QQQ weekly: 13 - 17 Oct

Choppy range

Price action

On Fri 10 Oct, Trump posted plans for a 100% tariff on China in response to Chinese export restrictions on rare earths, which sent QQQ down -3% that day. On Sun 12 Oct, Trump walked it back, posting that everything with China “will be fine”. As a result, QQQ bounced on Mon 13 Oct. For the rest of the week, QQQ chopped around in a wide 20-pt range, moving up and down on headlines relating to Fed speakers, China trade, and loan defaults at regional banks.

The lack of downside follow-through from the sharp, high volume down day on 10 Oct is constructive. The wide and loose price action this week suggests QQQ needs to settle down before it can move higher. On Friday, the VIX dropped -9pts, which suggests calm is returning. However, we can expect more trade-related potholes until America and China sign a final trade agreement.

The Fed

As we’ve noted in recent weeks, the FOMC is divided between the doves who favour a rapid reduction in the FFR in response to labour market weakness, and the hawks who favour caution as long as inflation is sticky. On Tuesday, Jerome Powell indicated he’s in the dovish camp, so we should expect another cut at the next FOMC meeting on 29 Oct. He also stated that the Fed is coming to the end of the QT process, which is also supportive for stocks.

Powell (Tue): downside risks to jobs have risen, but tariffs pushing up price pressures, Fed approaching end of balance sheet contraction in coming months, data since July shows labour market has softened considerably.

Markets & Narratives

On Thursday, the KRE regional bank index dropped -6% after WAL and ZION disclosed charge-offs on bad loans amounting to a combined $160m. For an excellent discussion of these events and some expert comment on credit markets, check out Steve Eisman’s podcast episode from Friday. He’s the GOAT on such matters. Key takeaway - nothing to worry about yet, but keep an eye on high yield credit spreads and bank earnings.

Breadth

Breadth continues to be weak. The McClellan Summation Index and the % of stocks above their 40dma are both falling.

Sentiment & Positioning

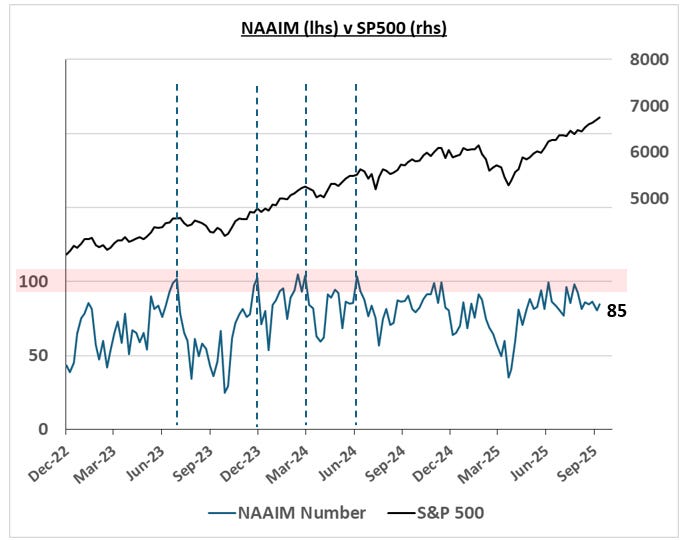

The surveys continue to show neutral positioning. The NAAIM is holding around 80, well below the danger zone above 100:

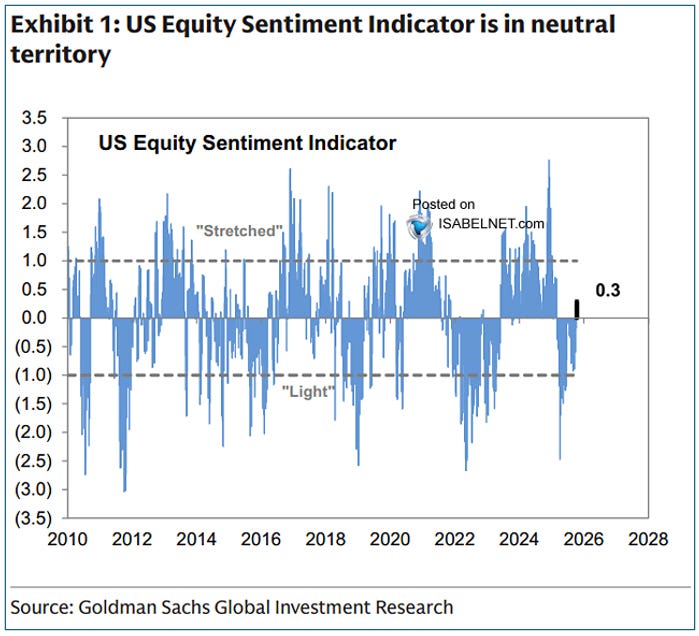

The GS US Equity Sentiment Indicator remains neutral:

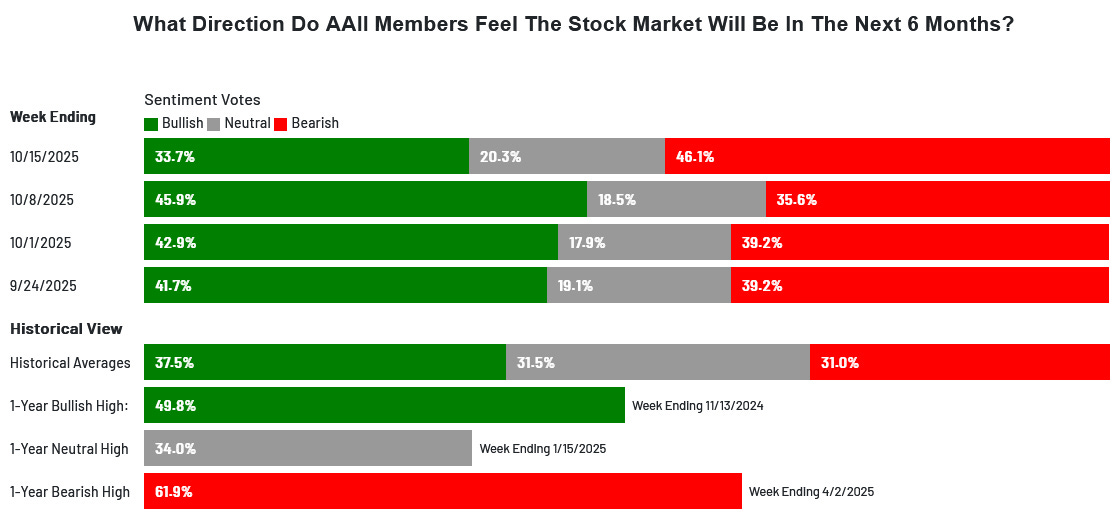

The AAII survey shows more bears than bulls:

As for the options market, the collapse of the VIX on Friday suggests panicky sentiment calming down.

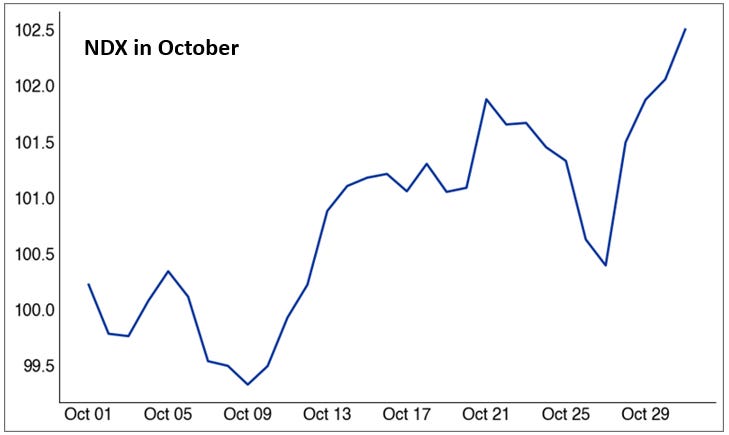

Seasonality

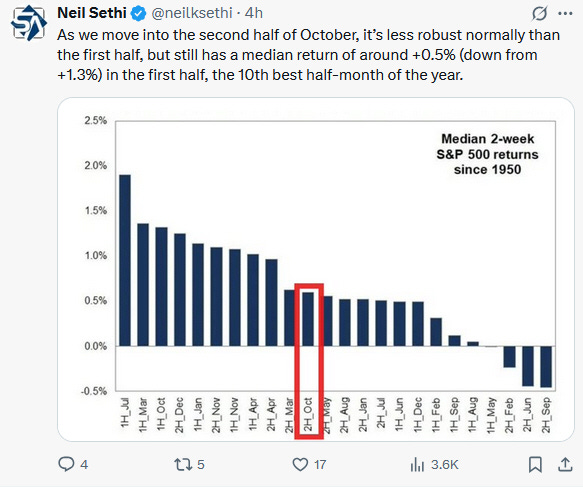

The second half of October tends to be a solid, if unspectacular, positive.

But, the second half of October can be choppy - look out for Black Monday clickbait posts on Twitter that come out this time of year. Below, for the Nasdaq100, note the pullback low that comes in at the back end of next week, shortly before the next Fed day on 29 Oct.

Summary

Price action: QQQ chopped around in a wide 20pt range, but didn’t follow through to the downside after the sell-off on 10 Oct. The long-term primary trend is bullish.

The Fed: Jerome Powell gave a speech in which he backed the dovish camp within the FOMC. He also guided for an end of QT, which is constructive.

Markets & Narratives: Tariff headlines continue to move the market. Look out for news relating to credit, either in bank earnings or credit spreads.

Breadth: breadth is poor.

Sentiment & Positioning: Positioning surveys remain neutral. After a spike early on Friday, the VIX fell -9pts.

Seasonality: Q4 is seasonally bullish, though October can be choppy.

View

Short-term: QQQ may not be out of the woods yet. A deeper pullback may present an opportunity for a long trade into year-end.

Long-term: the primary trend is bullish.

Technical evidence

QQQ is trending higher above its upward-sloping moving averages. It has reclaimed the bullish primary channel in play from the 2022 lows.

Realised volatility is consistent with bull market conditions.

Fundamental evidence

Monetary stimulus as the Fed cuts its policy rate.

Fiscal stimulus from the Trump administration’s spending bill.

Trump intends to appoint a dove as Jerome Powell’s successor.

Recent data shows US economy slowing, but OK.

Strong themes in tech: AI, defence, cybersecurity, robotics, nuclear.

Challenges and risks

Resumption of trade tensions with China.

Fed independence: will the Fed fall under the influence of the Trump administration and how will the market take that?

Policy: trade and immigration policy may lead to downside labour market and activity surprises, and/or upside inflation surprises over coming months.

If you find these posts useful, please do share with colleagues or friends - thanks!