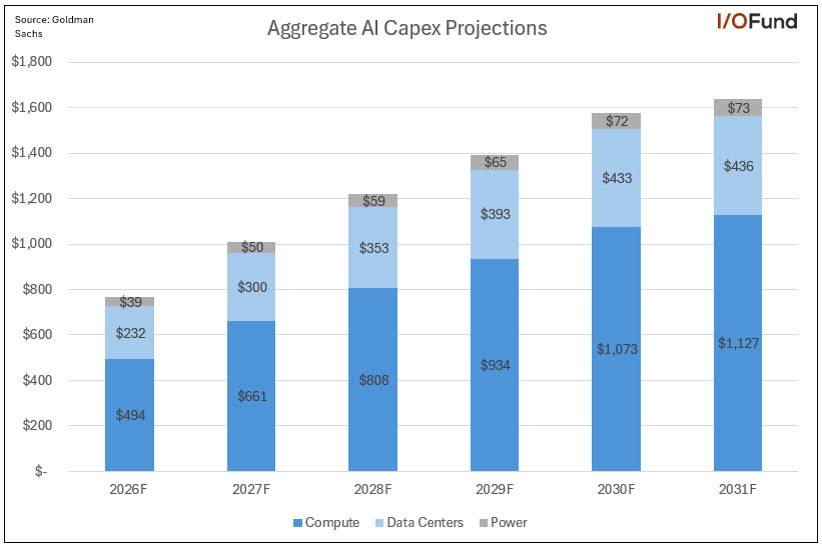

2/ AI Capex

Street forecasts for AI capex show no sign of letting up, running to trillions per year for the foreseeable future (chart below from GS via Beth Kindin). The numbers are bonkers. As long as this trillion-dollar narrative persists, AI-adjacent stocks have a tailwind.

Breadth

This week breadth improved as the market priced in an end to the conflict in Iran. Lagging sectors that have struggled with rising energy prices and higher bond yields started to pick up, such as transports, airlines, and utilities. Hopefully, the ceasefire holds and we see a bullish rotation to beaten down sectors.

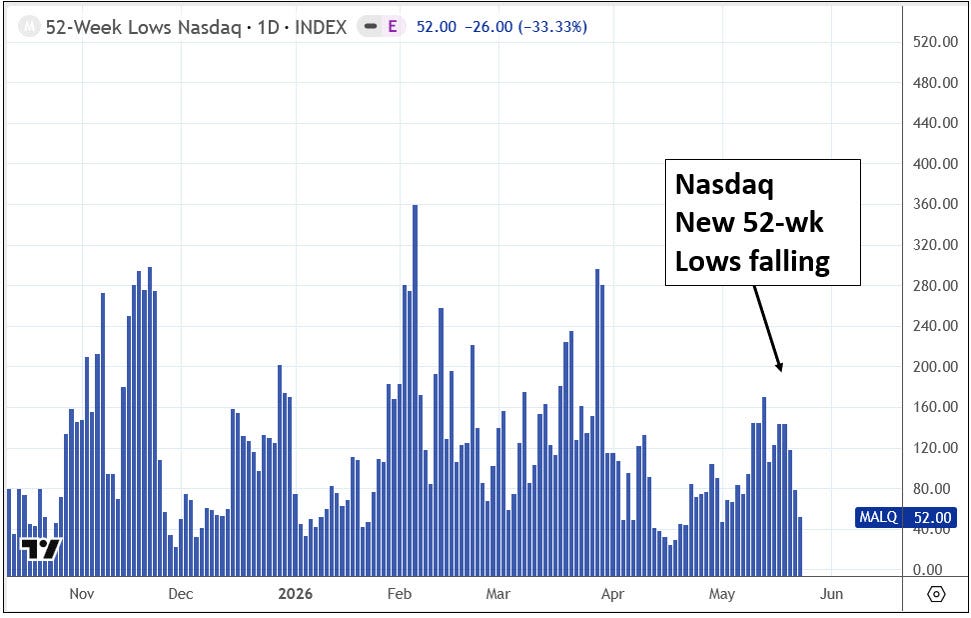

In terms of evidence, the McClellan Summation Index and % stocks above their 40dma both stopped falling. The Nasdaq 100 Advance-Decline Line picked up, while the equal-weighted indices QQQE and RSP both hit all time highs. And most encouragingly, Nasdaq New 52-wk Lows fell quite sharply (see below). This helps alleviate the bearish breadth divergence building since mid-April.

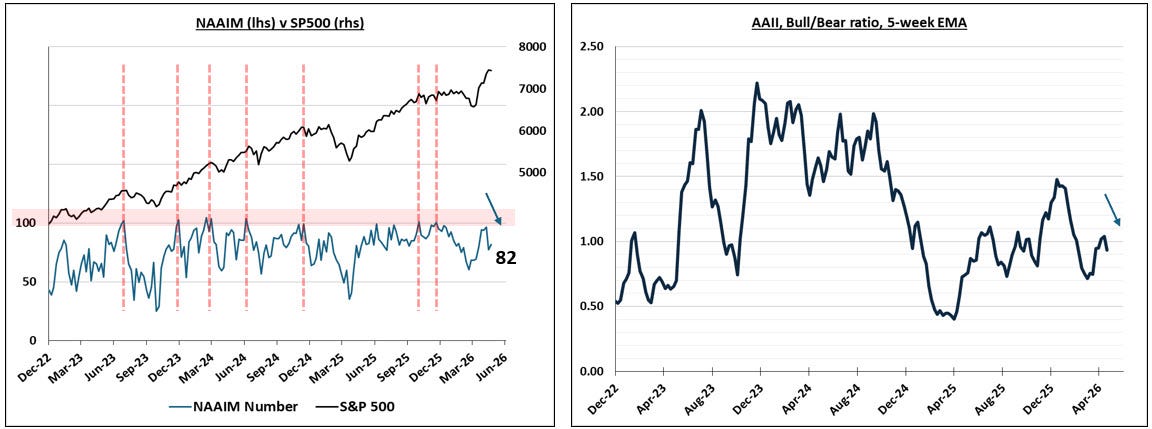

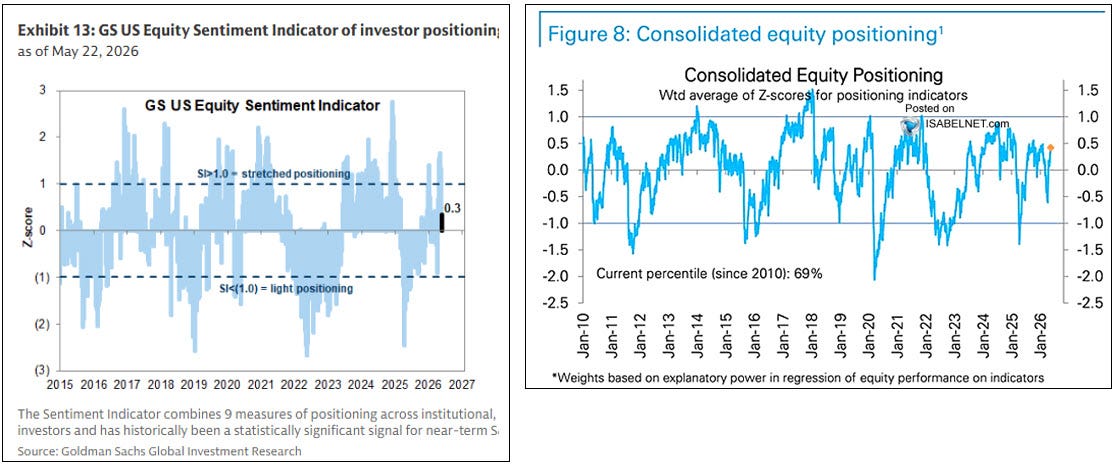

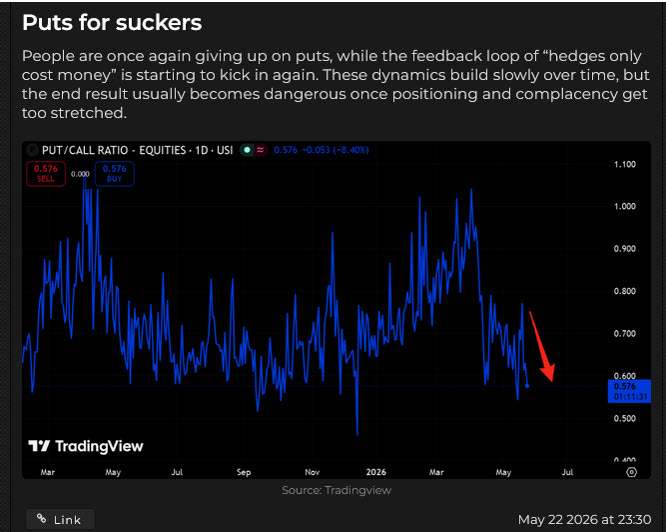

Sentiment & Positioning

Despite extremely strong index momentum, sentiment and positioning are, on the whole, not near euphoria territory. That suggests investors are underweight and that the pain trade could be higher.

NAAIM and AAII: neither are extended.

Investment bank surveys: both GS and DB equity positioning indicators are in neutral territory.

However, there are signs of exuberance in the options market, where Put/Call Ratios have declined rapidly. Hat tip to themarketear.com for this:

Seasonality

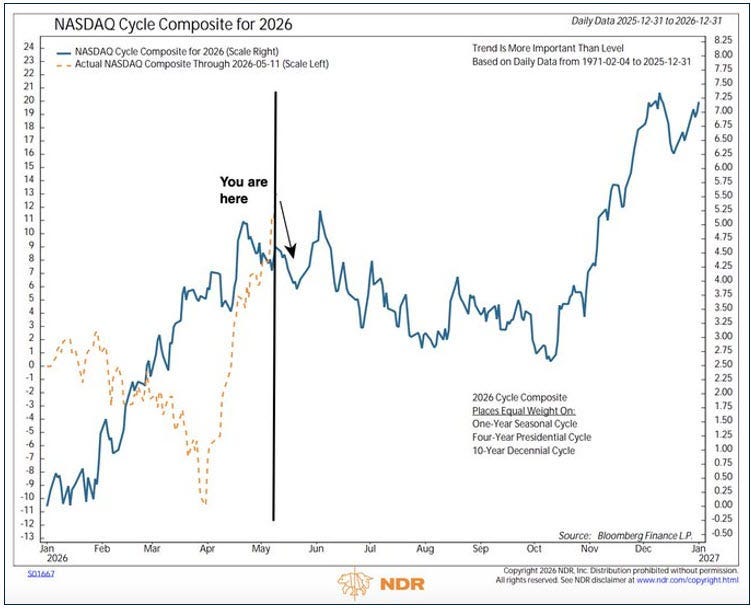

Same observation as our last post. The Nasdaq 100’s 1-year cycle becomes more constructive in the last week of May. However, NDR’s Nasdaq Cycle Composite for 2026 is less constructive (see chart below). This is a composite seasonality study that incorporates the 1-year seasonal cycle, plus the 4-year Presidential Cycle, and the 10-year Decennial Cycle. It suggests we are entering a seasonally challenging phase until the mid-terms.

However, as always, remember seasonality studies work as a guide to inform a probabilistic framework, they are not a bible. A resolution to the Iran conflict, falling bond yields, and ever-increasing AI capex can easily run over seasonally weak tendency.

Summary

Price action: QQQ appears to be consolidating in a tight, 25-pt range as it works off an overbought condition. Certain momentum studies suggest further gains are plausible. The primary trend is bullish.

The Fed: FOMC minutes were hawkish, so was recent-dove Christopher Waller, who stated it would be “crazy” to consider cuts given current data. The Cleveland inflation nowcast estimates headline CPI at 4.2%. Kevin Warsh has taken over as Fed Chair and must build a rapport with the market and his FOMC colleagues, neither of which are straightforward in current circumstances.

Markets & Narratives: 1/ Iran conflict - positive news this weekend. 2/ AI capex forecasts are running at more than $1tr per annum for years.

Breadth: solid improvements, MSI, T2108, and NDQ ADL rising. NDQ New Lows falling. Iran resolution may open door to bullish rotation to laggard sectors.

Sentiment & Positioning: indicators not stretched, but options markets show signs of froth.

Seasonality: the Nasdaq 100 1-year seasonal cycle shows strength at end of May, but seasonality composites that include the US Presidential Cycle suggest mid-term weakness in Q2 and Q3.

Key events next week: Iran news

View

Short-term: orderly consolidation, base case further upside

In early May, as QQQ became very overbought, my base case was for a period of consolidation or pullback after an extreme momentum surge. We have now seen two weeks of tight consolidation in a 25-pt range above 700. My base case is for further upside on the basis of strong momentum, positive news relating to Iran and AI capex, improving breadth, and unchallenging sentiment/positioning. However, I remain mindful that we could see a decent pullback if news relating to Iran disappoints, especially as seasonality is less supportive in the summer of mid-term years. Iran news, inflation, the Fed, and bond yields remain potential challenges.

Conditions for swing trading have been excellent, with breakouts and pullback setups working well, particularly in AI-adjacent stocks - examples this week were ARM, DELL, SNDK, and QCOM. I plan to continue taking these setups as long as they keep working. If the Iran ceasefire holds, I will broaden my focus to include swing set ups in beaten down sectors if they start acting well - airlines, cruiselines, travel, utilities.

Long-term: cautious bullish

From a technical perspective, after March’s pullback QQQ did what it needed to do - it reclaimed its long-term primary bullish trend and its long-term moving averages. The bull market is very much intact.

From a fundamental perspective, there are plenty of tailwinds supporting the market. Fiscal support continues, with the US running a large deficit that stimulates the economy; corporate earnings have been stellar; the AI theme continues to suggest trillions of annual capex spending; and, negative headwinds from Iran, private credit, and AI disruption have eased off.

My long-term view is bullish, but I can’t help but retain a little caution until the Strait of Hormuz is open, bringing energy, inflation, and bond yields down, and lifting pressure on the Fed to hike later this year.

Challenges and risks

Iran conflict and energy shock - rising inflation and bond yields, pushing the Fed to a hawkish pivot.

Fed dysfunction under new Chair Warsh.

Weak mid-term seasonality.

p.s. last week I was guest author of the CMT Association’s Market Mosaic. You can find Friday’s post in the link below - I wrote a mini-deep dive on what to look for in price action, breadth, and sentiment when markets are setting up for a bounce. Hope you find it helpful.

https://content.cmtassociation.org/a/how-to-spot-when-conditions-are-right-for-a-bounce.

See you next week,

Alex