QQQ weekly: 24-28 Jun

Price action

Monday brought downside follow through from last week’s corrective action, driven by NVDA falling for a third day, -6%. Tuesday brought a bounce which rode the 10dma higher till Thursday’s close. Friday’s cool/in line PCE release precipitated a pop at the open. However, the move stuffed at the key 486.8 level we identified last week. QQQ sold off hard the rest of the session and printed a heavy reversal candle on the daily, a third distribution day in the last seven sessions.

Having reached very overbought levels around 17Jun (RSI, 82), QQQ is bumping up against the top of the longer term bullish channel that began in early 2023. Are we entering a corrective or sideways phase?

The Fed

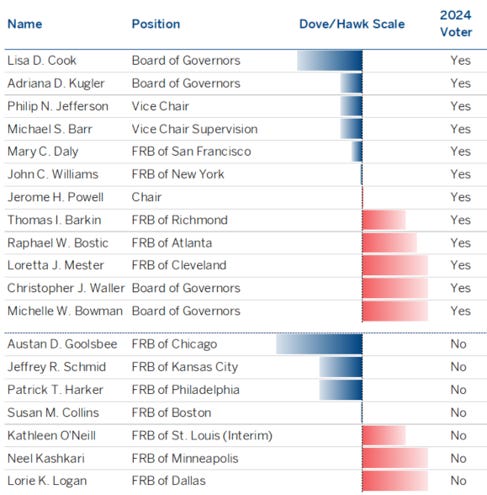

This week we heard from a range of FOMC speakers along the hawk-dove spectrum. The doves expressed optimism about inflation data and acknowledged the potential for cuts. The middle birds expressed caution. One pesky hawk contemplates hiking again if disinflation stalls.

Goolsbee, dove (Mon): optimistic about inflation, hopeful Fed will get confidence to cut

Cook, dove (Tue): at some point appropriate to cut, risks between inflation and jobs in better balance

Daly, middle (Fri, post PCE): PCE data is good news and shows inflation is cooling, policy working as expected, data dependent

Bostic, middle (Thu): one cut likely in Q4, but need to be absolutely certain inflation is moving to 2% before initiating cutting cycle

Barkin, middle (Fri, post PCE): lags still playing out that will slow economy, but policy possibly not constraining economy as expected

Bowman, hawk (Tue and Thu): not appropriate to cut, baseline is steady for some time, willing to raise rate if inflation stalls or reverses, upside inflation risks, do not see cuts in 2024

Here is a useful cheat sheet from BBVA (top panel shows current voters, bottom panel the non-voters):

Source: https://www.bbvamarketstrategy.com/public/fx-strategy/hawk-dove-cheat-sheet/

What did we learn about markets?

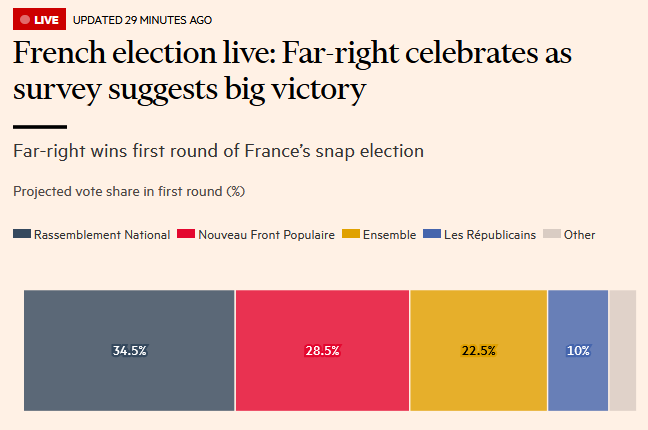

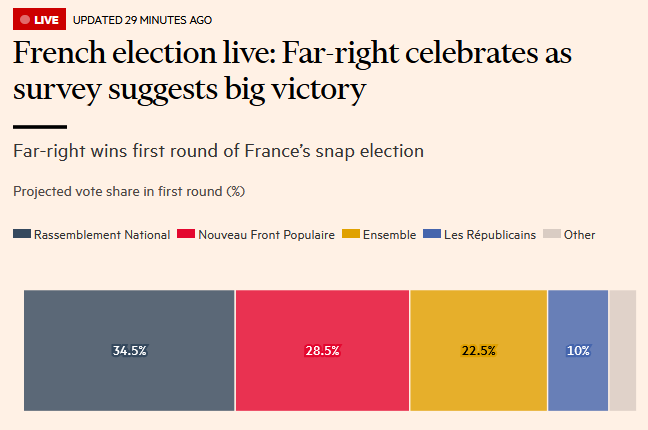

Headlines about political elections in the democratic West are coming thick and fast. Political uncertainty can generate market volatility and pullbacks, though generally not, on its own, a bear market. Next week will bring the first results of the election in France, the UK General Election (Thu 4 July), plus there is growing uncertainty about Joe Biden’s candidacy in the US Presidential Election. Can a combination of these events produce a summer pullback narrative?

France: Rassemblement National leads in exit polls

UK: The Financial Times backs Labour

US: The New York Times calls on Joe Biden to withdraw

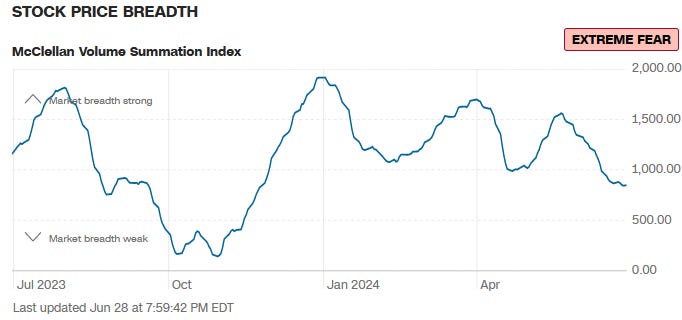

Breadth

Although the Market Monitor looked a little greener this week, the prounounced negative breadth divergence in markets continues.

McClellan Summation Index: still falling

Nasdaq100 Cumulative Advance-Decline Line: diverging from the index

Sentiment

The surveys continue to show bullish sentiment, while options markets show no change in the current deep complacency.

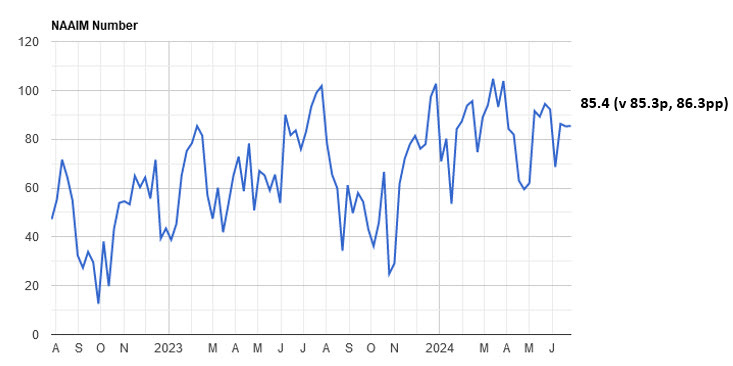

NAAIM: 85.4

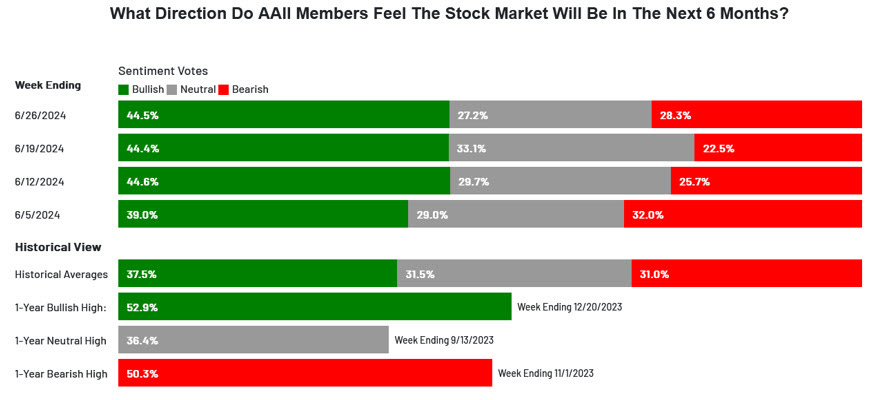

AAII: Bulls unch c44.5%, but Bears pick up somewhat

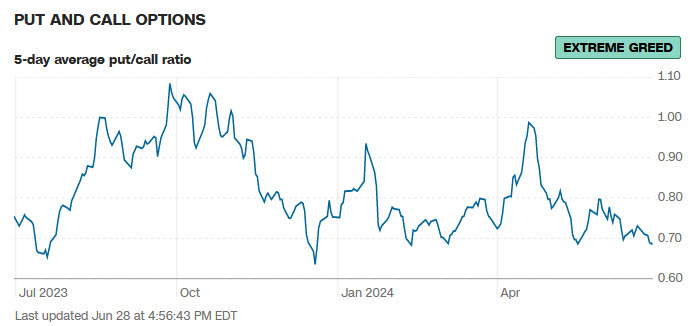

Put Call Ratio 5dma: stuck at very low levels, suggestive of complacency

Seasonality

VIX seasonality picks up mid July (source: equityclock.com):

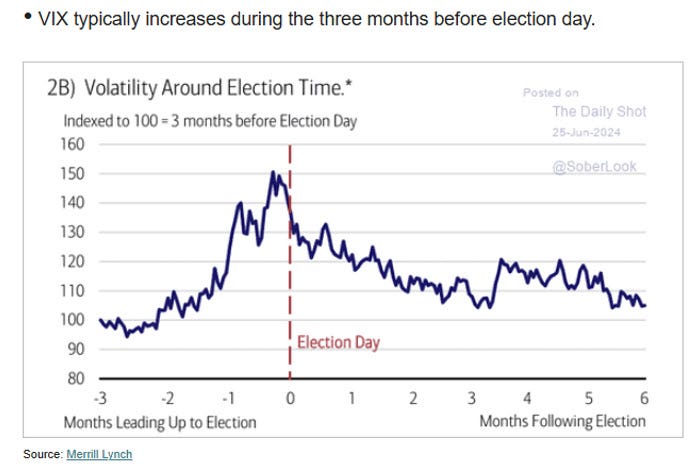

Implied volatility tends to pick up three months ahead of US Presidential Elections (sourcre: thedailyshot.com):

Summary

For a second week QQQ showed evidence of topping near the upper line of a long term bullish primary trend channel.

Fed speakers continue to offer a range of views about when the Fed might initiate a cutting cycle. Higher for longer remains the base case for now.

Political uncertainty in Europe and the US has the potential to develop into a pullback narrative.

Breadth continues to be problematic.

Sentiment is bullish. The put call ratio is low, which is a contrarian bearish indicator.

Seasonality suggests implied volatility tends to pick up from mid-July.

Key events next week: French and UK elections, ISM-M, JPowell, ISM-NM, FOMC minutes, NFPs

PS, an explainer for the weekly slide can be found here:

https://chartnotes.substack.com/about