QQQ weekly: 13 - 17 Apr 2026

Stampede

Price action

Last Sunday, talks between Iran and the US broke down, prompting President Trump to announce a naval blockade of the Strait of Hormuz. Weekend markets suggested a jump higher in oil and a gap down in stocks on Monday. However, during European hours on Monday, reports emerged that the two parties were continuing to engage. This set the tone for the week, during which incrementally better news emerged, culminating on Friday morning with a statement from Iran’s foreign minister Araghchi that the Strait of Hormuz will reopen as long as the ceasefire holds. Although this position was later contradicted by different Iranian voices on Friday afternoon, QQQ closed near the high of the week, up at a new all time high.

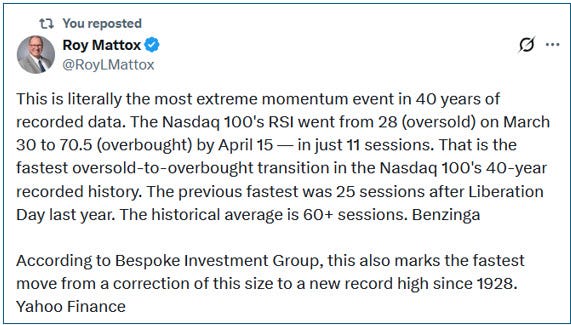

The bounce from the low has been unusually violent, even by QQQ’s recent V-shaped habits. From the 30 March low to Friday’s peak, QQQ has rallied +17%, which is real outlier stuff.

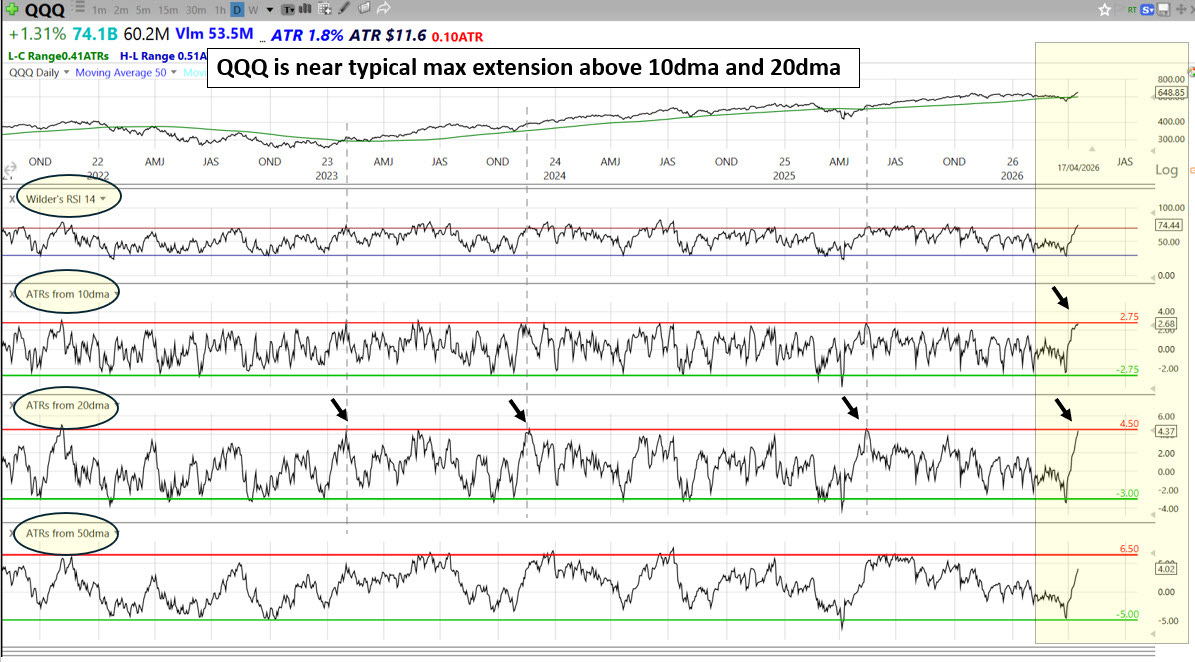

Consequently, QQQ is now short term overbought. I didn’t think I’d have to pull out the MA extension chart again so quickly, but here it is. As a reminder the chart shows how far QQQ has extended from its moving averages, expressed in terms of its 14d Average True Range (a measure of realised volatility, a similar concept to standard deviation). As you can see, QQQ is now about as extended as it gets from its 10dma and 20dma, so the base case now is for something of a short-term pause. (Note, the RSI reading of 74 is not problematic yet, 80+ is the level to get worried - great post here from Alphatica on the subject.)

Although a short-term pause seems likely, the burst of momentum over the last three weeks bodes well for the longer-term. See posts from SubuTrade here, Mark Ungewitter here, Isabelnet here, and Warren Pies here. The general view is that this move should be viewed as a bullish momentum event that implies strong 6m and 12m returns.

The Fed

The message from this week’s FOMC speakers was the same cautiously hawkish “wait-and-see” we have heard since the Iranian conflict began. The longer the war and the energy shock persist, the greater the risk consumer inflation expectations drift higher, and the greater the urgency for the Fed to act. So far, FOMC members have discussed the idea of hiking in conditional, hypothetical terms only, which has been a relief for QQQ.

Goolsbee (Mon): if oil stays over $90, it will spill over into inflation.

Hammack (Wed): baseline is for Fed to hold for a while, key is how high energy prices get and how long they remain there.

Musalem (Wed): current range of rates appropriate for some time, oil shock likely feeding inflation.

Williams (Thu): expect inflation to return to target in 2027 but likely well above 3% for next few months.

Waller (Fri): the longer the war goes on the greater the risk to inflation and jobs, surge in energy prices could have a lasting effect on inflation.

Daly (Fri): if shock ends soon Fed can return to policy path, if it persists, inflationary pressures will last longer, rates would need to rise if inflation took off, Fed can hold for now.

Markets & Narratives

1/ Iran

America and Iran are carrying on negotiations over the weekend. The ping pong of contradictory messaging from each side continues. Trump is keen to talk up the prospects of a deal, but this isn’t reflected in the noises we’re getting from Tehran. On Friday, we were told the Strait of Hormuz was open, but Saturday not. What is clear is that stocks and crude are both pricing in the notion we’re closer to the end of the conflict than the beginning, so we can expect a pullback if progress reverses.

2/ Private Credit

Some much better news this week in credit. JPM, WFC, BAC, and C all reported earnings this week. These banks have broad-based lending businesses, which provide a window into the health of US credit. Given the recent problems with private credit in terms of defaults, markdowns, fraud, redemptions, and gates, it was feared that the big banks’ earnings reports would bring further bad news. Thankfully, they provided a pretty benign view. Steve Eisman, financials sector GOAT whom I’ve referenced a fair bit on this subject, noted on his latest podcast that the big banks did not report any worrisome increases in non-accruing loans (ie seriously delinquent loans). Of the four big banks, JPM, C, and BAC reported a fall in non-accruing loans quarter-on-quarter, and only WFC reported an increase, and that was only +3%. Eisman notes, “the newsflow has been bad in private credit, but given the earnings reports of the big banks this week, we can say credit quality is overall fine. The bank earnings show the credit cycle is not here yet.”

We’ll get the next instalment of the story when Blackstone reports before the bell on Thursday. Hopefully their commentary tallies with the big banks…

3/ AI disruption

On Thursday, Anthropic announced the launch of Claude Design, prompting a number of software stocks, like ADBE, to drop out. However, software recovered to close higher on Friday. Are we seeing a turn finally? In the last two weeks the software ETF, IGV has undercut and reclaimed major support at 76.5 on very high volume.

Breadth

Breadth continues to recover strongly. Stockbee’s Market Monitor shows stocks rising +4% has heavily outnumbered those falling -4% since the market bounced at the end of March. This is the sort of heavy buying you tend to see at the start of rallies.

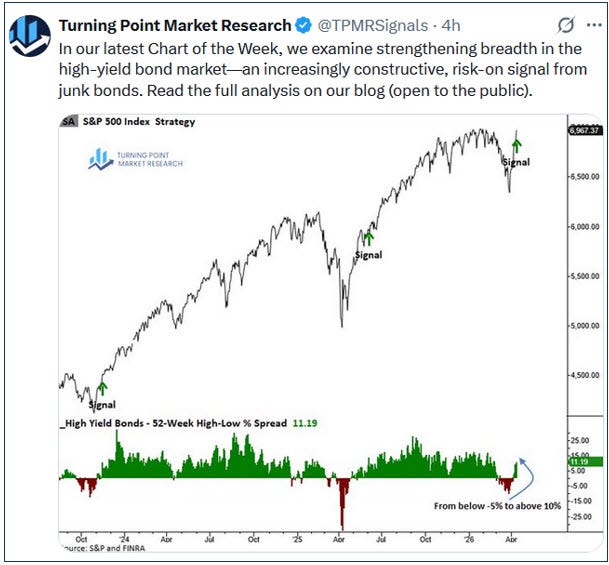

However, we haven’t seen the appearance of any well-followed breadth thrusts, like a Zweig Breadth Thrust, a Whaley Breadth Thrust, or Deemer Breakaway Momentum. But, we have seen a breadth thrust in high yield bonds. Given the poor headlines relating to private credit over the last six months, this feels significant.

Sentiment & Positioning

The VIX has been crushed as severe left tail scenarios relating to the Iranian conflict have drifted away. However, other metrics we look at haven’t normalised so quickly. The AAII survey still shows fewer Bulls (32%) than Bears (43%), while the NAAIM is still in neutral territory at 79. So, there’s a fair bit of catching up to do before things get euphoric.

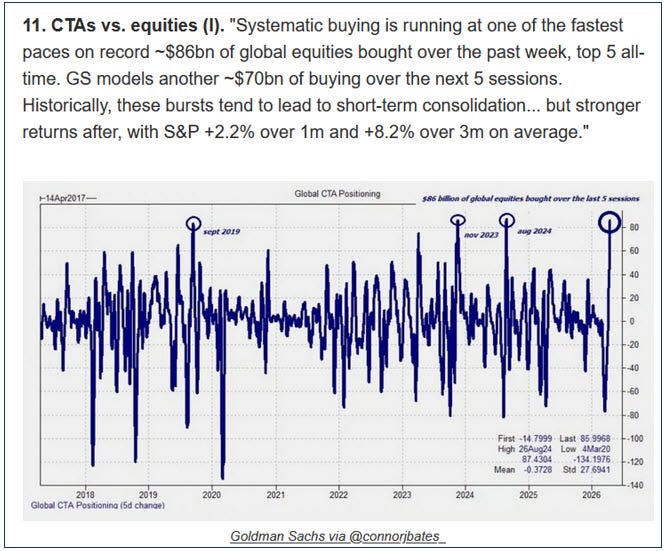

There has been quite a lot written about CTA positioning and the role of systematic strategies in the indices’ surge this month. Goldman suggest CTAs bought $86b of equities futures in the last five sessions in one of the largest examples of repositioning on record. GS reckons they are not done yet.

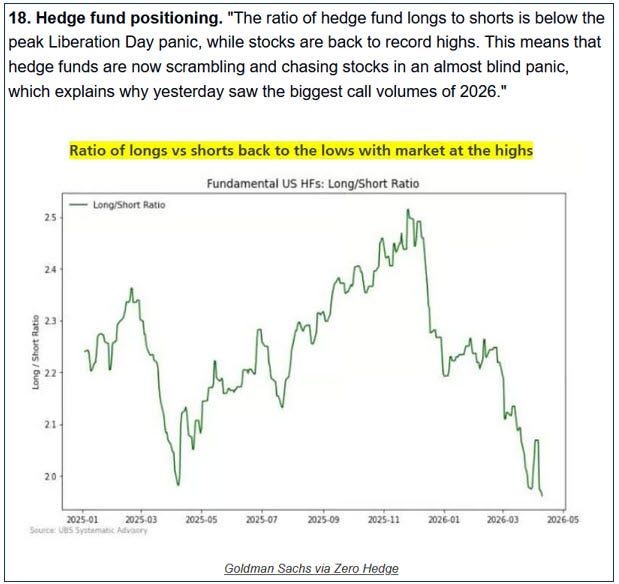

Hedge funds have also been caught offside with their positioning.

As for longer-term sentiment indicators, some view PEs as a useful gauge, which shows how far investors are willing to bid up stocks. The Nasdaq 100’s fwd PE at 22.4 sits below its 5y and 10y average (24.7 and 22.9 respectively), which is constructive. Good discussion here by Scott Rubner of Citadel.

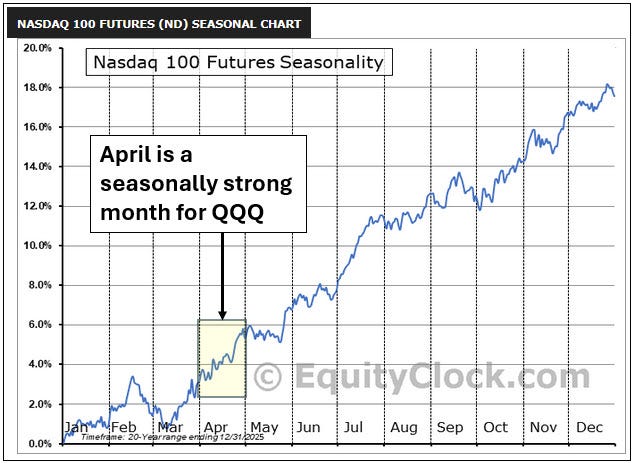

Seasonality

April is a seasonally strong month for QQQ.

Summary

Price action: having reached an oversold condition at the end of March, QQQ bounced on positive headlines relating to the Iran conflict. It has now risen +17% in one of the most violent V-shaped recoveries on record and is now short-term overbought. The bullish primary trend is reasserting itself, with QQQ above its 200dma and 50dma, which is turning back up.

The Fed: Fed speakers continue to guide that they expect to hold the FFR unchanged for an extended period while they assess the impact of an energy shock and tariffs.

Markets & Narratives: 1/ Iran - the conflict appears to be resolving, but the process is unclear and prone to unpredictable setbacks. 2/ Private credit - news improved this week, with large US banks reporting no major problems. 3/ AI disruption - the software ETF, IGV, may have found a floor.

Breadth: strong recovery as the indices bounced, but no Zweig, Whaley, or Deemer thrust signals. However, a high yield bond breadth thrust triggered.

Sentiment & Positioning: returning to neutral after reaching bearish extremes in late March. CTAs and hedge funds still have some repositioning to do if indices hold up.

Seasonality: April is seasonally strong for QQQ.

Key events next week: US/Iran headlines, earnings from BX, TSLA, IBM, INTC, VRT.

View

Short-term: base case pause, but open-minded

We noted last week that our base case was for a pause, but we were open-minded to the idea that de-escalation could bring a retest of the highs, which is what we saw. Base case this week is again for consolidation, based on QQQ’s extension from its 10dma and 20dma, and maybe a retest of 636. However, newsflow remains unpredictable - a US/Iran “deal” could see further upside panic, or a resumption of hostilities would likely bring a rapid unwind.

Long-term: cautious

Last week I lowered my longer-term view from bullish to cautious because the bullish tailwinds in play from the end of 2022 are fading and the mid-term year in the Presidential cycle can be a lemon. In particular the oil price shock arising from the Iran conflict means the Fed doesn’t unamibugously have the market’s back any more. However, there may be light at the end of the tunnel with the recent ceasefire and an apparent willingness on both sides to find a diplomatic solution. From a technical perspective, it’s very encouraging that QQQ has reclaimed its 200dma and hit a new ATH. If we can hold these levels a little longer, I will have more confidence in resuming a bullish longer-term outlook.

Challenges and risks

Iran conflict and energy shock.

Private credit.

Uncertainty relating to AI.

AI-disruption, OpenAI’s ability to honour its spending commitments, NVDA’s monopoly, capex depreciation, hyperscaler credit spreads, skepticism relating to scaling assumptions.

PS…

If you enjoy these posts and find them useful, please do share with colleagues, friends, or on social media - thanks!

Alex