QQQ weekly: 1- 5 Dec

Grinding higher

Price action

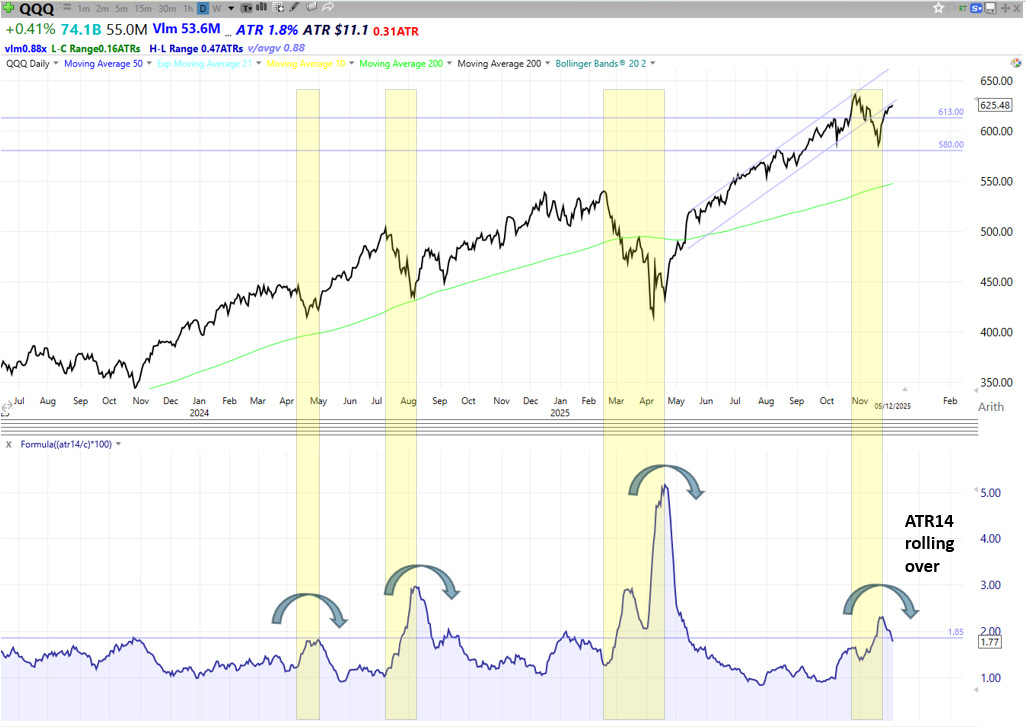

QQQ continued higher this week, following on from its Thanksgiving bounce. The price action was somewhat choppy, with a number of gaps and intraday reversals, but ultimately bullish. The move higher was helped along by data releases that didn’t rock the boat, and by the emergence of Kevin Hassett as the leading contender to replace Jerome Powell next year (more on that below).

Realised volatility is rolling over as shown in the lower pane below in the ATR14 expressed as a % of price. While that in itself of course doesn’t guarantee November’s corrective phase is behind us, it is consistent with the price action you tend to see when QQQ moves on from a pullback in a longer-term bullish trend. That’s encouraging.

The Fed

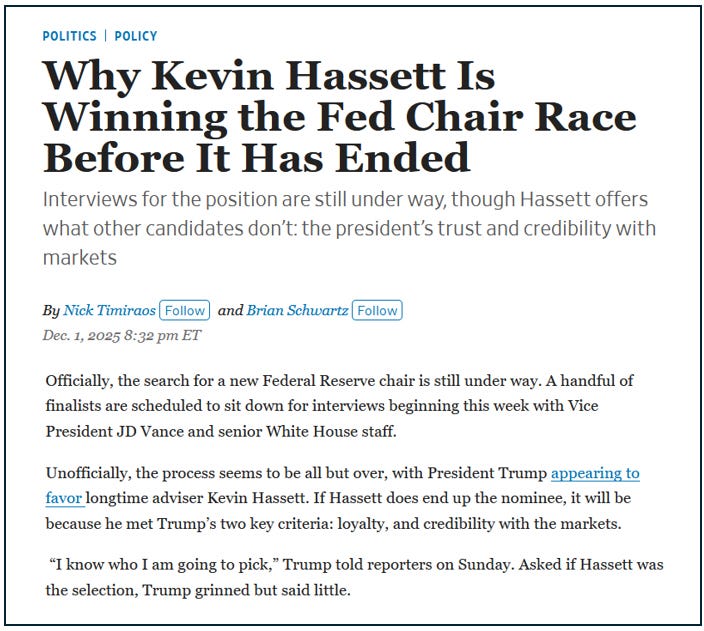

This week we had some developments on the question of who Trump will pick to replace Jerome Powell as Fed Chair when Powell’s term ends in May 2026. On Tuesday, Trump suggested they have whittled their long list of 10 candidates down to one. Without naming his choice, he hinted that it will be Kevin Hassett. Nick Timiraos of the WSJ also suggested the decision has been made.

Trump has made it clear he expects whoever he appoints to cut rates, regardless of the data. The assumption is Hassett will do Trump’s bidding. This could become a problem for markets in 2026 if inflation were to pick up and the Fed failed to act. Bond investors have apparently made that point, according to the FT.

On Tuesday, when Trump hinted Hassett is the front runner, referring to him as “the potential Fed Chair”, the US dollar weakened and the US Treasury curve steepened. This dynamic is likely to gain influence from here on. Hassett offered his views on the Fed Funds Rate in an interview on Friday, which was more restrained than Miran’s aggressive comments of late. For now, it seems, QQQ is OK with Hassett’s tenure.

Hassett (Fri): time for the Fed to cautiously reduce rates.

Markets & Narratives

1/ Bond yields

We haven’t discussed bond yields for a while, because they have been in a benign downtrend since May. However, as noted above, the dynamic around Fed independence may begin to influence bond yields. If Trump appoints a Fed Chair who is unwilling to lean against inflation, then bond investors may demand more compensation for taking inflation risk, leading to rising yields at the long end of the curve. Growth stocks don’t like rising yields, because much of their net present value derives from discounting distant future cash flows. They particularly don’t like it when bond yields break out suddenly. So, we are watching the US 10-year yield closely.

While US bond yields look like they might be about to break out of a longer-term downtrend, Japanese bond yields have already been rising for some time. Sharp accelerations of the trend can cause problems, as we saw in August 2024.

2/ AI

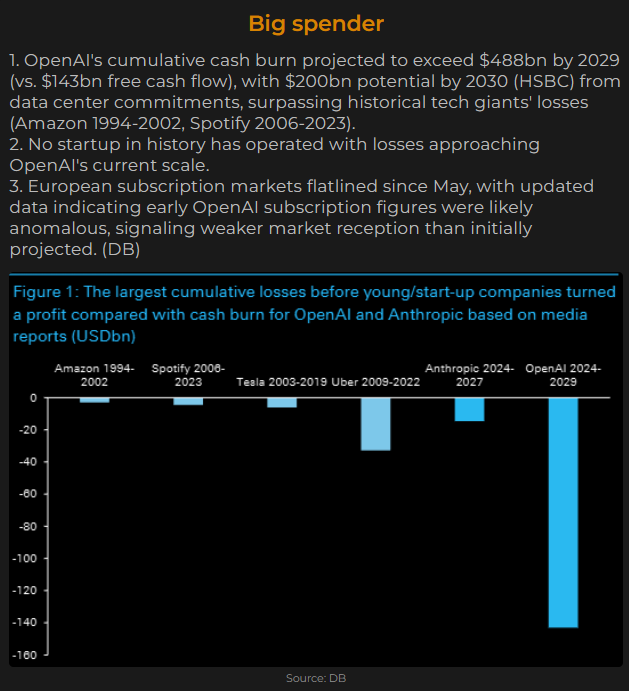

There is growing concern about OpenAI’s ability to honour its spending commitments.

Scrutiny regarding OpenAI’s ability to fund its expansion comes as Google’s Gemini is apparently overtaking ChatGPT. This muddies the AI theme.

Breadth

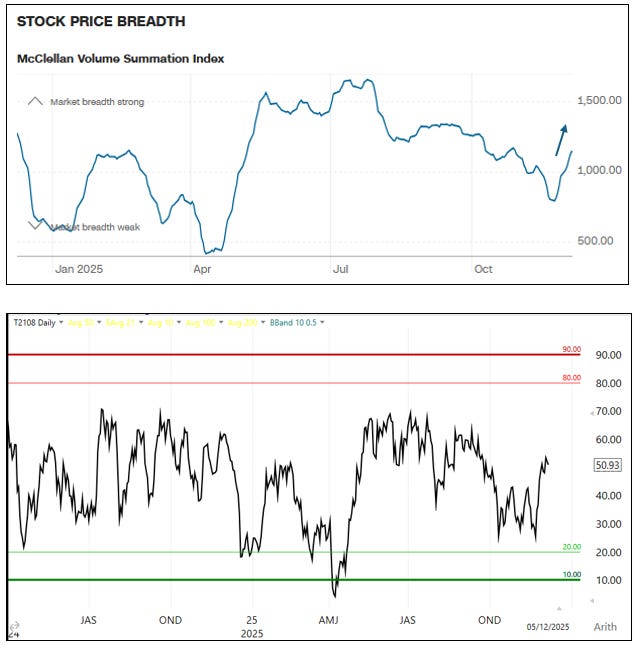

Breadth continues to improve. The McClellan Summation Index is rising quite quickly, along with the % of stocks above their 40dma.

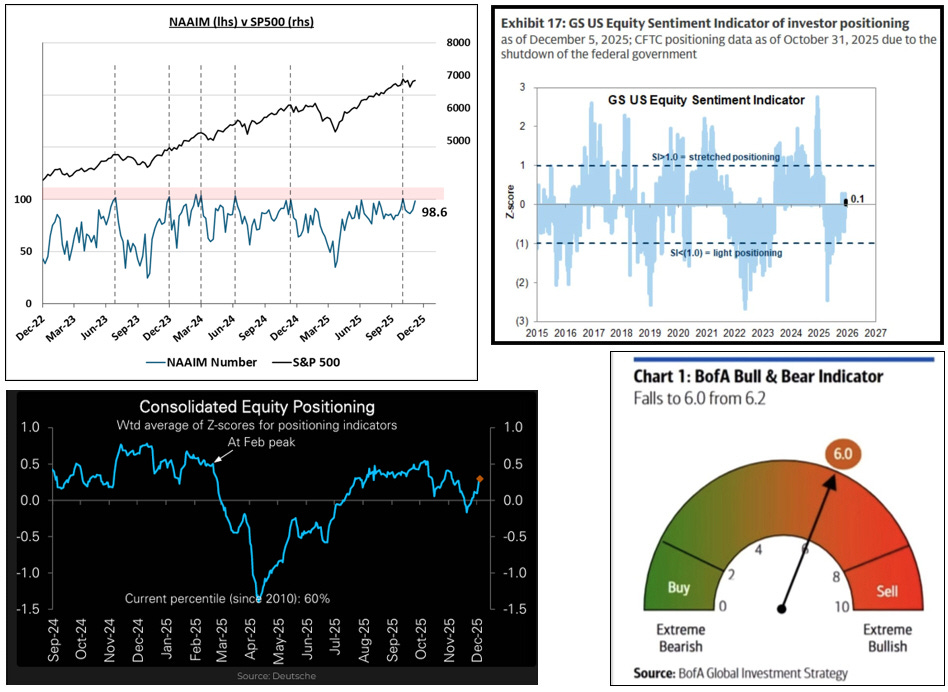

Sentiment & Positioning

Surveys suggest equity positioning and sentiment has grown more bullish as the market bounced, as you would expect. However, the surveys are not yet showing extreme readings that would warrant caution. The NAAIM is into the high 90s again, but not over 100. Deutsche and BofA’s indicators also suggest rising but not extreme bullishness. Meanwhile, Goldman’s US Equity Sentiment Indicator remains neutral.

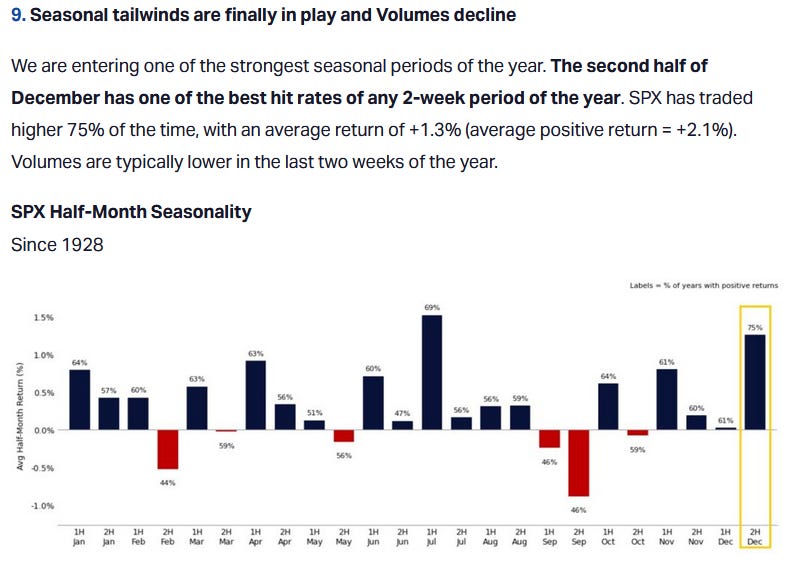

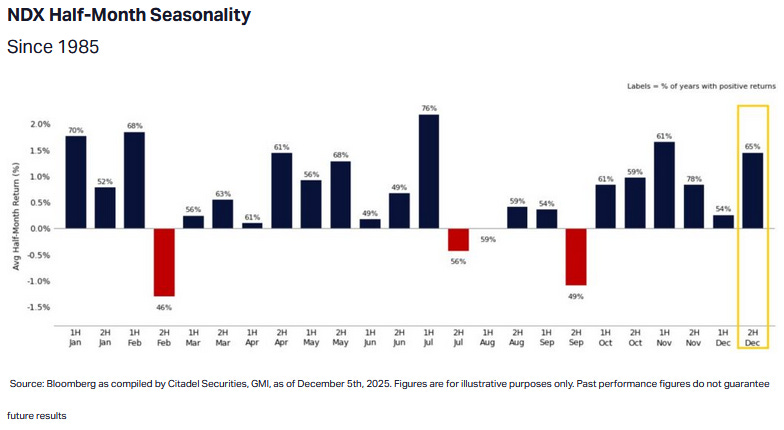

Seasonality

The second half of December is seasonally strong, as discussed by Scott Rubner of Citadel:

Summary

Price action: QQQ followed through to the upside after its Thanksgiving bounce. Realised volatility is falling, which is constructive. Longer-term, the primary trend remains bullish.

The Fed: Kevin Hassett emerged as the leading candidate to replace Powell as Fed Chair in 2026. This caused the Treasury curve to steepen, but has not impacted equities yet. The Fed is expected to cut by 25bps this week.

Markets & Narratives: rising bond yields may present a headwind to stocks if they accelerate to the upside. The AI theme is evolving into a complex story of winners and losers. At the moment, OpenAI is seen as falling behind.

Breadth: continued improvement.

Sentiment & Positioning: surveys suggest moderately bullish but not extreme positioning.

Seasonality: the second half of December is seasonally strong for QQQ.

Key events next week: FOMC meeting on Wednesday.

View

Short-term: short-term momentum is to the upside, supported by improving breadth, neutral positioning, and improving seasonality. But, keeping an eye on bond yields for signs of trouble.

Long-term: the primary trend is bullish.

Technical evidence

QQQ is trending higher above its upward-sloping 200dma. It has reclaimed the bullish primary channel in play from the 2022 lows.

Fundamental evidence

Monetary stimulus as the Fed cuts its policy rate. Trump intends to appoint a dove to replace Powell next year.

Fiscal stimulus from Trump’s spending bill.

Recent data shows US economy is OK.

Challenges and risks:

Uncertainty around the AI theme, in particular NVDA’s monopoly, OpenAI’s ability to honour its $1.4t spending commitments, capex depreciation, and hyperscaler credit spreads.

Fed independence: who will Trump announce as Powell’s successor and how will the market react? Will this lead to rising longer-dated bond yields?

If you find these posts useful, please do share with colleagues or friends - thanks!

Solid framework for thinking about near-term momentum versus longer-term structural risks. The point about bond yields potentialy breaking out is worth watching closely, since we saw in 2018 how quickly a steepning curve can flip the narrative on growth names. I'm curios whether the market has already priced in Hassett's dovishness or if we'll see another leg lower in rates once his appointment is formaly confirmed.