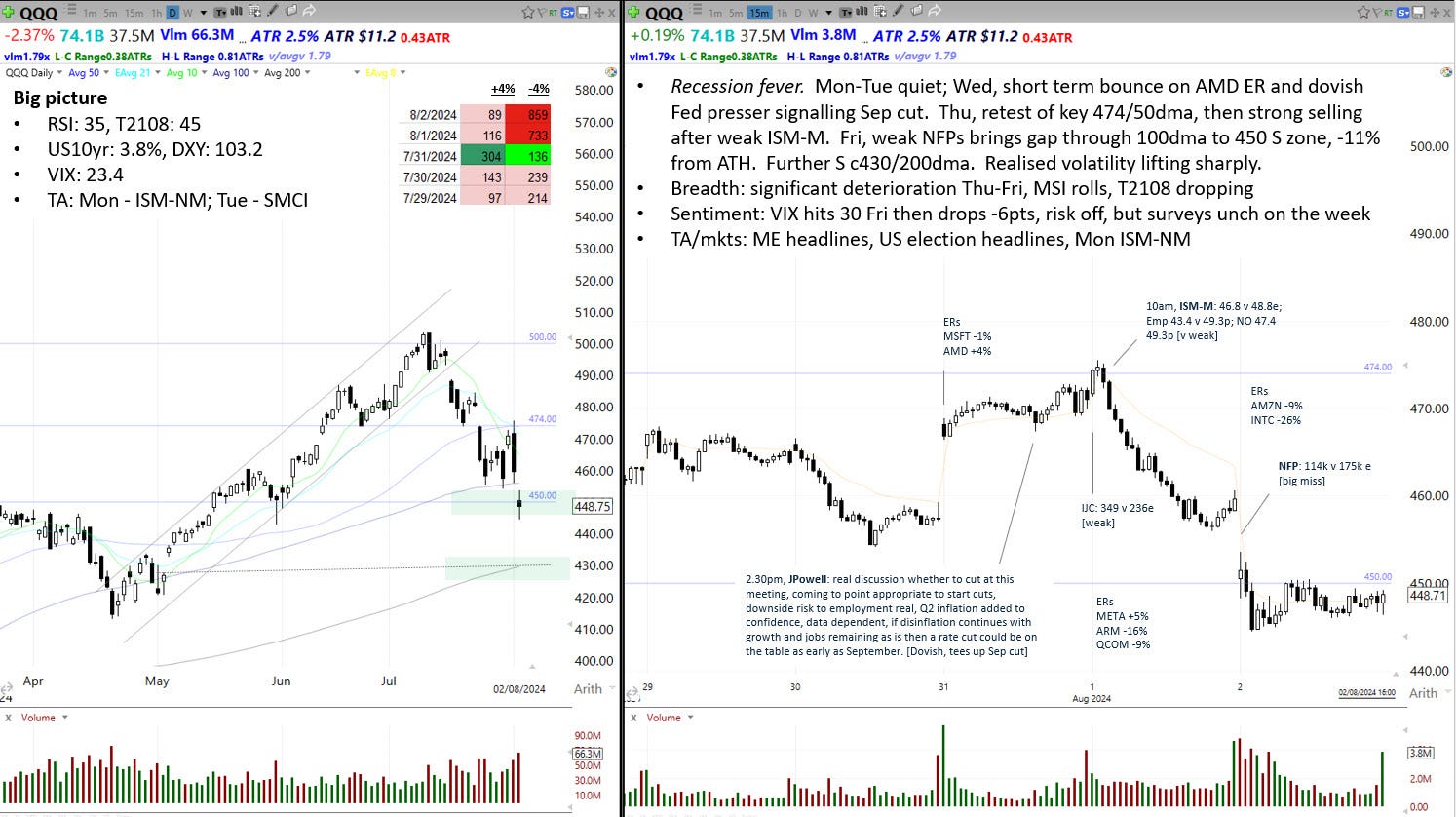

QQQ weekly: 29 Jul - 2 Aug

Price action

QQQ attempted to bounce Mon-Wed from the short term oversold condition we noted last week. However, the bounce failed into the key 474 level/50dma. This coincided with the release on Thursday of the ISM-M, which was very weak. Poor NFPs premarket on Friday prompted a gap down into the support zone c450, which held.

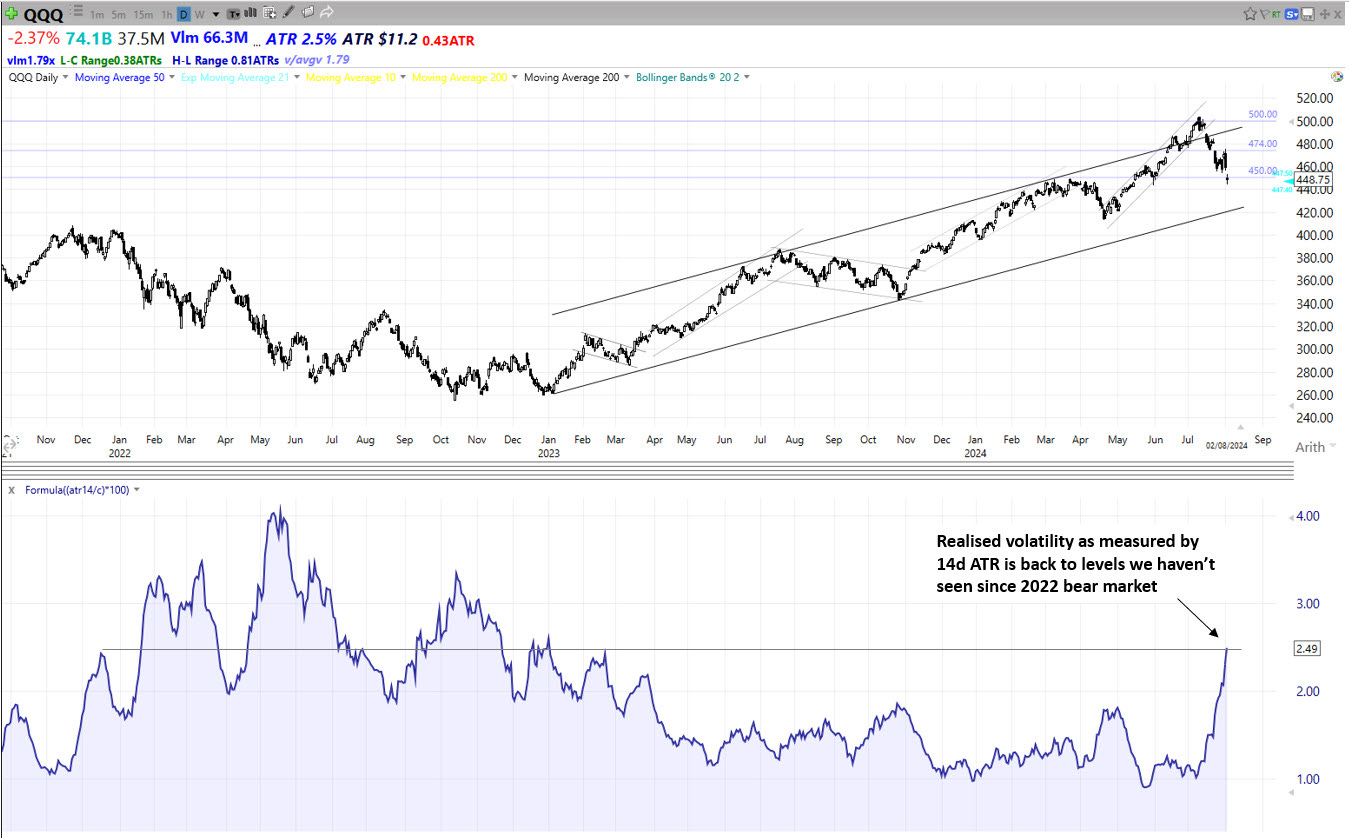

QQQ has now pulled back -11% from the high. A bounce seems likely, but note there has been a marked shift from a low volatility regime to a high volatility one. The chart below shows the 14d ATR of QQQ is now back at levels consistent with the bear market of 2022. Volatility needs to settle down before investors will feel confident about re-engaging.

The Fed

Wednesday was Fed day. JPowell guided expectations for a rate cut at the September meeting. Often the first question in the Q&A is teed up by one of the journalists to enable JPowell to deliver a clear message. NYT’s Jeanna Smialek asked, “the market pretty much entirely expects a rate cut in September, I wonder if you think that’s a reasonable expectation?” JPowell, deliberately reading from a prepared script, stated if data meets expectations “then a reduction in the policy rate could be on the table as soon as the next policy meeting in September.” Green light.

Following the FOMC on Wednesday, we had three data releases suggesting accelerating weakness in the jobs market: (1) the employment component of the ISM-M dropped to 43.9; (2) the IJC showed more initial claims than expected; and (3) NFPs on Friday were a big miss, 114k v 175k expected, with the unemployment rate lifting to 4.3% versus expecations of 4.1%. Austan Goolsbee, President of the Reserve Bank of Chicago, gave his take on Friday, “if unemployment is going to go higher than 4.1%, that’s the kind of thing the Fed has to respond to.”

Conclusions: 1) cuts are coming soon, 2) recession fever is the new narrative in play, and we should expect increased sensitivity to jobs data for some time.

What did we learn about markets?

The BoJ met this week and hiked rates, which accelerated a strengthening of JPY. Macro reversals of this magnitude can can spill over to other financial markets as speculators de-risk global portfolios.

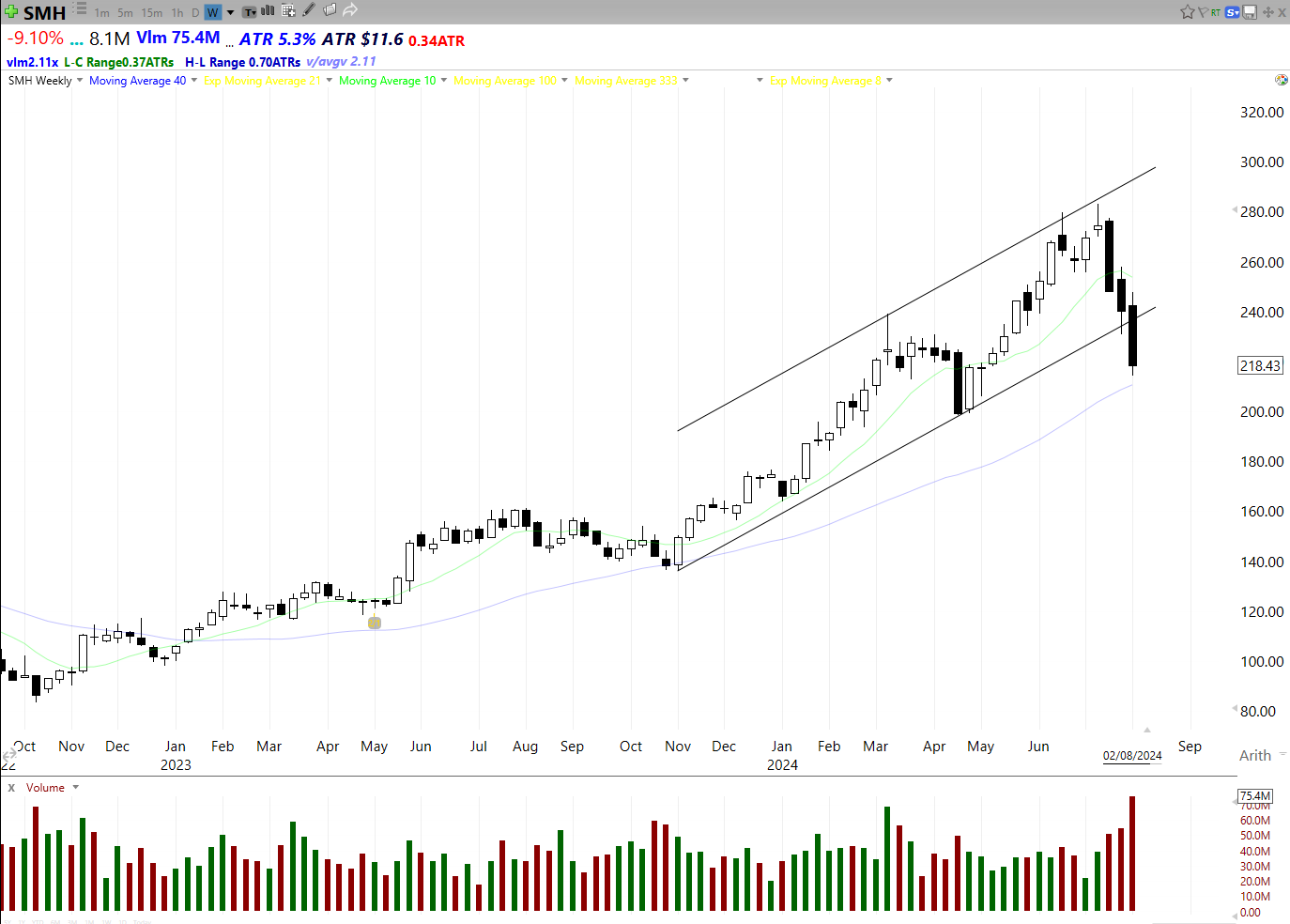

We also saw some awful price action among semiconductors, with SMH losing an important trend channel.

And on Friday INTC dropped -26% after reporting earnings.

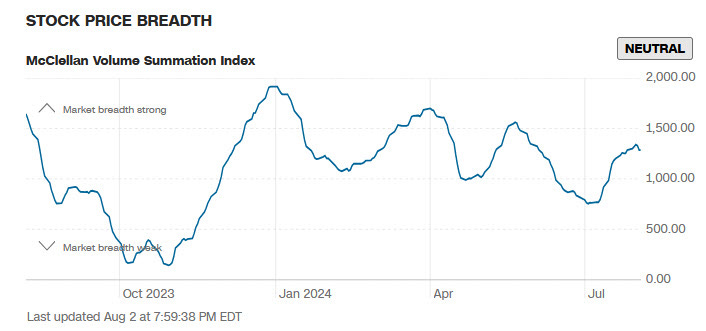

Breadth

Breadth deteriorated rapidly on Thursday and Friday. The rotation in play since 11 July gave way to a bout of high correlation risk off.

MSI: rolling over

% stocks above 40dma: rolling over

Sentiment

The surveys did not change much this week. However, we did see a large spike in the VIX. Note this faded rapidly on Friday, so maybe we have seen the peak. It would be better to see a clear capitulation in sentiment in the coming days, which would open the door to an enduring bounce.

Seasonality

Seasonality is playing out by the book during this pullback. Summer troubles arrived right on schedule.

Summary

Price action: QQQ continued to pull back after its failed breakout of 500. The primary trend remains bullish, but a shift in volatility regime may be warning of a a change.

The Fed: JPowell provided clear guidance the Fed plans to initiate a cutting cycle at their September meeting.

Breadth: deteriorated rapidly this week.

Sentiment: VIX spiked to 30, consistent with risk off and panic.

Markets: volatility in Japanese assets may have knock-on effects to global equities.

Key events next week: US election headlines, Mon - ISM-M

PS, an explainer for the weekly slide can be found here:

https://chartnotes.substack.com/about

PPS, if you find these posts useful, please do share - thank you!